Hedge fund veteran and Wall Street-approved suit Scott Bessent is likely the new Treasury secretary. That’s why this 11% dividend is a big winner.

Bessent will advocate for financial deregulation and increased lending. Easier and faster money. Which will be a boon for private equity and business development companies (BDCs).

Prior to Bessent’s appointment, the folks in Silicon Valley were already salivating over increased M&A: Big companies tossing money at startups and private firms raising piles of dough to get in on the action itself. That’s the rocket fuel that mints multi-millionaires and even billionaires.

This extra cash sloshing around will make inflation sticky. It already is. Bessent’s buddies on Wall Street will not receive as many rate cuts as they had hoped for as recently as September.

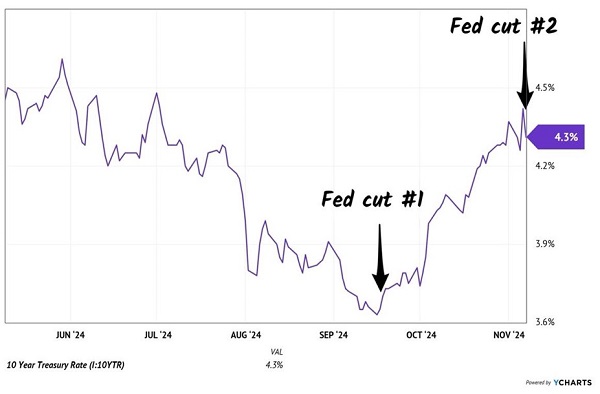

The bond market has already protested to Fed Chair Powell that these cuts were not really needed. The 10-year yield has risen (from 3.7% to 4.3%) with each dovish decision, a signal that cuts now will keep inflation around longer tomorrow:

The 10-Year Yield Irony

This is a challenging environment for bond investors. Bond prices tend to move opposite interest rates, especially long-duration fixed income. As the 10-year yield rises, bond prices come under pressure.

The long end of the yield curve is rising while the short end is shrinking. This “de-inversion” of the previously inverted yield curve is the bond market backing off its prior “recession call.” (An inverted yield curve means bond investors see lower yields ahead than today, consistent with the Fed lowering rates to combat a recession.)

Easy money is here. Buckle up.

It’s a tough time to be a bond but this is an ideal environment for business development companies (BDCs) and their big yields. And we could talk specifics, but let’s keep it simple—VanEck BDC Income ETF (BIZD) is a simple, effective way to play this trend.

And bank an electric 11% yield that is buoyed by Bessent!

BDCs lend to small businesses—you know, like traditional banks used to. These days it is nearly impossible to get a business loan from a bank, so BDCs stepped in to fill the gap, providing debt, equity, and other finance solutions to small businesses.

Congress created BDCs in 1980. They receive special tax privileges in exchange for returning 90% of their taxable profits to shareholders as dividends. (Sound familiar? It’s the same deal REITs enjoy.)

BDCs operate like private equity (PE) firms. Both will benefit from a friendly deal-making environment. For our purposes, we choose BDCs because it is easier to buy them.

PE shops typically require a minimum investment of at least six figures and often into the millions. But we can buy BIZD with a $20 bill and receive change. Even a crumpled-up bill will do!

We can buy BDCs individually as we would any stock. But given the bullish backdrop, I like BIZD as a one-click way to get industry exposure and collect an 11% dividend that is diversified across 29 companies.

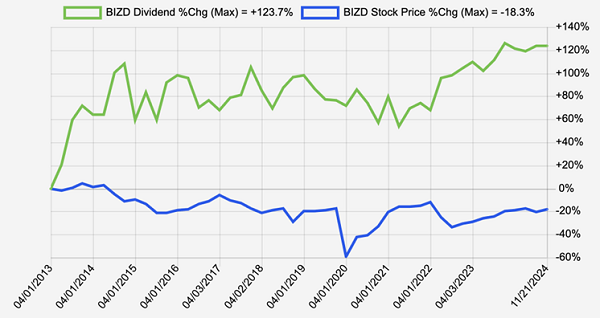

Over time, BIZD tends to do better as a trade than a long-term buy and hold. Sure, the fund has doubled its dividend (+124%) since inception. Problem is, it shed 18% in price over the same time period:

BIZD Dividend +124% Since Inception

On a total return basis, BIZD sits 147% higher. The big dividends add up! Still, we should time our entries and buy BIZD when the rising tide is set to lift all boats in the sector.

Why the price volatility in this ETF? There are some poorly run BDCs. See: Prospect Capital (PSEC), a regular target in these pages! Over the last three years, PSEC has lost its investors 25%—including payouts. The company has paid a large dividend but lost more in price. Not ideal!

But the sun will even shine on this dog’s behind under Bessent. I don’t have the stomach to buy it straight up, I’ll take it in a basket with 28 other BDCs likely to rally.

The private lending party is on. After all, we have a hedge fund bro heading the Treasury and Powell spiking the punchbowl!

Meanwhile, Uncle Sam is buzzing with deficit spending to keep the party going. The new department of government efficiency (DOGE) won’t dent the current fiscal deficit, which is an all-timer. The Congressional Budget Office (CBO) projects a $1.9 trillion deficit on $4.9 trillion in tax receipts. (Worse, this is the CBO that paints its projections with rose-colored ink.)

So, we have nearly $5 trillion in revenues, and almost $7 trillion in expenditures. A 40% overshoot.

Give me an extra $2 trillion, and I’ll show you a good economy, too! Small business financing is back. And BIZD is here for it. Let’s take the 11% yield and ride the deal-making rager.

This is the type of dividend payer that allows us to live off of a modest sum like $500K practically… forever. The math is great! Put $500K in BIZD, bank $55,000 in yearly dividends.

And keep your principal intact!

But this isn’t ideal from a diversification standpoint, of course. Sure BIZD owns 29 stocks, but they all trade directionally similar.

As retirees we want stocks that zig when others zag. However, we don’t want any dead weight on our 11% dividend party!

No problem–we can diversify into other big dividend payers by following my “$500K forever” plan right here.