A stock’s current yield holds an almost untouchable place in most investors’ minds. But here’s the thing: it’s lying to you.

My take: you’re much better off going by a company’s shareholder yield, which tells the full story on the payout we get.

Shareholder what?

We’ll get into exactly what shareholder yield means for us in a second. But we first need to look at how going by a stock’s current yield alone can steer you into a ditch.

Lumen Technologies Shows How a High Yield Can Be a Trap …

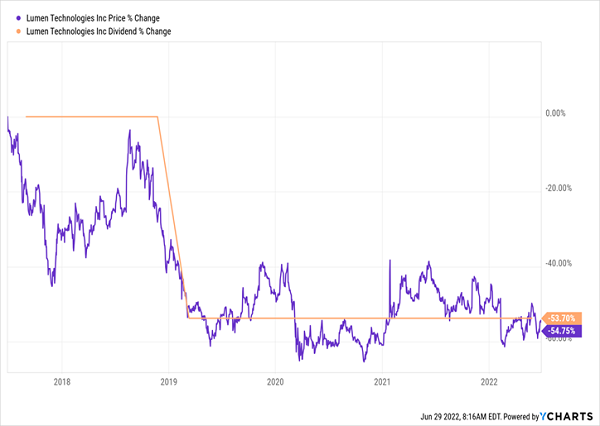

Consider regional telecom operator Lumen Technologies (LUMN), which we discussed last week in our third article on my proven “Dividend Magnet” investing strategy.

The stock sports an 8.9% current yield, which sounds pretty sweet: buy it now and you get nearly 10% of your investment back every year in cash.

But you don’t have to dig too deep to discover that this high yield only exists because Lumen’s share price has been decimated (as current yields and share prices move in opposite directions). As you can see below, Lumen is a serial dividend cutter, and its price has been falling with its payout.

A 9% Yield Is Cold Comfort When Half Your Money Is Gone

This is the Dividend Magnet working in reverse! It’s a disaster for anyone who was lured by Lumen’s “high” current yield.

… And a “Low” Current Yield Can Mask an Opportunity

The sad thing is that most folks who fall for traps like this damage their portfolios twice over. That’s because, while they’re often lured by sucker yields like Lumen’s, they ignore strong dividend stocks because they see their current yields as “too low.”

Let’s stop here for a moment, because this is where the rubber really hits the road on my dividend-growth investing strategy.

A dividend stock, at the end of the day, has three ways to pay us:

- Its current dividend payout: This, of course, is the dividend we get after we buy.

- Dividend growth, which increases the yield on our original buy and acts like a “magnet” on the share price, with the rising payout pulling the stock higher.

- Share buybacks, which cut the number of shares outstanding, juicing earnings per share and other per-share metrics (which tends to lift the share price).

Buybacks often get a bad rap, but they shouldn’t, because when they’re done right (i.e., when the stock is cheap), they can seriously juice our return. This is another problem with the current yield—it tells us nothing about this buyback effect.

Shareholder Yield Combines Dividends and Buybacks

This is where my preferred “yield”—shareholder yield—comes in. It includes buybacks and dividends to give us a more complete picture of what a stock is really paying us.

To see it in action, let’s consider Reliance Steel & Aluminum (RS), a name that members of my Hidden Yields service will recognize. Reliance is a California-based company that offers more than 100,000 metal products in various shapes and sizes.

Right off the bat, most folks would turn up their noses at Reliance due to its “low” current yield of 1.8%, only a hair above the S&P 500 average. But let’s ignore that for a second and factor in Reliance’s payout growth, which has been spectacular. You can see its Dividend Magnet in action, too:

Another “Dividend Magnet” Goes to Work

If you have any doubts that a rising payout is the No. 1 driver of share prices, this should put them to rest. The pattern is unmistakable! And because of that growth, folks who bought Reliance a decade ago (before we launched Hidden Yields) don’t care about today’s miserly 1.8% payout: they’re yielding a stout 7% on their original buy!

This is, hands down, the safest way to get a high yield from a stock.

Now let’s move on to buybacks: Reliance has taken 18% of its shares off the market in the last decade, making everything look better on a per-share basis, including earnings per share, free cash flow per share and dividends per share. All of those factors feed straight back into explosive dividend- and share-price gains we just saw in the chart above.

How to Calculate Shareholder Yield

The formula for figuring out a company’s shareholder yield is simple: take the amount spent on share repurchases in the preceding 12 months, deduct any cash brought in through share issuances, then add in the total spent on dividends.

You then take that sum and divide it into the company’s market cap, or the value of all its outstanding shares.

In Reliance’s case, that comes out to $188.9 million spent on dividends and $340.6 million spent on buybacks, for a total of $529.5 million in total shareholder returns in the past 12 months. With a $10.6-billion market cap, we can say that Reliance sports a 5% shareholder yield—much more than the 1.8% current dividend yield you’ll see on most screeners.

Don’t Face This Volatile Market Alone: Get the Reliable Income You Need Now

I’m constantly updating members of my Hidden Yields service as this market transition continues, and I want to help you ensure your portfolio is safe, and primed for long-term growth, too.

Click here and I’ll give you my full dividend strategy and show you how to get a no-risk 60-day trial to Hidden Yields. Your trial includes my take on whether Reliance can keep up its dividends and buybacks, my latest buy/sell/hold advice on the stock, and instant access to my full Hidden Yields portfolio of reliable dividend growers.

That’s not all: I’ve also prepared a Special Investor Report that reveals the 7 stocks I fully expect to return 15% annually, year in and year out over the long haul.

Those gains will, of course, be powered by these firms’ powerful Dividend Magnets, plus share buybacks that give your returns—and your shareholder yield—a nice extra kick. Buy these stocks now and you can tuck them away forever.

Don’t miss this opportunity. Go right here and get your free trial to Hidden Yields (including my latest advice on Reliance), which comes with that Special Investor Report including my top 7 dividend-growth stocks to buy now.