I hear from readers of my Hidden Yields dividend-growth service all the time—and many are wondering why their “dividend guy” has suddenly become a “cash guy”!

Truth is, there’s been nothing for us to buy! We’ve unloaded 17 positions since last October in Hidden Yields and are sitting on a big cash pile—waiting for our chance.

And that chance is coming. In fact, if you’re using dollar-cost averaging—or investing a fixed amount of money on a fixed date, in other words—to build your portfolio, now is a great time to put money toward the safest stocks you own—especially as we get closer to “stock season”: the period from November to May, when markets are typically stronger.

Yearning for a Return to “Normal” Investing Questions

That’s our short-term play here. But what about the long run?

The good news is that bear markets are always shorter than bulls, so time is on our side. The typical bear market lasts 10 months, and we’re now into month eight, meaning November—the start of the aforementioned stock season—is when we’ll likely go shopping.

Then, with any luck, we’ll be back to judging companies on the fundamentals—not the latest utterances of Jay Powell!

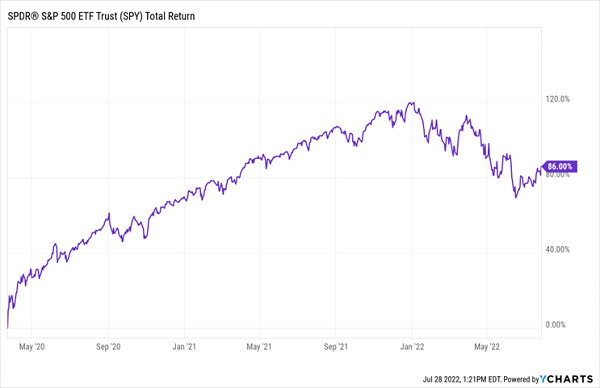

In hopes of that, I want to get back to a more “normal” portfolio-management question today: how do you know when to sell a dividend grower and take profits? Because despite this dumpster fire of a year, many folks are sitting on healthy gains, even if you bought as recently as March 2020:

2022 Mess Masks Big Profits for Many Investors

With that in mind, you just might be wondering whether it might be time to unload some of these positions and lock in your profits.

So today I’m going to give you three indicators I always use when making buy/sell decisions for my Hidden Yields. Taken together, they give us a simple strategy that lets a too-often-ignored factor—dividend growth—dictate our next moves.

Buy (and Hang on!) When Dividends Outrun Share Prices

If you’re a regular reader of my columns on Contrarian Outlook, what I’m about to say won’t surprise you: dividend growth is the No. 1 driver of share prices.

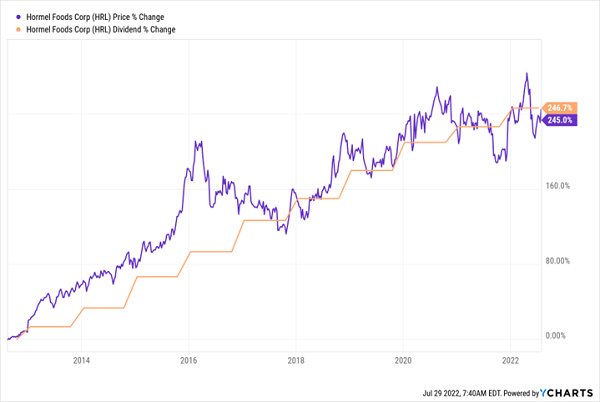

The share price of a stock Hidden Yields members know well—Hormel Foods (HRL) shows the relationship between dividends and share prices as clear as can be:

Hard to Argue These Two Lines Aren’t Related

Here’s the real trick here, though: despite this pattern, every now and then a stock’s share price lags its payout growth. And if you buy then, you’ll give yourself a chance to ride along for some nice “snap-back” upside.

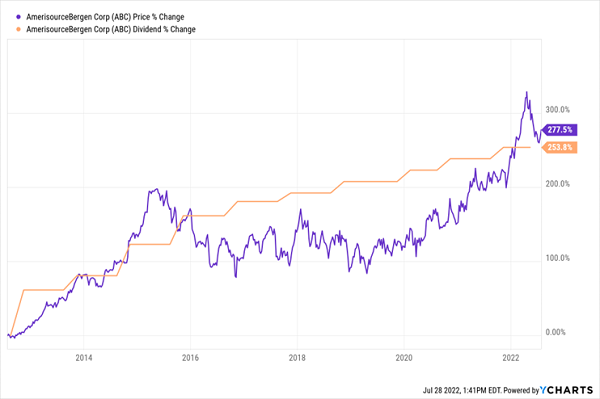

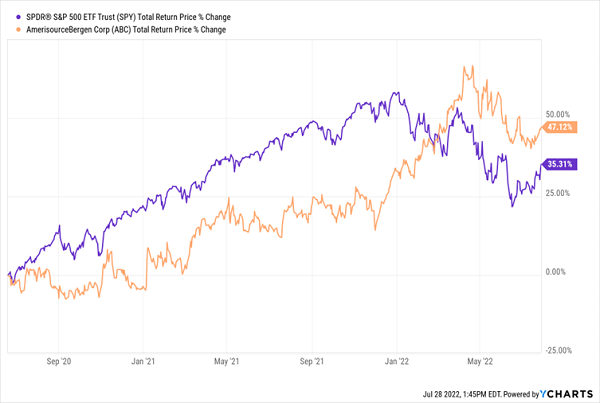

This is a cool strategy I’ve seen work time and time again. Drug distributor Amerisource Bergen (ABC), which we discussed in our article last week, provides a perfect illustration. ABC has hiked its payout 254% in the last decade, pacing its share price to an almost identical gain.

ABC’s Dividend Growth Lifts Its Share Price

See that big gap above, where the share price lags the payout over a period of a few years? I watched that closely, and when it got ridiculously wide (in part due to overblown litigation against the company), we pounced. I issued a buy call on ABC in Hidden Yields on June 19, 2020. As you can see, that was when the gap was near its widest point.

Right on cue, ABC began to close its “dividend gap,” delivering us a market-crushing 47% total return in a little over two years:

… And Then Bounce Back

I’m sure you see where I’m going here—and how this strategy can be turned on its head to tell us when it’s time to sell.

Sell When Share Prices Outrun Payout Growth

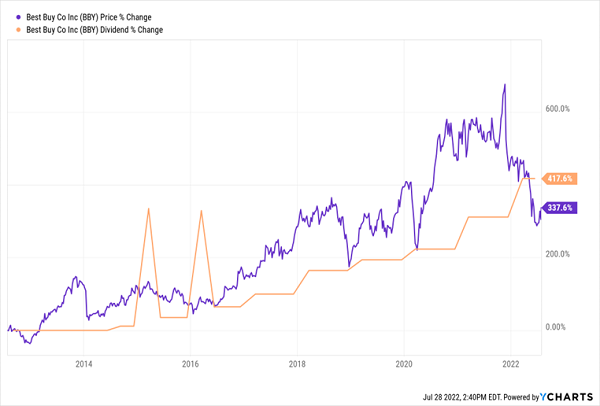

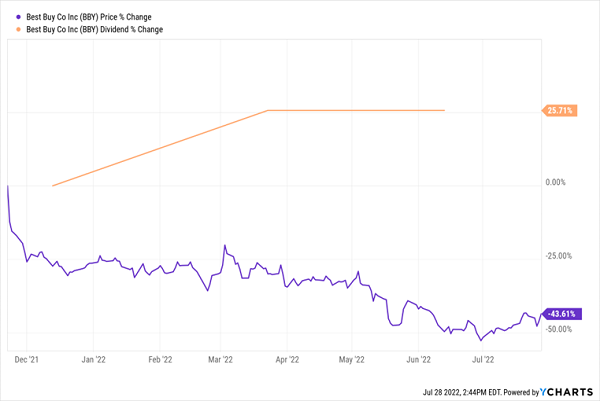

Just as a share price that’s behind its payout growth can be a buying opportunity, a stock that’s too far ahead can alert us to a big tumble. To see what I mean, consider Best Buy (BBY)—and let’s keep anyone who bought the stock in late November in our thoughts for a moment:

BBY Flies Too Close to the Sun

We’ve avoided Best Buy in Hidden Yields because no matter how fast the company boosts its payout—and it has sent its dividend soaring in the last decade—investors bid the share price higher, putting the ingredients for a big fall in place.

That’s exactly what happened when the situation got truly ludicrous in late 2021. Anyone who bought then suffered a sickening 44% loss, even as the payout jumped:

Big Dividend Hike Is Cold Comfort for November BBY Buyers

Which brings us to another factor we need to keep in mind at all times when buying (and especially selling) dividend growers.

Payout Ratios Are Your Window on Dividend (and Share Price) Health

The key signal of whether a dividend can keep growing—and pulling up the share price—is a company’s payout ratio, which is the percentage of the last 12 months of free cash flow (FCF) that have gone to dividends.

(We prefer FCF to net income here because the latter is an accounting figure that can be manipulated, while FCF is the amount of operating cash flow left after capital expenses—a simple number that can’t be fudged.)

I demand a ratio of 50% or less for stocks I recommend in Hidden Yields (though real estate investment trusts can have higher ratios, as these companies pull in predictable rents from tenants).

If you own a “regular” stock whose payout ratio spikes above that line, especially well above, it’s time to sell. And you need to sell yesterday if your FCF payout ratio goes negative (meaning the company is paying dividends while generating negative cash flow).

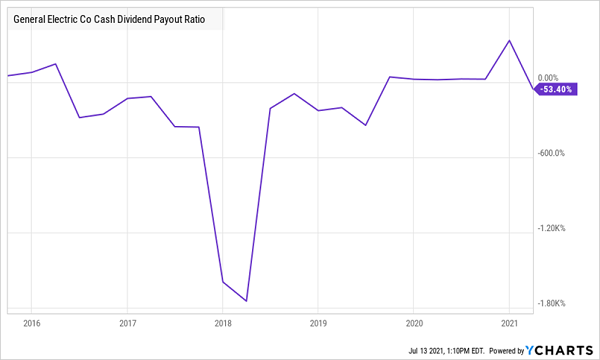

The classic example is General Electric (GE), a dividend go-to that saw its payout ratio go negative with the June 2016 payout.

That was the first sign a payout cut was coming, but it was largely ignored—until GE slashed the dividend in half a little over a year later, in December 2017. The move triggered a big share-price drop from which the stock has yet to recover. (The payout has since been sliced again and now stands at just eight cents a share.)

GE’s “Dividend Red Alert” Went Unheeded

Today, GE’s FCF payout ratio is a much healthier 17%, but its dividend cuts and share-price drops leave it with a pathetic 0.44% yield, which isn’t enough to get our pulses racing. And with revenue down by more than half in the last 10 years—and showing little sign of growth—there’s little hope for more payout hikes from here.

URGENT: Buy These 7 Dividend Growers Before the Fed-Driven Recession

Look, you and I both know, deep down, that the Fed will probably tip us into a recession with its outsized rate hikes. After all, Powell and Co. have been late on every single shift in the economy since 2020!

I want you to be ready—which is why I’ve assembled my 7-stock “Recession-Resistant Portfolio,” and I’m inviting you to take “kick the tires” on this collection of reliable dividend growers now.

All 7 of these firms are growing their payouts fast. And all 7 are seeing their stocks rise as those dividends continue to head north.

How will that play out for us? If the market shoots higher, I expect these 7 “recession-resistant” plays to do even better. If stocks stumble, these 7 companies’ growing dividends will help stabilize their share prices. And we’ll collect their surging dividends the whole time!

This is why, no matter what happens, I’m calling for 15% annualized gains from these 7 stout companies over the long haul.

The time to buy them is now. Click here and I’ll share my full dividend-growth strategy and give you the opportunity to download a Special Investor Report revealing the names, tickers and my latest research on all 7 of these “recession-resistant” dividend growers.

Don’t miss your chance to buy these 7 “ironclad” dividends now, while they’re still bargains!