Just because you’re a dividend investor doesn’t mean you’re fated to “grind out” income 3% and 4% at a time. With a slight change to your current (dare I say pedestrian?) strategy, you can keep your dividends and enjoy 81% to 437% price upside or more.

These types of life-changing returns are easily achievable within a few years. You just need to employ the ultimate contrarian dividend strategy – and buy select “born again” payouts.

The strategy is two-fold:

- Find the stocks with rock-bottom sentiment around them, and

- Only buy them when a cheery outlook is guaranteed.

First, Find Firms Burdened With This “Stigma”

Contrarian investing works because it capitalizes on overly-negative sentiment to find value. In the income world, this means buying when yields are abnormally high – and prices abnormally low – thanks to popular yet incorrect beliefs.

Corporate bankruptcies can be particularly profitable events for strong-willed income investors like us because they extinguish any and all hope.

And here’s the best part – we don’t even have to invest during the depths of despair. You and I can wait a few years until a successful turnaround is basically guaranteed. And we can still bank triple-digit returns then, with less risk than a typical stock purchase.

All thanks to the shame that lingers longer than it should.

While firms may emerge from bankruptcy in a matter of months, the associated stigma can last many years. An academic study published in the Journal of Finance studied the stock returns of 131 firms emerging from Chapter 11 bankruptcy – and found they outperformed the broader market over the next 200 days by a large margin.

Another study published by the International Journal of Business and Social Research studied 59 companies filing for Chapter 11 protection. It also found that these stocks beat the market handily over the next 250 days.

There’s nothing special about the 200 or 250 day threshold the academics picked. The stocks they studied crushed the market for the simple reason that they were “too cheap” thanks to the bankruptcy black eye they carried.

But we can do even better. Look, I hate losing money – and I’m not interested in buying firms as they emerge from bankruptcy. I only want to buy stocks in companies that are definitely going to make it, so that I can hold them profitably for many years. I also want them to pay me a dividend.

That’s why I employ this income-twist on bankruptcy buying. It helps me avoid the losers and bank safe double and triple-digit returns – while collecting yield to boot. (And by the way, it works whether or not the firm officially filed for bankruptcy – or simply got in enough trouble that it had to eliminate its payout.)

Next, We Buy the “Reborn Dividend”

How do we know when a turnaround is working?

Simple – management reinitiates the dividend.

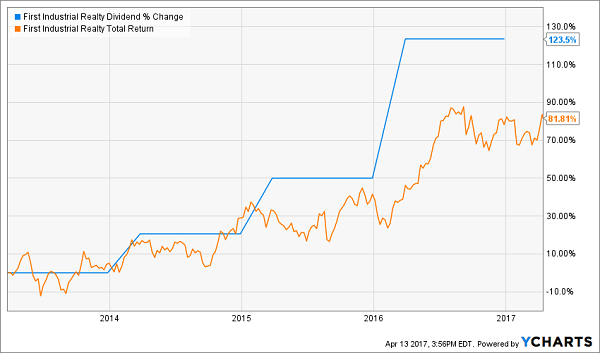

Let’s take the case of legendary REIT (real estate investment trust) CEO Bruce Duncan, who inherited a mess at First Industrial Realty Trust (FR). His first order of business when he took the helm in 2009 was to eliminate the firm’s dividend to preserve cash and pay off debt!

First Industrial leases distribution centers. And Bruce, as he described it, went “back to basics.” He had his team focus on increasing occupancy across his current facilities. Then, he started raising the rent on his tenants, and buying more buildings.

How’d investors know for sure that Bruce’s strategy was working? The clear signal came in 2013, when he reinitiated the firm’s dividend. Investors who bought then have enjoyed 82% returns in the four years since:

The “All Clear” Signal Precedes an 82% Gain

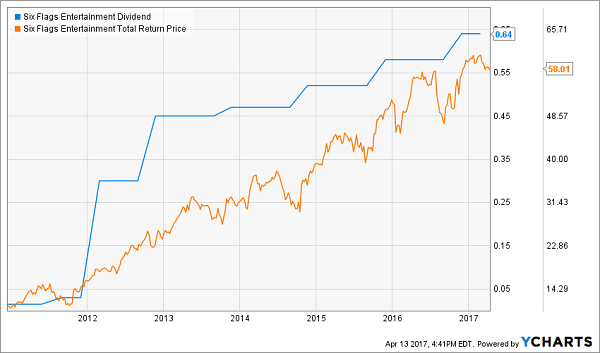

Theme park provider Six Flags Entertainment (SIX) similarly found itself in trouble in 2009, and filed for bankruptcy. The firm cleared its debt load, brought in a new CEO, and soon reinitiated its dividend in 2011.

The result? 437% total returns for investors!

The Next “Reborn Dividend” for 100%+ Gains

Every turnaround story (and bankruptcy case) is a separate situation. Here’s what to look for when buying a born again payout:

- A new CEO. In my experience, a new leader (and new way of thinking) is essential.

- Low or no debt. Most distressed firms simply owe too much money.

- A new dividend. Preferably one that is starting on an upward trajectory.

As you can see in our examples, you could have bought these stocks anytime after their dividends reappeared and done quite well.

My favorite dividend grower today is still selling for “free lunch” prices thanks to its own 2009 bankruptcy. It’s selling for less than nine times free cash flow (FCF), which is astounding considering that its turnaround CEO has already:

- Increased the firm’s dividend by 300%,

- Repurchased 36% of all outstanding shares, and

- Boosted FCF by 155%!

Its last dividend hike was an amazing 67%, and its stock price is still catching up. Which means this stock has 43% upside for the year ahead, thanks to its continued payout growth and share repurchases.

I have an email with my full analysis attached ready to be sent to my Hidden Yields subscribers this Friday. Are you a current subscriber of our dedicated dividend growth publication? If not, why not? Let’s fix that and get you setup with a 60-day risk free trial. You’ll receive my favorite pick this Friday along with my latest report highlighting 7 more dividend growth stocks with 100%+ upside.

If your retirement nest egg isn’t yet where you always wanted it, these dividend growers are simply the safest way to guarantee 12%+ annual price gains while you also enjoy a current income stream that (oh by the way) happens to grow by 10%+ every year!

“Efficient market” proponents are dead wrong – you can bank 12%+ annual returns following this safe dividend growth strategy. Click here and I’ll outline this strategy for you in detail – and I’ll also share my 7 favorite buys today, including names, tickers and buy prices.