Most investors I speak to have no idea how much they’ll need to retire (and with the uncertainty we’re facing today, that’s totally understandable!).

So let’s talk about that—and focus on closed-end funds (CEF), totally overlooked investments that could let you retire on dividends alone, possibly on as little as $325K. That’s the ultimate way to get peace of mind these days, because you don’t have to worry about selling into a pullback to keep your income stream intact.

The Income Side

When calculating how much you’ll need to clock out of the workforce, you really only need to know three things:

- How much you’ll spend in your first year of retirement.

- How much your investments will return after you retire.

- How much you can safely withdraw from your portfolio in retirement.

The first question is perhaps the easiest—most people want to spend about as much in retirement as they did while they were working.

While retirees have lower costs on some things, notably work-related expenses like commuting, they also have higher costs for others, like healthcare. And while these don’t exactly cancel each other out, in the long run, retirees should expect a mix of private health insurance, Medicare and careful planning to keep their costs no higher than when they were workers.

So let’s assume you’ll want as much income in retirement as you have now. While you alone know that number, for simplicity’s sake, let’s consider a hypothetical average American, who needs to make $35,805 from their investments.

The Income Piece of the Retirement Puzzle

I haven’t pulled that number out of the air; it’s the median yearly personal income in the United States, so we’ll go with that for now, and work on delivering it through portfolio returns alone.

Investment Returns and Withdrawal Rate

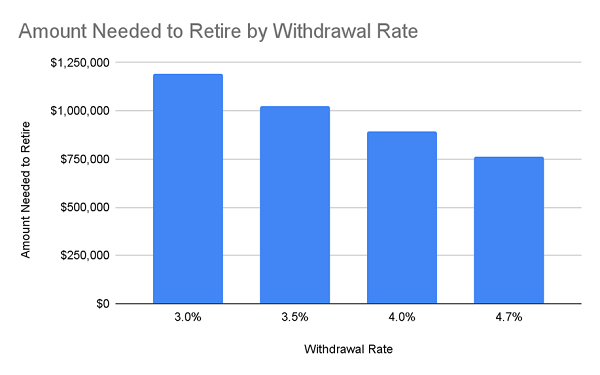

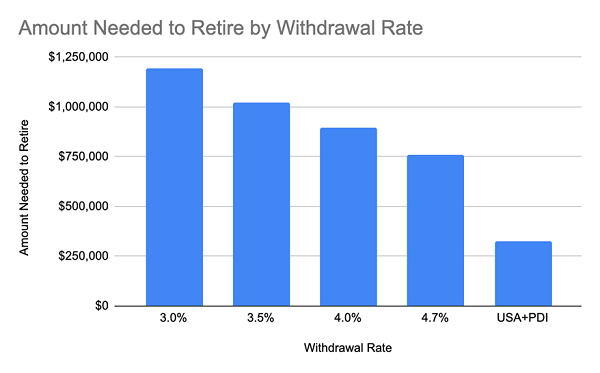

When it comes to getting an income stream in retirement, financial advisors have long used the 4% rule, which refers to the percentage of your portfolio you can safely withdraw every year. Hence it’s commonly referred to as the SWR, or safe withdrawal rate. Some advisers even suggest lowering it to 3.5% or 3%, although the actual inventor of the rule has more recently amended his own rule to 4.7%.

Source: CEF Insider

As you can see, this number is important; for those who go with 3%, over $1.1 million is needed to generate $35,805 in annual income, while the 4.5% rule demands a hair above $760K, which could still equate to many years of staying in the rat race!

The risk-averse might choose the smaller number, but there’s little reason beyond fear for such a decision. The inventor of the rule, retired financial advisor William Bengen, said that 4.7% looked like a safe rate for those who needed their nest egg to last 30 years.

More recently, Bengen has said 4.4% looks more realistic, due to the decline in stocks and bonds. That would mean a median income could be produced with $813,750 in savings, putting retirement years closer than the most risk-averse might suspect.

A New Withdrawal Rate to Consider

But for closed-end fund (CEF) investors, $813,750 is still overkill.

CEFs are, like mutual funds and ETFs, a group of funds that collect pools of money from investors and dedicate those funds to one group of assets or another. There are CEFs that hold stocks, bonds, commodities and real estate, among other sectors and subsectors.

But unlike mutual funds and ETFs, CEFs are dedicated to paying high dividends, with an average yield of 7.9% across the CEF market. Over a third of the CEFs have returned that much or higher on an annualized basis in the last decade (or since their IPO, whatever’s most recent). So many of these funds can produce enough of a rate of return and a dividend yield to sustain a retiree at a much higher withdrawal rate.

When you are managing your own portfolio of investments, the temptation to sell in market crashes is intense. That’s one reason why market crashes are as powerful as they are, because so many in the market sell, encouraging others to sell and so on.

We don’t want that; we want a fund run by managers who try to sell some of their holdings when stocks are overbought and give us our profits in the form of a cash payment, then buy more stocks when they’re oversold to sell again at the right time in the future.

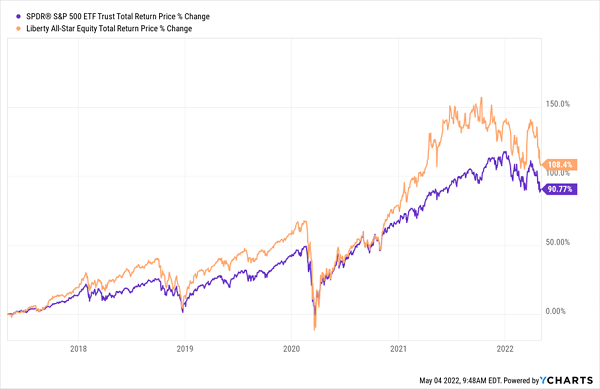

This kind of asset turnover is ultimately what CEFs aim to accomplish, and some do it well. Take, for instance, the Liberty All-Star Equity Fund (USA), a CEF I’ve recommended in the past. It’s far outpaced the S&P 500 in the last five years:

USA Runs Ahead of the Market

With a 13.8% annualized return over the last decade, outperformance over the last five years and a 10.4% current yield, USA has been a retiree’s friend. And CEF investors who buy USA when it’s trading for less than NAV can get even better returns; those are the times when the fund is most attractive (it trades at a 4.2% premium today, so you might want to hold off on this one until it dips into discount territory).

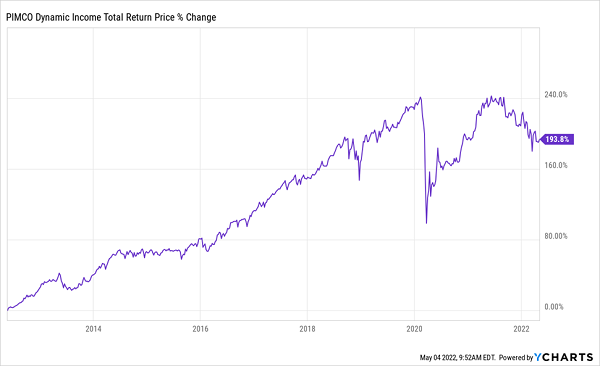

If you add the PIMCO Dynamic Income Fund (PDI), you have a two-fund portfolio of stocks and high-yield corporate bonds to diversify across asset classes. PDI yields 11.6% and has a strong history, returning 11.2% annualized over the last decade.

Another Top-Performing CEF

What does this mean for your nest egg? Between these funds, you have an average 11% yield, which means you can reproduce a median US income on dividends alone with just $325,500.

The Cheapest Retirement

Source: CEF Insider

The takeaway is that the best retirement option is to clock out on dividends alone, without touching your principal. That way, you don’t have to worry about selling stocks into a correction to keep your income stream level (which, by the way, is a key flaw of the 4% rule). You can simply collect your dividends—and turn off the financial news.

My Top 4 CEFs for Retirees Yield 7.5%, With Fast 20%+ Upside Potential

The only hitch with these two funds is that both trade at premiums to NAV right now, and I much prefer to buy at discounts to improve our upside (and more important these days, hedge our downside).

That’s why I recommend holding off on these two for now and going with 4 other CEFs I’m urging investors to buy now. They yield 7.5% today but the star attraction is their discounts, which I forecast will contract, propelling these stocks to an estimated 20% price gain in the next 12 months!

The best time to buy these stocks is now. Click here and I’ll reveal the details of my CEF investing strategy and show you how to get access to each of these tickers in a Special Investor Report I want to give you today.