Think back three months: The market was in the throes of the “tariff terror.” Us? We were doing what we always do: sifting out overly beaten down closed-end funds (CEFs) with huge yields.

Today, the stock market is doing the opposite of what it was back then—levitating from all-time high to all-time high. And we’re still finding bargain-priced dividends. Right now, some of the best ones are in corporate-bond CEFs.

Let’s keep at it now by zeroing on two corporate-bond CEFs that are still undervalued—though one much more than the other. On average, they yield north of 9%.

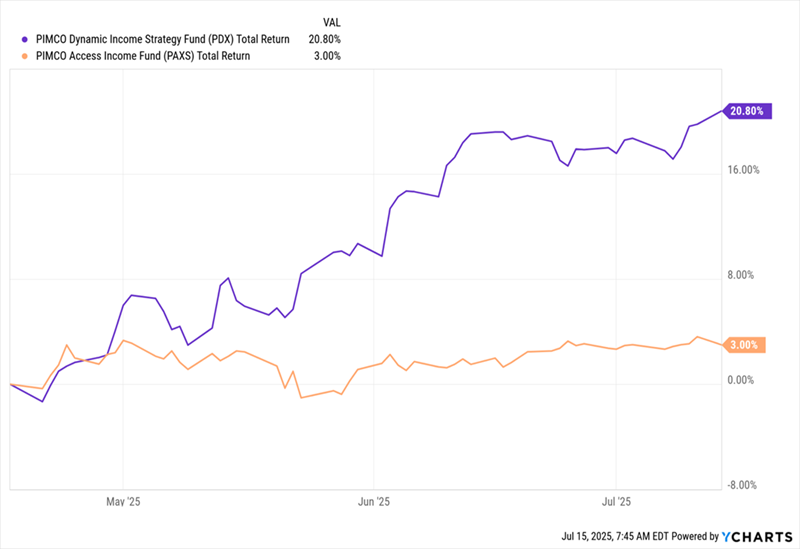

I mention the April tariff crash for a reason: In an April 17 article (published as trade confusion reigned), I focused on two oversold PIMCO corporate-bond funds that, at the time, yielded 10.1% between them. Those were the PIMCO Dynamic Income Strategy Fund (PDX)—currently a holding in our CEF Insider service—and the PIMCO Access Income Fund (PAXS).

Since April 17, PAXS (in orange below) and PDX (in purple) have bounced, posting a nearly 12% average total return, based on their market prices. But the gains have been lopsided.

PIMCO Funds Surge (With PDX Leading)

We’ll talk about that gap more in a second. First, let’s dig into the dividends, since they’re usually investors’ No. 1 reason for buying CEFs.

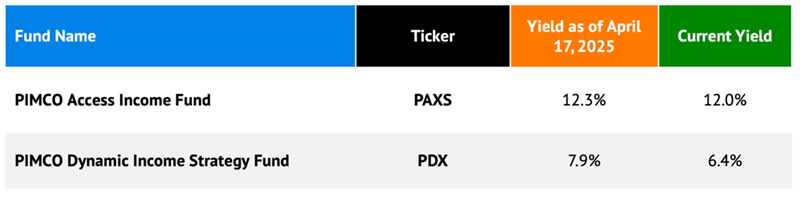

If you’d bought these CEFs on April 17, you’d have gotten a 10.1% average yield. Here too, the gap was quite big between the funds, with PAXS yielding over 12% at the time.

Note that these funds’ average yield has fallen due to price gains (as prices and yields move in opposite directions), though PAXS’s yield is still near where it was in April, at 12%. In other words, the fund’s smaller market-price gains mean it still offers a lot of income.

This is takeaway No. 1 in CEF investing: The higher yielder isn’t always the bigger short-term winner. In fact, it’s often the opposite: Many investors fear all big yields—even many CEF investors. (There’s really no excuse for that, since many CEFs have offered 10%+ yields for years without major payout cuts).

As a result of that fear, lower-yielding CEFs tend to bounce higher than bigger payers after a market panic. So PDX’s outperformance is no surprise. But there’s something else going on with these funds’ net asset values (NAVs).

NAV is a measure of a CEF’s portfolio performance: Since CEFs have fixed share counts, their NAV and market-price performance usually differ. A market price below NAV results in the “discount to NAV” that we CEF buyers covet.

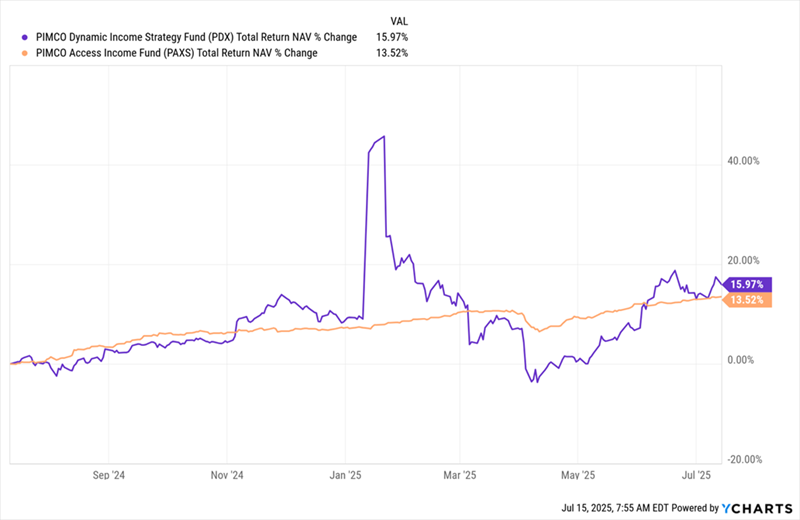

PDX’s Portfolio Edges Out PAXS

Over the past year, PAXS (in orange above) and PDX (in purple) have posted similar total NAV returns, with PDX edging ahead. That’s not too surprising, as both funds invest in a mix of credit assets and have overlapping management teams.

However, some aspects of PDX’s portfolio, like a focus on energy and oversold floating-rate credit, drove its outperformance (including that spike in early 2025) at different times over the last 12 months. In the future, we can expect both funds to keep recovering, mainly because of their discounts to NAV.

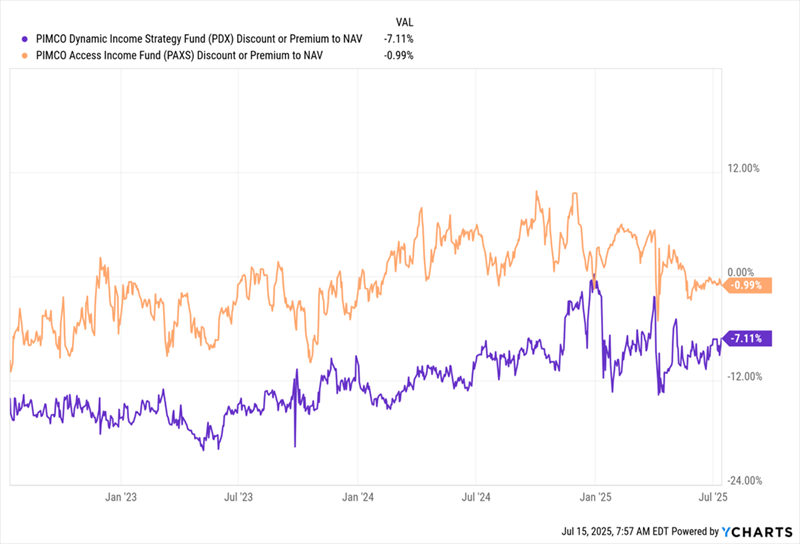

PDX, PAXS Discounts Bubble Away

Both funds trade at discounts as I write this, with PDX’s markdown being much bigger, at 7.1%. That makes the fund the more appealing choice between these two, even with its lower yield.

I expect PDX’s closing discount to result in a bigger total return than we’d get from PAXS in the long term, even if that discount is rangebound today. However, PAXS isn’t a bad fund, with the market’s continued gains spurring a bigger appetite for risk and income. As more investors look to CEFs, we should see more demand for those with the highest yields, and 12%-paying PAXS is nicely set up to benefit from that.

PAXS’s portfolio mix of leveraged-credit investments should allow its NAV to keep climbing in a rising market. That, in turn, would attract more investors and bring the fund’s tiny discount to a premium. This wouldn’t be unprecedented, since PAXS was trading at a double-digit premium less than a year ago.

In fact, a premium is likely for both funds in the longer term, since they both operate under the PIMCO name, and PIMCO CEFs tend to trade at large premiums.

There are lots of reasons for this, including the fact that investors generally don’t like to sell PIMCO funds because they often do outperform, and the company aggressively courts the ultra-rich in California via wealth managers.

As a result, many shares of these funds sit in accounts and aren’t traded very much. In the past, in fact, I’ve seen premiums on PIMCO funds shoot as high as 40%!

Could PAXS or PDX see that type of premium? It’s possible, though it will likely take years—though these funds’ current high payouts would make the wait a pleasant one.

5 Cheap Monthly Dividend Funds Paying 10.2%

These 2 bond CEFs are far from the only bargain income plays available now. Truth is, there are bargains aplenty across CEF-land.

Yes, even in today’s overinflated market!

Better yet, most CEFs pay dividends monthly, so we’re NOT waiting around for our next payout. We get our “dividend paycheck” every few weeks!

I’ve uncovered 5 monthly paying CEFs that are throwing off reliable payouts now—and their yields are no slouch, either: an incredible 10.2% on average today!

These 5 “battleship” funds are my top picks in monthly paying CEFs. They throw off steady cash whether the market is melting up or melting down—and you can collect your first payout within a few weeks of buying in!