The stock market is way up – and ironically, that’s terrible news for us dividend investors. Yields haven’t been this low in decades! The S&P 500 pays a measly 1.8% today. If you have a million-dollar portfolio, that’s a lousy $18,000 per year in income. Pathetic.

Most people invest their money in index funds like those that mimic the S&P 500. We can do better – four-times better, to be specific – and raise our dividend income by 400% simply by selling these mainstream plays and buying bigger payouts that are better values.

Specifically we’re going to discuss stocks, bonds and funds that pay 7.3% to 8% instead of the broader market’s lame 1.8%. That’s $73,000 to $80,000 in passive income on a million bucks, or up to $40,000 annually on $500,000. (Versus $18,000 and $9,000 per year – an easy choice.)

But first, let us show you the logical – but wrong – assumption that most mainstream dividend investors make.

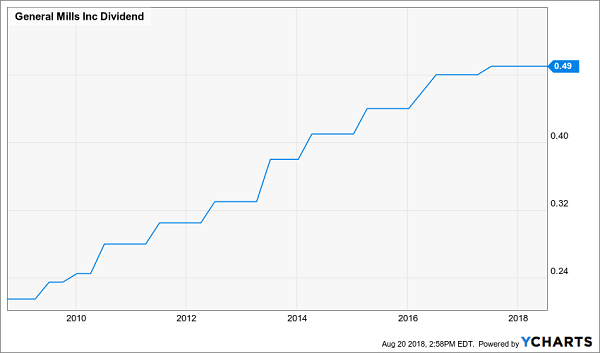

They look at a “consumer staple” like General Mills (GIS), see it yielding a “generous” 4.3%, and think it’s a good buy. The problem is that anyone who bought this “safe” stock two years ago has suffered a 36% price decline:

Not Enough Dividends to Cushion This Decline

Unfortunately these investors bought the wrong chart for investment income. They wanted the stock’s payout, but were streamrolled by the stock’s price decline while they waited.

Wouldn’t it be nice if you could collect the dividend without the price risk? For example, General Mills’ dividend never goes down. Isn’t this a better bet for retirement income?

Too bad the dividend-only chart isn’t for sale! It is, after all, what gives companies their reputations as “dividend aristocrats.” You can count on their dividends so much that they become “must have” stocks, revered royalty.

General Mills isn’t really a “must have” stock anymore, though. Sagging demand for Cheerios and Green Giant Peas have weighed on its profit (and hence, dividend) growth in recent years. As they’ve slowed down, so has the stock price.

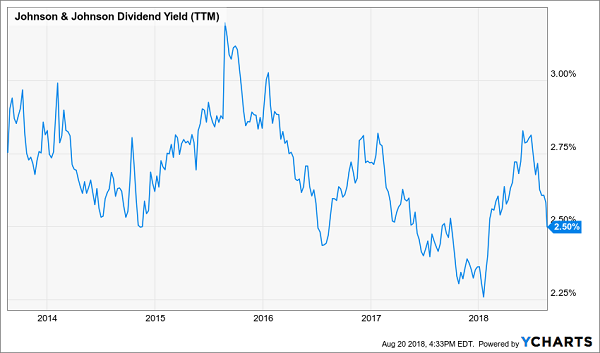

Unfortunately even still-robust aristocrats have their issues as retirement picks too. Let’s take Johnson & Johnson (JNJ), which has nearly doubled its dividend over the last ten years (+96%). Shares pay 2.5% as I write, but they’re also 2% lower year-to-date.

There Goes Your Yearly Dividend

Again, to buy JNJ’s dividend staircase, you end up buying its manic price chart. And sure, there were great times to buy Johnson & Johnson for profits, such as when the market ripped off its Band-Aid in the 2008-09 crash and the stock paid 3.8%. But can we really sit in cash and wait for the next financial crisis to present us with a buying moment?

For most of the last five years, Johnson & Johnson has paid between 2.25% and 3%. Unless you’re rich, this investment doesn’t generate enough income to fund a comfortable retirement. (Remember, a 3% yield only generates $30,000 in dividend income on a million dollar position.)

JNJ Rarely Pays Much

The problem with this stock is that it’s always expensive on a valuation basis. The downside stock risk is greater than the benefit of the dividend. Which means you’re exposing yourself to short-term price risk to collect a 2.5% dividend.

There are two issues with this approach.

Firstly, you’re putting your retirement portfolio in the way of a potential stock market crash (which will take down Johnson & Johnson too) in order to collect the income it pays investors. And in the conventional wisdom of annual 4% withdrawals, you’re selling more shares at exactly the wrong time (when the price is low!)

Bottom line, if you’re after dividends, this purchase isn’t worth the risk for a stingy 2.5%! Even if you buy $1 million in shares in the baby shampoo god, you’re only collecting $25,000 in income annually. That’s less than your neighborhood coffee barista earns – and you probably didn’t save and invest your entire life to sling lattes to supplement your retirement lifestyle.

This is the problem with investing in dividend aristocrats like these – companies that have increased their dividends for at least 25 consecutive years – is that they’re already considered the highest quality companies in the world. Which means their stocks are almost always expensive, and their current yields are usually quite modest.

Tempted to hang about waiting for these dividend aristocrats stocks to go on sale? They rarely do and waiting can be hazardous to your health. You are paying the “opportunity cost,” which is what you could have earned by investing it better elsewhere.

(Remember, Johnson & Johnson hasn’t been on sale in ten years – and even in the depths of the financial crisis, the stock still didn’t pay 4%.)

Well, you might say, “You just have to choose the right aristocrats.” Unfortunately, it’s not a matter of dividend aristocrat-picking prowess either. They’re usually overpriced (a function of their popularity and automatic inclusion in exchange traded indices).

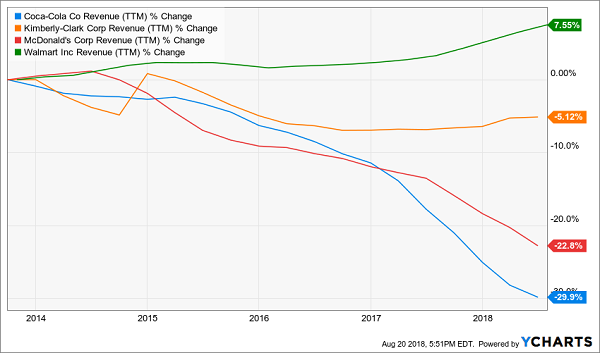

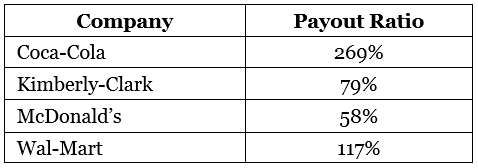

Let’s take four more blue chip “dividend aristocrats”: Coca Kola (KO), Kimberly-Clark (KMB), McDonald’s (MCD), and Wal-Mart (WMT). To say their best growth days are behind them would be kind. Check out their flat-to-declining sales trends – it is difficult to declare a dividend safe when the business behind the payout is struggling:

Sales Challenges for This Royal Bunch

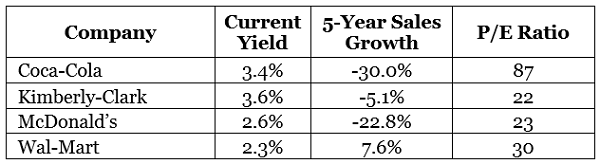

You’d never guess these firms were having sales struggles by looking at their valuations. Let’s consider their price-to-earnings (P/E) ratios, which look quite pricey considering these uncertain growth prospects:

These P/E ratios not only reflect investor convictions in growth (as the companies offer little) but also misplaced belief in safety (yes, they’ll likely be around come what may, but not at these prices). Is this worth a 4-stock aristocrat portfolio that only pays an average 3.0%? I think not.

And this is after taking into account dividend growth. Over the past decade, these four companies have boosted their payout ratios (the percentage of earnings they pay as dividends) to support their aristocrat status. Sure, their dividends are growing, but they can’t do it forever by increasing the amount of their extra cash they dish out (that’s the payout ratio). All four exceed my “half profits, half payouts” rules of safety today (meaning I prefer to see this ratio under 50% – and certainly under 100%!):

Look at what this means. Your $1 million portfolio will only earn you $30,000 in dividend income annually invested in these shares, but you think, “If I hold along enough, that 3% on my original investment will grow.” But the dividend growth is iffy.

These companies’ best days are behind them. If they weren’t, the payout ratios would stand still or even decline while the dividends grow. That’s not the case for our four companies.

Let me repeat. A $1 million portfolio will only earn you only $30,000 in dividend income annually invested in these shares. A million bucks invested this way gets you a Californian $15 minimum wage in retirement. And it’s not even that secure.

The 8 Best 8% Dividends with Big Upside to Buy Today

Most Wall Street spreadsheet jockeys say we investors can’t have both the income and safety of bonds and the upside of stocks. We have to choose, or allocate, or whatever.

They’re wrong. My 8% “no withdrawal” retirement strategy lets retirees rely entirely on dividend income and leave their principal 100% intact.

Well that’s not exactly right. Their principal is more than 100% intact thanks to price gains like these! Which means principal is actually 110% intact after year 1, and so on.

To do this, I seek out stocks and funds funds that:

- Pay 7%, 8% or better…

- Have well funded dividends…

- Trade at meaningful discounts to their intrinsic values…

- And know how to make their shareholders money.

And I talk to management, because online research isn’t enough. I also track insider buying to make sure these guys have real skin in the game.

Today I like three “blue chip” funds as best income buys. And wait ‘til you see their yields! These “slam dunk” income plays pay 8.5%, 8.7% and even 8.9% dividends.

Plus, they trade at 10-15% discounts to their intrinsic values today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch issues will simply trade flat… and we’ll still collect those fat dividends!

If you’re an investor who strives to live off dividends alone, while slowly but safely increasing the value of your nest egg, these are the ideal holdings for you. Click here and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my three favorite closed-end funds for 8.5%, 8.7% and 8.9% yields.