What the heck happened last Monday? I know I don’t have to tell you that the market dropped off a cliff, only to float back higher as the week continued.

The media has been saying that it was all about the latest jobs report in the US, which came out on Friday and simply wasn’t that bad—certainly not the kind of result that deserves the response we saw from stocks.

To put it in perspective, the NASDAQ 100’s fall in a single day was worse than what we saw in the pandemic, when the global economy literally shut down.

Despite the rise in the unemployment rate, joblessness is still relatively low historically speaking, companies are defaulting less than a few months ago (and at historically low levels), and the US economy is set to grow well over 2% this year, after strong growth last year. So, a panic selloff makes no sense.

Until we look east.

Japan Grabs the Spotlight (in a Bad Way)

What happened to the US stock market is really the story of what happened in Japan.

In late July, the Bank of Japan raised interest rates, helping deepen a trend that had already been happening: the Japanese yen was recovering after getting weaker for a long time.

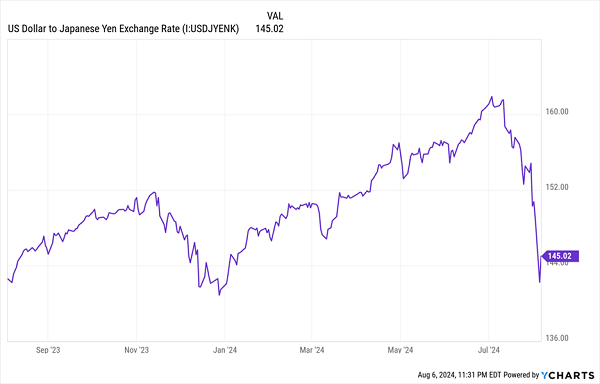

A Massive Drop

Note how the Japanese yen was slowly getting cheaper, until a dollar bought you over 160 yen, more than the 145 or so you could buy at the start of the year or a year ago? The cheaper yen is great for Japanese exporters and tourism, of course.

However, if the yen is too cheap, it can stifle domestic consumption, especially for imports, of which Japan’s biggest is energy. Those higher energy prices were flowing throughout Japan, causing inflation that the country’s citizens are very much not used to, foreshadowing a hit to economic growth. To prevent that, the Bank of Japan raised interest rates, and the foreign-currency market adjusted.

The only problem: it essentially adjusted in a day.

This was a shock in Japan, for sure, so it’s not surprising that the country’s stock market crashed over 10% in a day. But why would that spread further afield?

Many media outlets said this was because Wall Street is worried about America, drawing comparisons to the Black Friday crash of 1987. The reality is more complicated. The real worry on Wall Street on Monday was the so-called carry trade. It works in three steps.

Step 1: Investors borrow Japanese yen from a Japanese lender.

Step 2: They exchange those yen for US dollars.

Step 3: Finally, they use those dollars to buy US stocks and bonds.

If your stocks and bonds rise by more than 2% (the highest interest rate on margin loans in Japan, before the country’s central bank started raising rates), and if the Japanese yen doesn’t go up in value, you make an immediate profit. Even if it does go up in value, you can easily pay off your loan before it goes up too much, since foreign currencies tend to change slowly.

Well, most of the time, anyway. The kind of “off-the-cliff” move we saw with the yen is very rare, and it’s worrying because more people who borrowed yen to leverage bets on US stocks will become sellers, exacerbating the problem.

This didn’t actually happen last Monday. However, traders thought it was happening, and so they kind of made it happen on their own. This is unusual, but it does happen in financial markets from time to time, especially when a historic trend changes course. In this case, the shift came from the Bank of Japan, as this was only the second time it had raised interest rates in 17 years.

On Tuesday, more traders realized the yen carry trade, as it’s called, wasn’t actually the existential risk they thought it was, so stocks began to recover. But not fully, as the swift decline reintroduced fear to the markets.

All of this had significant implications for our favorite income plays: closed-end funds (CEFs).

In volatile times, a covered-call stock fund like the Nuveen S&P 500 Dynamic Overwrite Fund (SPXX) is often a good choice. The fund, which, as the name suggests, holds Visa (V), McDonald’s (MCD), UnitedHealth Group (UNH) and all the other S&P 500 names, generates extra income (and supports its 7.6% dividend) by selling call options, whose value goes up with volatility.

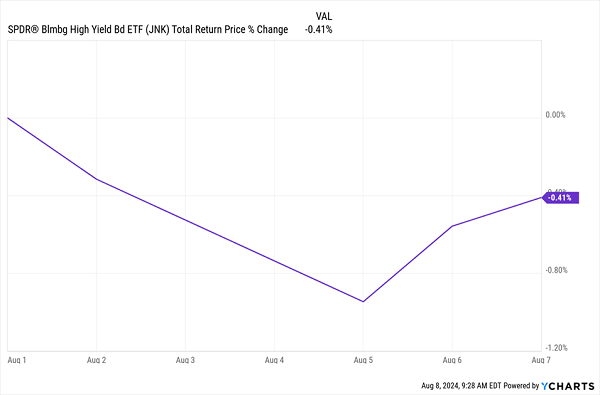

However, that isn’t working out yet: SPXX declined as much as the broader indices and hasn’t bounced back as much. But we do find another surprising alternative: high-yield corporate, or “junk,” bonds, which have barely budged since the start of August:

Bonds Hold Their Own

Many people avoid junk bonds because they don’t understand them. Yet they’re doing well now because of their high yields, as well as ongoing low corporate bankruptcies. Moreover, the Federal Reserve is set to cut interest rates, increasing the value of already-issued bonds held by junk-bond CEFs and ETFs.

We’re also seeing highly premium priced funds like the PIMCO Corporate & Income Opportunity Funds (PTY) hold their value, since the fund’s 10% dividend yield looks secure and is far higher than the 1.4% yield we’d be lucky to get from an equity index fund.

And the failure of junk bonds to decline tells us something else: this panic is limited to the stock market, and we probably won’t see more of a drop unless we see poor economic data from America. That’s the main fear in stocks now, but not bonds.

5 Urgent Buys to Cash in On the “Yen Panic” (With 8.7% Yields)

My top 5 CEFs to buy now yield an outsized 8.7%, give us exposure to stocks and high-yield bonds and are still cheap following last Monday’s dive.

In fact, the discounts on these high-income plays are so big I’m calling for 20%+ price gains from them in the next 12 months. That’s in addition to their rich 8.7%+ payouts.

A big part of that 20% gain forecast comes from the fact that they’re all smaller CEFs, which helps boost their upside as they’re discovered by the mainstream crowd.

Click here and I’ll share more details on each of them with you and explain more about why CEFs are (for now) so far off the radar. You’ll also get to download a FREE Special Report naming all 5 of these funds, including their tickers, current yields, discounts and everything else you need to get in on them now, while they’re still cheap.