Everywhere you look, there’s a subscription service begging for your attention: from Netflix (NFLX) to cable TV … and even a Hot Sauce of the Month Club.

Pretty well everyone has at least one, and many folks have several. One study showed that 7% of American households have six or more services for video alone!

There’s a reason why companies charge recurring revenues, of course. It’s a great business model to hit up our credit cards monthly.

But great businesses don’t always translate to rewarding stocks. We contrarian dividend seekers tend to steer clear of the streamers because:

- They pay no dividends!

- There’s zero certainty, despite their seemingly predictable revenue streams: I’m sure you know of folks who dial into a streaming service, binge their favorite show and then check out. You’ve likely done this yourself.

But there is another way for us to tap “recurring revenue” stocks for sturdy payouts that shrug off a market crash: we’re going to look for companies that are either tied to surging megatrends or forgo fickle consumers entirely and focus on much more reliable clients: other companies.

Corporate business is, after all, more “sticky”: once a company commits to a certain provider, be it for back-office functions, health benefits or cloud platforms, they tend to stick around. It’s just too costly and time-consuming to switch.

You can find the best “recurring revenue” buys by looking out for four “must haves” (besides a top-quality product clients can’t live without, of course!):

- A growing dividend, which tends to pull a company’s share price higher. In times of crisis, a rising payout is a sign of a healthy business, which draws frightened investors in.

- Rising profits (and better yet free cash flow, a snapshot of cash generation that can’t be manipulated) to back that rising payout and, in turn, our upside.

- A safe payout ratio: I demand that “regular” stocks (i.e., those outside the real estate investment trust market) pay no more than 50% of free cash flow as dividends.

- A large slice of its market, so there are fewer competitors to switch to!

Add all four together and you get an excellent shot at long-term profits (and rising dividends!). We saw this in action at my Hidden Yields service, when we bought cell-tower “landlord” American Tower (AMT) in November 2018.

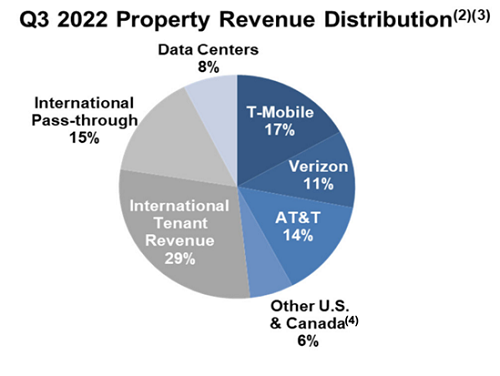

We’ve written about cell-tower firms like AMT many times in the last few years, and with good reason: for one, AMT, along with Crown Castle (CCI) and SBA Communications (SBAC) are basically an oligopoly that controls the nation’s cell-tower infrastructure between the three of them.

If you’re AT&T (T), Verizon Communications (VZ) or T-Mobile US (TMUS), you pretty well have to do business with one of the three cell-tower kingpins. AMT counts all three of the major telcos as “subscribers,” as you can see below.

Source: American Tower Q3 2022 operational update

And talk about “sticky” business: AMT’s leases are typically non-cancellable and run for five to 10-year terms, with yearly escalators built in.

We loved AMT because it’s a “pass-through” company, taking the revenue it collects from new leases and those yearly “escalators” and passing them on to investors in the form of a dividend that rises every quarter, just as it did through our two-and-a-half year holding period:

Soaring “Recurring Revenue” Translates Into Gains and Upside

As you can see, AMT’s soaring dividend (up 65% in just two and a half years) also pulled up the stock’s price, with a nice 48% increase in that time—a phenomenon I call the “Dividend Magnet.” The final tally was a nice 57% total return from one of the savviest recurring-revenue plays out there.

NextEra Energy: Another Strong “Recurring Revenue” Play

Utilities are the ultimate recurring-revenue stocks, and they’re recession-proof, too: because no matter what happens with the economy, the utility bill must be paid.

That’s a good reason to buy a stock like NextEra Energy (NEE). Plus, the stock matches up perfectly with our four “must haves”: on the market-share front, NEE’s regulated Florida Power & Light subsidiary is the state’s biggest utility, serving five million households.

NEE is also the largest developer of renewable energy in North America. This combo of steady income from its regulated operations and growth from the renewable side has translated into a dividend that’s soared 53% in the last five years.

In its latest quarter, EPS jumped 13%, and management says continued strong earnings will let the company juice its dividend by 10% annually at least through 2024, using this year as a base.

That strength is largely on the back of NextEra’s renewables pipeline: just from July to late October, NEE added 2.1 billion gigawatts to its backlog and is now sitting on about 20 billion worth. As these projects roll out, they’ll power NEE’s earnings, which is why the company expects those yearly 10% dividend increases.

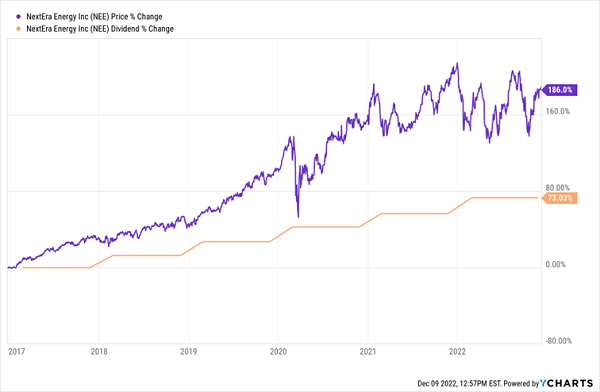

Now let’s talk about NEE’s Dividend Magnet, because it’s definitely worked its magic on the share price—in fact, it may have worked a little too well, as the price has more than doubled up the company’s share-price growth in the past five years:

NEE’s Share Price Overpowers Its Dividend

That’s not surprising, as NextEra is rarely “cheap” because everyone knows it’s a great stock. It does dip from time to time, though (back in May, for example, shares were down some 27% from January 1, compared to an 8% year-to-date decline today), so it’s worth keeping NEE on your list to buy on dips.

This Overlooked Dividend Grower Is the “Next” NextEra

Even though NextEra is currently a bit out of reach, price-wise, that’s not the case for a spinoff renewable-power company I’m pounding the table on today. It focuses on buying clean-energy projects like wind farms, solar farms and even natural gas assets with stable cash flows from long-term contracts.

I expect this pick, which yields about 4% today and has a surprising connection to NextEra, to deliver strong gains and dividend growth in 2023 and beyond, as more investors discover its outsized potential. The Biden Administration’s new clean-energy law should give its shares an extra kick, too!

This stock is in the portfolio of my Hidden Yields dividend-growth service, which I’m going to let you try under a no-risk 60-day offer today.

Once you’ve started your trial, just click over to the portfolio and you’ll see the stock I’m talking about there. Don’t miss out!