Look, I know what a pain it can be to track your dividends.

ChatGPT? It’s no help. When I asked if it could give me a hand, its top suggestion was that I use a spreadsheet!

I mean, I guess the offer to help set up formulas is appreciated. But this is still a pain to set up—with AI assistance or not.

Sure, your brokerage account might have a built-in dividend tracker, but it’s almost certainly only useful for any investments you hold with that particular broker.

But what if you hold investments in more than one account, or with more than one brokerage (as many of us do)? Or maybe you want to project income from an investment you don’t own (yet) but are considering buying?

For those situations, brokerage-run apps are clumsy at best. Useless at worst.

There are a bundle of “outside” apps out there, too. But switching to one likely means manually entering your tickers and/or learning a whole new system. No thanks!

Truth is, all of this sounds like a J-O-B. And we want no part of that. We’re retired (or at least aspiring to be)!

Know What You’re Getting Paid—and When—With Income Calendar

Here at Contrarian Outlook, we’ve tried a lot of different dividend-projection tools, and we didn’t find any we loved (or even liked much). So we went ahead and created our own—exactly how we want it.

It’s called Income Calendar and I’m focusing on it in today’s article to let you know we’ve recently beefed it up with some new features that make it very easy to use, including the ability to connect to any brokerage. Even Fidelity!

No more flipping back and forth between screens to input tickers. And definitely no more spreadsheets. Instead, IC simply links to your brokerage account and inputs all tickers and share counts automatically.

I had my Schwab account connected in just a few clicks when I tried it. And that’s just the start of what IC can do.

Let’s take a walk through this beefed-up tool with a ticker subscribers to my Contrarian Income Report service will recognize: Ares Capital (ARCC).

ARCC is a business development company (BDC), a class of firms that lend to small businesses. It’s a prime pick for what I call the “no-landing” economy.

A key thing to keep in mind about BDCs is that they get special tax privileges. In exchange, they must return at least 90% of their taxable profits to shareholders as dividends. They trade just like regular common stocks, with tickers we buy and sell.

The tax savings mean more money available to send out to us as dividends, juicing the yields on these stocks. ARCC pays an outsized 9% dividend today.

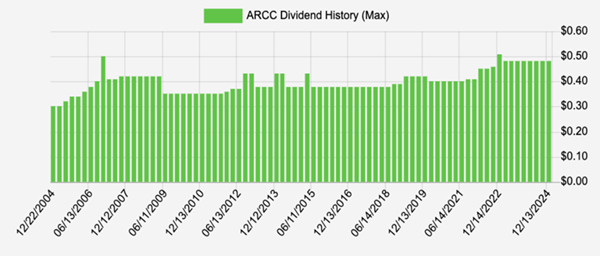

On the dividend front, the company’s $2.39 a share earnings in the last 12 months easily covered the 48-cent per share quarterly payout (or $1.92 over the 12-month period). An 80% payout ratio is great in the land of BDCs.

And about that dividend: Ares not only yields 9% but has a history of hiking its payout, too. I know I don’t have to tell you that a 9% payout that grows is a rare bird indeed.

Look at this chart, generated through, you guessed it, Income Calendar:

A Rare 9% Dividend That Grows

Source: Income Calendar

The “bump” at the end of 2022 was a special dividend. Ares keeps a “spillover” of extra earnings that it pays out to shareholders periodically, or it may choose to keep these funds on hand for a rainy lending day.

That high, and growing, payout makes ARCC a great candidate to track through IC, so let’s go ahead and do that.

ARCC’s Dividend Can Be a Pain to Track (Unless You Use This Tool)

Through Income Calendar, we can instantly forecast when (down to the day) and how many (down to the penny) dividends our portfolio will kick out in the week, month and year ahead.

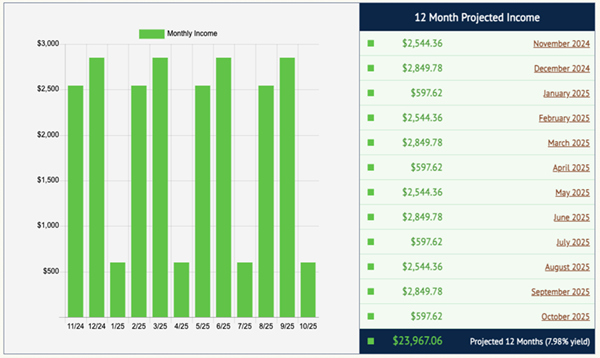

Let’s plug ARCC into Income Calendar, along with a couple other high-paying CIR portfolio holdings—the Alerian MLP ETF (AMLP), with a 7.8% yield, and the monthly paying AllianceBernstein Global High Income Fund (AWF), current yield: 7.2%.

Let’s say we invest $100,000 in each of these three high payers. Income Calendar tells us, immediately, what we can expect in terms of dividends every month from our 3-buy “mini-portfolio”:

As you can see, with just these three buys, we’ve got dividends ranging from $597.62 all the way up to $2,849.78, and a total of $23,976.06 in dividends on the year, on just $300K invested. Sweet! (Bear in mind, too, that to be overly conservative, we don’t project dividend growth here, so our “real” payouts could be higher.)

You can get complete breakdowns by stock, plus a month-by-month calendar giving you a heads-up on earnings dates, ex-dividend dates and other critical periods for every one of your holdings. Instantly!

Check it out. Here’s what our 3-buy portfolio shows us for December, one of our highest-paying months:

We can see our projected pay dates, as well as ex-dividend dates (the dates before which we need to be “in” the stock to get the next payout) and even things like market holidays.

We even get a heads-up on when our stocks are due to report earnings—though there are none of these for our trio in December (understandable, due to the holiday season).

So long, spreadsheet. Hello, extra time.

There’s more, too, like real-time email alerts every time a dividend drops into our account, a “week-ahead” summary telling you exactly how much we’ll get paid and when, a handy tool that instantly tells you your “yield on cost” (so you can see the “true” yield on each of your stocks, based on the timing of your original buy) and more.

Click here and I’ll tell you more about this powerful dividend planner and give you the opportunity to “road test” it out for yourself. I’m sure you’ll love it.