The bond market is blowing up many retirement portfolios. Let’s make sure yours is outrunning inflation, rates, and everything else—with these yields up to 25%.

(That’s not a typo. We’ll talk 25% dividends in a moment. First, let’s address the fixed-income elephant in the room.)

The 10-year Treasury is rapidly running towards 3%—a level it hasn’t hit since 2018. The Fed’s hawkish stance has created a mass exodus in bonds, sending the T-note up from 1.5% at the start of the year to nearly 2.9% in just a few short months.

Now, that’s definitely no reason to start jumping into government debt. That piddling 3% isn’t anywhere near the levels of income we need to retire comfortably.

But it is going to make some investors think twice about some of the middling blue chips they own. After all, if you’re expecting little to no growth out of the stock market and are only getting 2% from the S&P 500 and many of its large, dividend-paying components… that T-note’s 3% is suddenly going to look a lot better, and that could take even more air out of America’s most basic stock holdings.

That puts an even higher premium on big, juicy yields, which should be mostly shielded from any eventual flight to the relative safety of bonds. But we need good and truly high yields—which is why we’re going to discuss five stocks and funds paying up to 25%

Why do we need so much?

It’s a simple matter of retirement math.

Even after 2022’s disappointing downturn, the S&P 500 still only yields 1.4%. Well, let’s think about that practically. Even if you had a cool million bucks to pour into an S&P 500 index fund, that 1.4% yield means you’d only bring home about $14,000 in annual income. That’s just barely over a grand each month!

Those 10-year notes are better than they used to, but even at 2.9%, that’s $29,000 annually—and only if you’re willing to plunk seven digits into government IOUs!

That’s why we need more—a lot more.

I like to target 7% to 8%, or more. That’s at least $70,000 or $80,000 annually if we have $1,000,000 to put to work. Or $35,000 to $40,000 on $500K. And so on.

The S&P 500 itself may not pay much, but we can find many stocks and funds that yield 7% or more. We just need to know where to look.

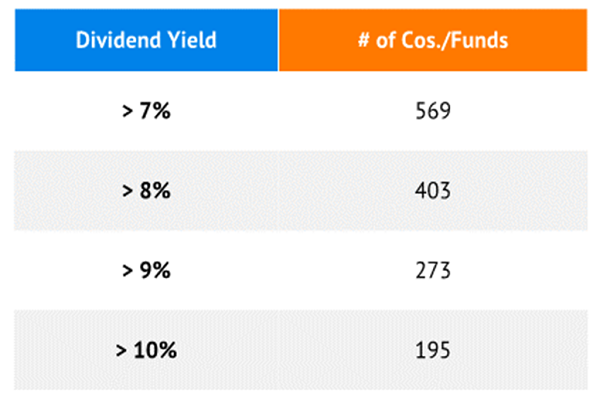

It Pays to Be Contrarian: Yields Over 7%

Note: U.S.-listed companies and funds with market capitalizations or AUM greater than $300 million. Source: S&P Global Market Intelligence

Now we wouldn’t want to toss these 569 stocks and funds into an ETF and buy it. There are some dividend disasters in here. We need to sort through this pile.

Which is why we’re talking today. Here at Contrarian Outlook, we research high yield so that you don’t have to.

But that’s why I’m here. I’ve put in the research to help you find those exceptions that can change your retirement overnight.

Let’s consider five today—yielding between 8% and 25.2%—to see which are potential candidates for a “retire on dividends” portfolio.

Buckle (BKE)

Dividend Yield: 21.0% (TTM)

Let’s start out with a dividend that’s much more than it seems.

Buckle (BKE) is a fashion retailer of mid- to higher-end clothes, accessories and footwear that operates 439 stores in 42 states. And it relies on special dividends to reward shareholders while remaining financially sound. You see, BKE pays out a 35-cent regular quarterly dividend that itself has grown at a decent clip over the past half-decade or so. Based on that, BKE yields about 4.3%.

But it also has paid out a variable special dividend depending on its profits—its $5.65-per-share distribution in 2021, for instance, elevates that yield to a fantastic 21%!

The question is: Will the stock itself hold up?

Like many brick-and-mortar fashion names, Buckle has seen its sales gradually decline over time as Amazon.com (AMZN) and other e-tailers carved out their place. But 2020 and 2021 were something of a renaissance, with revenues actually improving during the worst of the pandemic, and last year delivering a more than doubling in profits.

However, shares crested last year and have lost more than a third of their value since November. That’s because year-over-year comparisons will no longer be kind to BKE—the pros expect profits to retreat by double digits in its current fiscal year, on tepid top-line growth.

Retirement investors should best consider this: Fashion is fickle. Be it American Eagle (AEO), Gap (GPS) or other similar retailers, these stocks typically only work best as swing trades. But there’s no meaningful path to long-term growth in a brick-and-mortar retailer whose store count ebbs each year.

This Balloon Could Let Out Even More Air

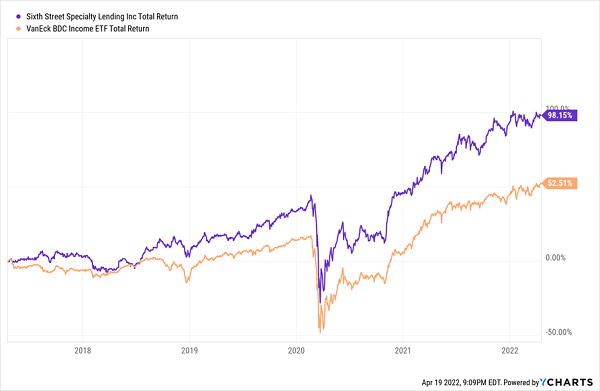

Sixth Street Specialty Lending (TSLX)

Dividend Yield: 10.2% (TTM)

A potentially steadier stock that also leans on special dividends is Sixth Street Specialty Lending (TSLX)—a business development company (BDC) previously known as just TSLX that I like to pop in on every now and then.

As I’ve said before, TSLX swings for the BDC fences. It makes transactions of up to $300 million (and syndicated transactions of up to $500 million) to companies between $15 million-$300 million in companies between $50 million-$1 billion in enterprise value bringing in between $10 million-$250 million in EBITDA. It’s not choosy about how that capital is put to use, either: organic growth, acquisitions, restructuring and a few other uses are all fair game. And it will do investments of all kinds – senior secured loans, mezzanine debt, non-control structured equity and common equity.

That lends itself to an eclectic group of portfolio companies, from human resources support services firm PrimePay and education data company Illuminate Education to struggling retailers such as JCPenney and Staples.

TSLX looks particularly good in the current environment given that it’s primarily floating-rate in nature, meaning it can benefit from rising short-term rates, which are all but guaranteed in the near future.

And again, Sixth Street leans on special dividends to augment its regular dividend. That’s a great safety valve during lean times, as you can pull back and still guarantee a minimum level of income—and of course, during boom times, investors reap the rewards.

TSLX Has Been a Standout BDC

It’s worth noting that TSLX trades at a fat 1.4x to net asset value (NAV). That’s mighty pricey—in fact, that makes Sixth Street one of the most expensive BDCs on the block. But it’s also worth noting that investors rarely get a chance to buy this stock at a fair price.

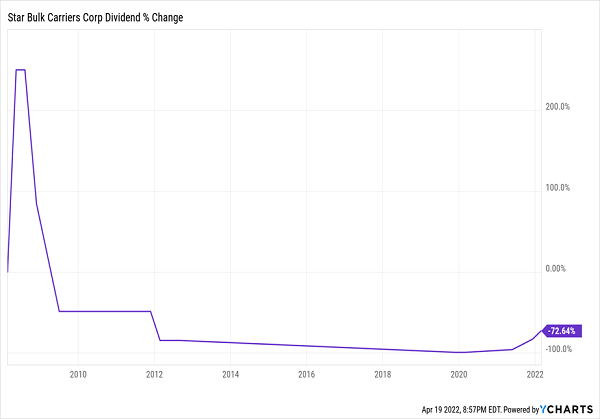

Star Bulk Carriers (SBLK)

Dividend Yield: 25.2%

What could be wrong with a 25%-plus yield that has grown by more than 440% annually over the past three years?

Well, that’s the big question facing potential investors in Star Bulk Carriers (SBLK).

Star Bulk is a global dry bulk shipping company with a fleet of 128 vessels ranging from Supramax (medium-sized) to Newcastlemax (extremely large, and named as such because they’re as big as they can get and still enter Australia’s Port of Newcastle).

These vessels transport everything from iron ore to fertilizers to grain, delivering more than 60 million metric tons of cargo across the world annually.

And as you can imagine, business has been good.

The COVID-19 pandemic flipped a lot of industries upside-down, but few industries past home exercise bikes and video conferencing have benefited more than shippers. That’s because the global supply chain has been thrown into complete disarray, juicing shipping costs the world round. Consider that the Baltic Dry Index (a composite index measuring varying types of dry bulk carriers) has shot up from about 770 from the start of 2020 to highs well into the 5,000s and have since receded to still-fruitful levels in the low 2000s.

SBLK saw revenues more than double between 2020 and 2021, while net income shot up from about $9.7 million to $680.5 million in that time.

That has meant excellent things for its dividend, which began under a new policy in late 2019. Each quarter, an aggregate dividend will be declared equal to the company’s total cash balance minus a minimum cash balance equal to its number of vessels multiplied by varying amounts through 2021 up to $2.10 million in the fourth quarter and beyond. As a result, Star Bulk has gone from offering up 5 cents per share all year in 2019 to $2 per share in just the first quarter of 2022 alone.

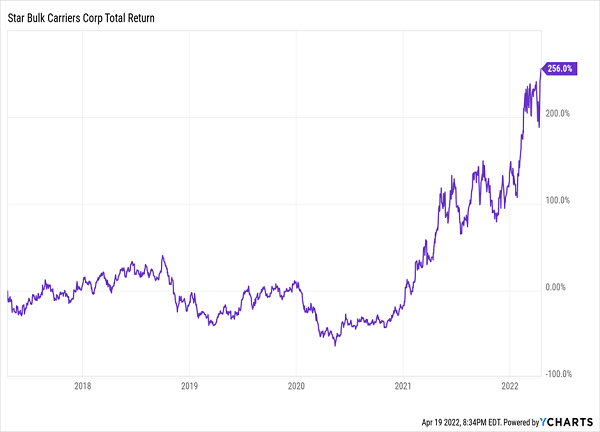

That makes for nearly irresistible returns for as long as shipping rates remain elevated. SBLK has more than tripled over the past five years, with virtually all of that progress coming since 2021.

Star Bulk: To the Moon!

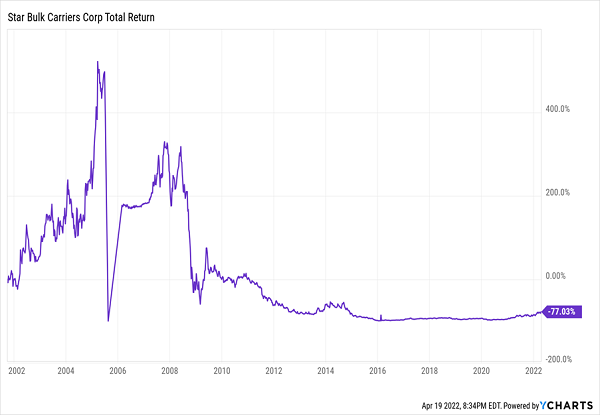

But the question is: What happens when the world returns to some form of normalcy? The longer-view lens might tell the tale:

Shipping Hasn’t Been a Good Business in Years

Star Bulk’s profits are expected to decline modestly this year before falling by nearly a quarter in 2023. That’s not to say SBLK can’t make the most of continued supply-chain difficulties, or even that the yield will disappear altogether. But it’s a variable dividend—one that easily could fall off its perch when the world goes back to normal.

It Wouldn’t Be the First Time

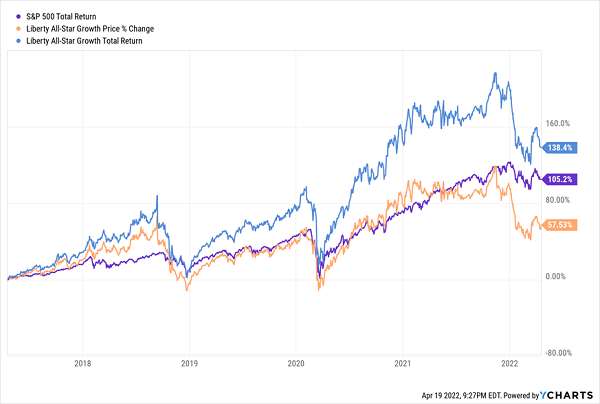

Liberty All-Star Growth (ASG)

Dividend Yield: 8.0%

Another place we can tap for high yields is the closed-end fund (CEF) space. Less revered than their mutual fund and exchange-traded fund (ETF) brethren, this tiny corner of the fund world uses a variety of levers to generate exceedingly high yields, even out of otherwise mundane assets.

Take Liberty All-Star Growth (ASG), for instance. With a yield of 8%, you might assume that ASG invests in a high-yield asset class such as BDCs, REITs or maybe MLPs.

Nope. Instead, the portfolio is split into three different fund management groups, each of which is tasked with buying equities in various depths of the asset-class pool: large caps, mid-caps and small caps.

But as the name implies, they’re all looking for growth.

The result is a portfolio ranging from mega-caps like Amazon.com (AMZN) and Alphabet (GOOGL)—both of which don’t even pay a dividend, mind you—to relatively unknown mid- and small-caps such as Montrose Environmental Group (MEG) and StepStone Group LP (STEP).

So…where’s the income coming from?

That’s the rub. Sometimes ASG distributes dividend income from its holdings, but some of its distributions are long-term gains, which means they’re treated differently come tax time. But for what it’s worth, those distributions (capital gains or otherwise) still make a world of difference.

All-Star Growth Lives Up to Its Name

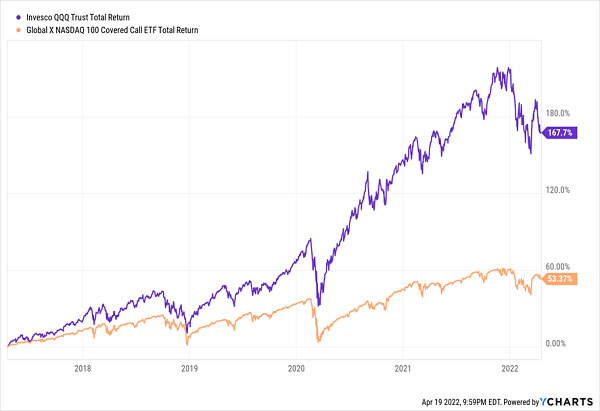

Global X NASDAQ 100 Covered Call ETF (QYLD)

Dividend Yield: 11.6%

What if you got paid more than 10% to hold the Nasdaq’s most prominent stocks?

That’s effectively the deal on offer with the Global X Nasdaq 100 Covered Call ETF (QYLD), which does indeed offer double-digit yields despite being a portfolio of tech and other high-growth stocks.

But it doesn’t just hold them. It trades them. Sort of.

QYLD holds a number of individual positions to replicate the performance of the Nasdaq-100 Index. But then it writes calls on the same index to generate a high base level of income.

So Wait. What Gives?

Selling covered calls in general naturally limits the potential upside of the underlying holdings, but QYLD’s method of methodically trading merely index options rather than picking and choosing individual-component options leaves a ton of money on the table.

Live Off Dividends Forever With This “Ultimate” Retirement Portfolio

Frankly, you have two better options on the table:

You could consider a similar actively managed strategy that beats the pants off QYLD.

Or you could go with a much simpler (but still high-yielding!) mini-portfolio of my favorite “triple play” holdings: The 7%-yielding “No Withdrawal” retirement portfolio.

We all know you need enough income to cover all of your regular expenses. And we probably all inherently know that we should be holding high-quality stocks. But investors often overlook the importance of growing their nest egg in retirement – that way, if the unexpected happens, you won’t cripple your dividend-producing potential to dig out of trouble.

Get on Google and search for a set of “best stocks” by some of the mainstream financial outlets. I have—and after a few quick analyses of these “pro” sets of picks, I calculated likely total returns of between just 3% and 5% annually, based on so-so dividends and potential share appreciation from paltry estimated earnings growth now that the “recovery bump” is starting to be priced in.

Those kinds of returns will force you to bleed your nest egg dry just a few years after you retire. And you have worked too hard, for too many years, just to struggle financially in your golden years.

My “No Withdrawal” portfolio features the best of several high-income assets. Of course, only a handful of stocks and funds meet my rigorous standards for this multipurpose strategy. But the result is an “ultimate” dividend portfolio that provides you with …

- An average 7% portfolio yield

- The potential for 10%-plus in annual capital gains

- Robust dividend growth that will keep up with (and beat) inflation

This portfolio will let you live off dividend income alone without ever touching your nest egg. You won’t have to worry about paying the mortgage or other monthly bills, nor will you have to wonder how you’ll survive if a financial disaster strikes.

Let me show you how to secure the comfortable retirement you’ve worked your tail off to enjoy. Click here and I’ll provide you with THREE special reports that show you how to build this “No Withdrawal” portfolio. They include names, tickers and full analysis of their wealth-building potential 100% risk-free!