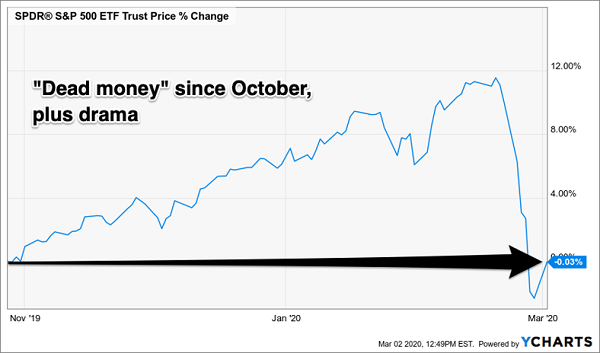

Have four months of “dead money” ever caused this much drama?

Let’s put last week’s pullback in perspective. As uncomfortable as it may have been for investors who watch the market daily, it simply served as a public service reminder that most investors are probably better off not watching the market daily.

The result of one of the worst weeks in Wall Street history? A mere return to late October 2019 price levels:

Wall Street’s Tower of Terror

Typically, an erasure of four months’ worth of gains wouldn’t be a big deal. However, this stock market had been unusually bullish, gaining nearly 12% in less than four months. These kinds of gains are typically not sustained over time, and last week was a reminder that “buy and hope” gains can be given back quickly.

Stock drops are dangerous for the buy and hope crowd. After all, they must grow yet also preserve their capital, a dual mandate that puts them behind the 8-ball when precipitous falls occur. They withstand some losses and then get scared into selling at the worst possible moment.

However, these meltdowns are actually good things for us income investors.

With stock prices lower today than they were just two short weeks ago, we can secure more dividend for our dollar with each purchase we make. This obviously applies to cash that we’ve been waiting to put to work. But don’t forget, it also applies to dividends that are ready to be reinvested.

For those of you with retirement portfolios filled with quarterly and even monthly payers, there’s always another dividend check on the way. These payouts are going to net you more shares than they would have just 14 days ago and, over time, this advantage adds up.

“But Brett,” I can hear some saying. “Shouldn’t we keep our cash in cash until the current pullback is over?”

If your crystal ball works better than mine, then sure, keep that powder dry. Unfortunately, I’m not aware of any timing mechanism that picks the bottom of pullbacks (or bear markets, for that matter) with pinpoint accuracy. The best we can do is play the probabilities.

Most “permabears”—analysts and investors who are always waiting for the end of the world—underperform. (Even when they get it right!) They flip to cash early and, even if they haughtily sit out the downturn on their pile of money, they never quite know when to get back in.

Know anyone who has been sitting on a portfolio of too-much-cash since 2009? They missed an epic bull market.

Now, I admit it’s late in the financial cycle. Problem is, as we mused a few weeks ago (just prior to the virus-driven meltdown), nobody really knows what time it is in the stock market rally.

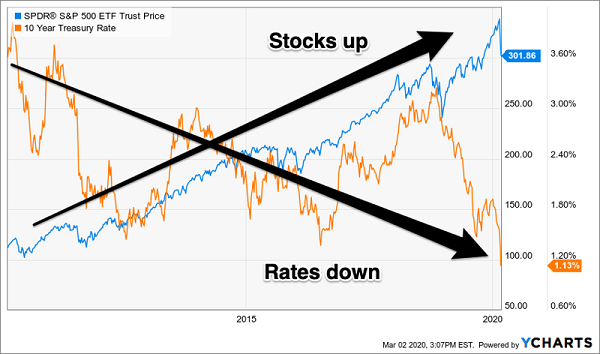

What I do know is that there are two “big picture” trends in place:

- Stocks are still in an uptrend, as they have been since 2009. And,

- Interest rates continue to circle the bowl. In fact, US bonds hit their lowest all-time yields last week! This news was largely overshadowed by the stock market’s hysteria:

Big Picture: Stocks Up, Rates Down

Now, I don’t bring up these trends because I confuse us for “trend followers” who like to buy high and sell higher. But it is clear, from the chart above, that financial trends are indeed “a thing” over long periods of time, and it is important to stay aligned with them.

For the past 11 years, this has meant owning stocks and fixed-rate bonds. Which brings me to our bargain shopping list. Some bonds irrationally went on sale last week!

On paper, this shouldn’t have happened. Our bond funds should have sailed through the pullback. After all, with rates moving lower and lower, this made the portfolios of our funds more and more valuable.

But fear, as it usually does, struck our otherwise happy little land of CEFs (closed-end funds). These vehicles of modest market caps are held largely by individual investors, who are considered the “weaker hands” in the markets. They sold in a panic last week, and many perfectly good CEFs shed price.

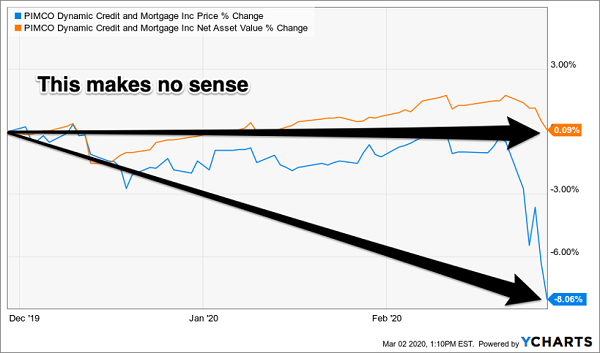

Don’t be fooled by their price declines. As I’ve said before, it is all about the NAV, or “net asset value” of a fund’s underlying portfolio. If you see a panic that causes a price to drop, while the NAV doesn’t flinch, buy the fund.

For example, let’s look at the PIMCO Dynamic Credit and Mortgage Fund (PCI). My Contrarian Income Report subscribers know PCI well, as we’ve enjoyed 8% to 9% dividends that have added up to 91% total returns since we bought this income machine during the panic of 2016.

PCI’s NAV has held up just fine during the recent market volatility. This is a sign that the fund’s 8.9% dividend is “well covered” by income plus capital gains.

However, PCI’s price, which trades like a stock and is subject to the whims and day-to-day insanity of market buyers and sellers had, by the end of last week, “diverged” from its NAV by 8% to the downside:

Temporary Market Insanity

Again, this might appear “bad” to someone who buys a fund like PCI, stares at it regularly and hopes it ticks up every single day. However, it is great news to calculated income seekers like you and me, as we are simply looking to maximize our dividend per dollar invested.

PS – I’ve got my eye on 5 “pullback-proof” dividends in particular that are paying up to 9.8% today. These income machines didn’t budge much last week, which shows they are really ready to take off if and when the bull market resumes.

That said, who knows. Could we see a retest of last week’s lows? Typically, in a pullback that extreme, we would see a retest and potentially another sharp leg down.

If this happens, will you have the stomach to stay in your stocks?

If the sound of another 14% down makes you a bit nauseous, I’d recommend this 5-pack of pullback-proof payers to calm your stomach and meet your income needs. Click here for my full analysis and 5 favorite dividend plays today.