If you flip on the financial news this Friday, or click over to your favorite stock website, you’re going to see headlines about retail stocks. After all, they can’t have a Black Friday without weighing in on immediate winners and losers!

In recent years, the retail sector has produced many more losers than winners. Amazon (AMZN) is blamed as the brick-and-mortar-killer, taking down not only unimaginative retailers but also the landlords that rent to them.

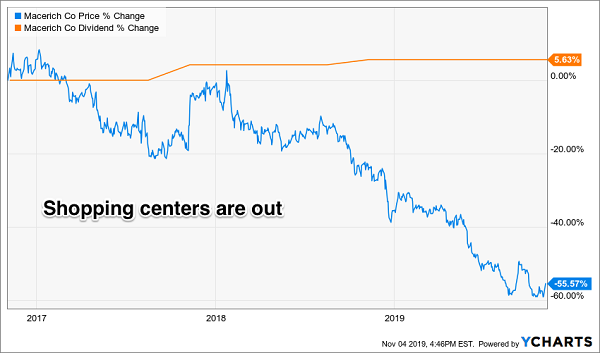

The carnage even extends to shopping center rentiers like Macerich (MAC). It promises a 10.2% yield, but this inflated payout is due to a stock that split “the wrong way”—halving in price without the increase in sales! This double-digit yield probably won’t last long. It is living quarter-to-quarter as tenants (and the rents they pay this REIT, or real estate investment trust) are being bombarded by free shipping courtesy of Bezos & Co.:

These Token Dividend Hikes Don’t Fool Mr. Market

On the whole I would lump most retail REITs into Macerich’s troublesome bucket. Problem tenants are going to make consistent payouts a problem.

So does this mean that we income seekers should ignore retail entirely? No! There are actually select, savvy firms that are benefitting from Bezos & Co. taking down their competitors.

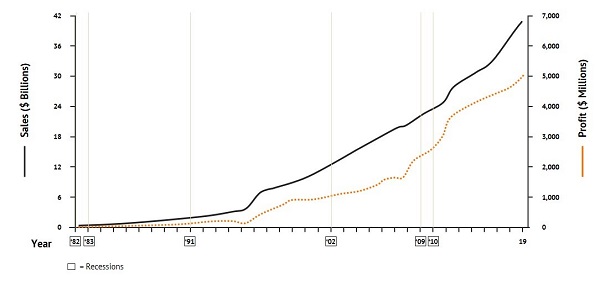

One of my favorites is a good one for anyone who prefers their stocks to be “recession-proof.” Below is a chart of its sales (black line) and profits (dotted orange line) since the 1982 recession. The firm has sailed through the last five recessions, in fact, with barely a hitch:

With results like this, you’d probably think this recession-proof growth stock is priced for perfection today. It isn’t. Because it is actually one of the best companies in a challenging industry, it is still a discounted stock today. Yet for reasons we’ll discuss, these industry fears are misplaced for the firm, which means its cheap shares are a screaming bargain.

Why would we want to fish in a turbulent pond? (Other than the fact that we can do so cheaply? After all, the cheap can always become cheaper!) We’re combing through this out-of-favor industry because we can own the top companies that are easily gaining market share at their failing competitors’ expense.

As mentioned, retail has been an increasingly tough place to make a buck in recent years. The big bad Internet has huffed, puffed and blown down many brick and mortar business plans. Why go to a store when Amazon.com (AMZN) can deliver it to your doorstep in days—or hours!

And it’s hard to blame investors for wanting to own Amazon. The e-commerce giant is in a constant state of gobbling up and digesting traditional retailers. Amazon Web Services, the firm’s cloud hosting solution, prints money too. Bezos & Co. use these profits to subsidize their online domination of retail, mowing down all who dare get in their way.

But not all, it turns out. Some brick buildings are still standing. In fact, their businesses are actually getting stronger and stronger thanks to the smackdown that Amazon is laying on their competitors.

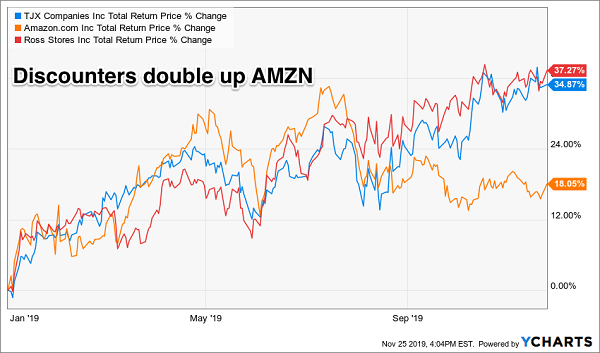

Firms like Ross Stores (ROST) and TJX Companies (TJX) are able to buy their discounted merchandise at even bigger discounts. Being the last stores standing, they can name their price! Plus the online world still can’t compete with the thrill of finding a bargain in person.

The shoppers inside a Ross store and TJX’s T.J. Maxx aren’t merely combing through clothes racks so that they can buy the same item from their phones. They’re going to make their eventual purchase in-store, to the benefit of these shareholders. In fact, these two stocks have returned 50% to 100% more year-to-date than the bandwagon-riding shareholders of Amazon!

The Last Stores Standing are Thriving

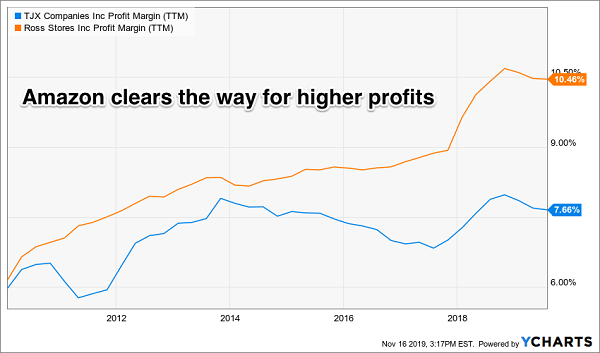

The rise of online shopping is actually helping these Internet-resistant retailers. As competitors have dropped off, TJX’s profit margins have improved by 41% over the last decade to 7.7%. (If you’re scoring at home, this towers above Amazon’s current 4.3% margins.)

Thank You, Bezos, for Bankrupting Our Competitors

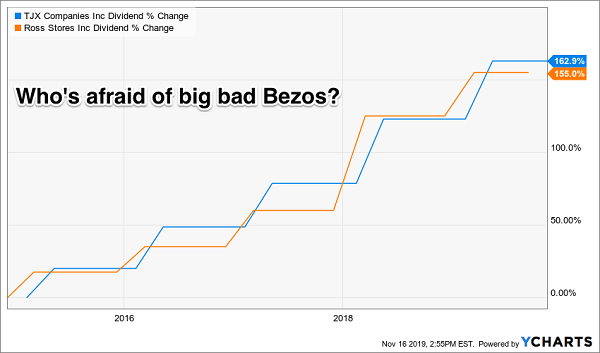

We like higher profits when they translate to higher payouts for us. And boy, do they ever with this dynamic duo. Over the last five years these two timeless discounters have shrugged off Amazon’s domination and delivered 155% to 163% dividend growth to their investors:

Dividend Growth Up to 163%

This dividend growth is why these stocks have beaten up on Bezos & Co. year-to-date. As long as these firms continue to increase their payouts, there should be more triple-digit stock price gains to come.

With the interest rates plunging, the best move you can make is buy dividend growth. Because if there’s one thing we can count on, it’s this: as long as so-called “safe” investments pay less than inflation, fast-growing payouts will be in high demand.

Zero in on those stocks with accelerating payouts backed by soaring cash flows, and you’ll be well on your way to doubling your nest egg (and your income stream) fast.

7 “163% Upside” Buys to Double Your Nest Egg and Triple Your Income

You know me, I’ve got 7 perfect buys for our new plunging rate environment: 7 “hidden” stocks I’ve handpicked to pay you up to 163% in gains and dividends.

That’s more than DOUBLING your money in just a few years!

Imagine turning a retirement “pot” of $250,000 into $500,000, or $500,000 into $1 million. And on it goes.

Plus, these 7 dividend wonders are growing payouts at an accelerating pace. That sets you up to earn 10%, 13%, even 15% yields on your initial buy in just a few years—just like the lucky folks who bought Ross and TJX a few years back!

And even if the market does take a tumble, these stocks’ soaring dividends give you downside protection as more yield seekers spot their surging income streams and buy in, eager to hedge their own downside with dividend cash.

Don’t miss your chance to buy these 7 “hidden” dividend plays while you can still grab a bargain. Click here and I’ll give you everything I have on each one: names, tickers, buy-under prices and the double-digit dividend (and share-price) growth you can expect from each one.