These five stocks may deliver big dividend raises. I’m talking potential payout hikes starting at 20%.

It’s possible that one of these firms doubles their dividend because, heck, they did that one year ago!

How do I know?

Gaudy dividend growth numbers are especially attractive because they often lead to big price gains. I call this dynamic the “dividend magnet.”

The “magnet” effect is pretty straightforward: When a company not only grows its profits, but shares gobs of those earnings with stockholders as dividends, investors on the outside see both a sign of quality and the potential for income and buy in—driving the stock price higher for us!

Chip stock Broadcom (AVGO) is a perfect example of this dividend magnet in action. Since its 2016 merger with Avago, Broadcom’s yield has spent most of its time below 4%, sometimes as low as 1%.

Investors seeking high current yield alone would never have given AVGO a second look.

But investors who saw the company’s dividend-growth potential dialed in bigtime profits:

Why Does AVGO Always Have a Small Yield? Shares Climb Too Fast!

Investors who bought AVGO shares shortly after Broadcom and Avago merged, then held on through today, are currently collecting a wild 18% yield.

If the headline dividend puts investors to sleep, consider the velocity of the payout. It’s possible a big raise—and subsequent price pop—is on the way.

In the spirit of the dividend magnet, let’s discuss five companies that are due to deliver dividend hikes in the upcoming weeks. Recently these shareholder-friendly firms have gifted investors with generous raises between 20% and 178%. If history is ready to repeat, or at least rhyme, then let’s be ready.

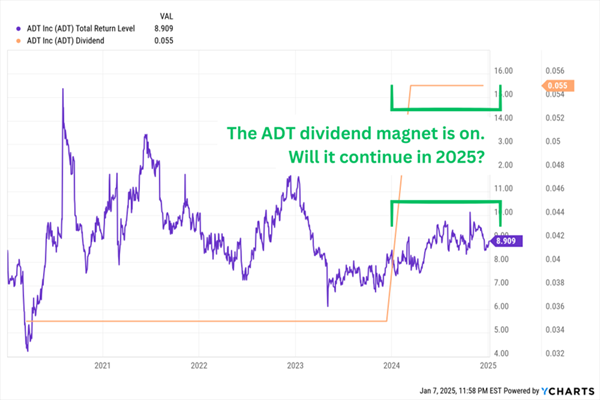

ADT Inc. (ADT)

Dividend Yield: 3.1%

2024 Increase: 57%

Projected Q1 Dividend Announcement: Late January to February

I love big hikes after years of stagnant payouts. A sudden dividend boost can reflect a sea change, whether that’s through organic growth or a sudden business add-on.

Hence my interest in seeing that ADT Inc. (ADT), a provider of home and small-business security technology, announced in January 2024 that it would juice its payout by 57%—its first hike since initiating a dividend a couple months after its January 2018 IPO.

ADT is in a curious situation. When Apollo spun the company off, ADT was saddled with nearly $10 billion in debt. The only meaningful cut it has made to that debt came in 2023, after ADT sold its commercial business to private equity for $1.6 billion. ADT’s debt now stands at $7.7 billion, which is still more than its $6.2 billion market cap.

Interestingly, ADT’s resulting dividend action wasn’t a special dividend—a common move after a big sale—but a significant raise to its regular distribution.

What ADT does next will be telling. Its payout ratio is an uber-safe 30%. And after operating in the red for most of its publicly traded life, ADT has strung together two years of positive earnings, and it’s expected to finish 2024 with a 43% pop in adjusted profits after shutting down its lagging solar division. But the company still has a pile of IOUs to whittle away, which could limit its dividend aggression.

The first period to watch is late January—that’s when ADT announced its big hike last year. But historically, ADT announces dividends in late February or early March, alongside its Q4 and full-year earnings report.

ADT Has Sounded the Dividend Growth Alarm

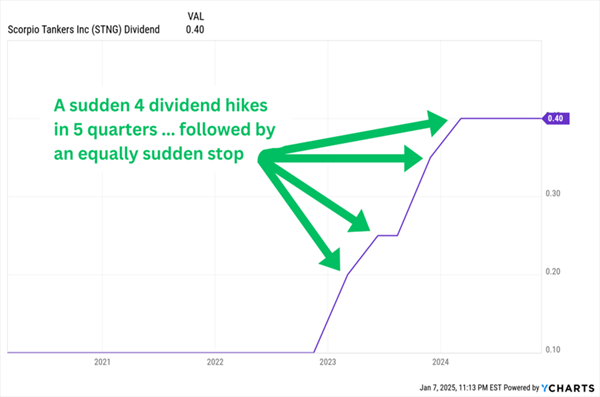

Scorpio Tankers (STNG)

Dividend Yield: 3.0%

2024 Increase(s): 100%

Projected Q1 Dividend Announcement: Mid-February

Scorpio Tankers (STNG) is a seaborne transportation company specializing in the shipping of crude oil and refined petroleum products. It currently boasts 102 vessels, including 14 Handymax vessels (35,000 and 48,000 deadweight tons), 49 Medium Range vessels (40,000 to 55,000 DWT) and 39 Long Range 2 vessels (105,000 to 115,000 DWT).

Tanker and shipping stocks are among the most cyclical stocks we’ll ever come across, with operational results and stock prices as fickle as the sea. To wit, STNG has recorded net losses in five of the past 10 years—and it has still made about $900 million in profits during that time.

That’s why most shipping stocks have extremely variable dividend programs. Which makes STNG’s more traditional regular dividend stand out.

And that dividend has exploded, from 10 cents per share in February 2022, to 20 cents in February 2023, to 40 cents in February 2024. That’s two consecutive dividend doublers!

But the reason I’m so interested in Scorpio’s February 2025 dividend announcement is a matter of timing. Scorpio started aggressively raising across 2023, first with the doubler to 20 cents, but then to 25 cents (May) and 35 cents (November). Scorpio’s February 2024 hike was “just” 14% from the prior quarter, and STNG has stayed put since then.

The Start of a Longer Dividend-Growth Trend, Or Just a Short-Lived Spurt?

In other words, the upcoming announcement could tell us whether Scorpio’s recent raises are more than a short-term flash in the pan. It certainly has room, at a payout ratio of less than 15% of 2024’s expected full-year earnings.

Just be aware: Shareholders have been burned by Scorpio’s more rigid dividend program; the tanker firm slashed its dividend by 92% in 2017 in the midst of a multiyear downturn. Accounting for a 1-for-10 reverse split in 2019, the current distribution is only a third of what it was previously.

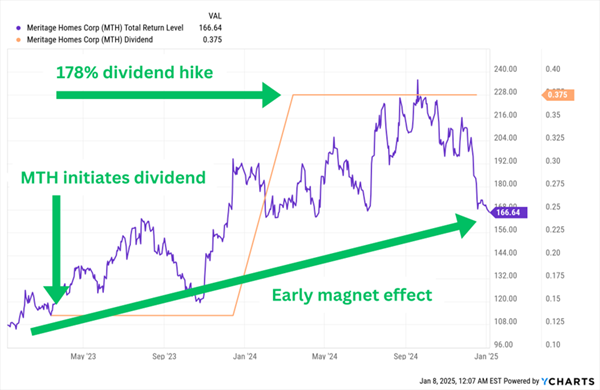

Meritage Homes (MTH)

Dividend Yield: 2.0%

2024 Increase(s): 178%

Projected Q1 Dividend Announcement: Mid-February

Meritage Homes (MTH) is a mid-cap homebuilder that builds single-family attached and detached homes for first-time and first move-up buyers, primarily across the southern U.S., from California to the Carolinas. And like many homebuilders, it also provides mortgage, title, title insurance, and other housing-finance products to buyers of its homes.

Regular readers will remember MTH in my 2024 roundup of new dividend programs. Meritage Homes came out of the gate swinging in early 2023, following both a big jump in profits for full-year 2022 and increased confidence that the Fed’s rate hikes would soon be coming to an end. (BofA says that for every 25 bps that the mortgage rate declines, as long as it’s under 7%, more than a million households are priced back into the housing market.)

MTH’s profits declined in 2023, but it was still a strong year for the highly cyclical homebuilder, and in early 2024, it nearly tripled its dividend with a 178% boost to 75 cents per share quarterly. Of course, that distribution is now 37.5 cents per share by virtue of a 2-for-1 stock split at the start of 2025, which Meritage needed after a multiyear stock surge.

Impressive Early Dividend Days for Meritage

That puts a massive target on Meritage’s next expected dividend announcement, which should come in mid-February. On the one hand, the pros see another respectable year from MTH, with profits climbing by mid-single digits, and MTH pays out less than 15% of profits as it is.

On the other hand, a conservative hike (or no raise at all!) could signal anxiety over 2025’s outlook. Despite multiple Fed rate cuts, 30-year mortgage rates have climbed back to nearly 7%, rekindling worries about home affordability. As a result, MTH’s value has plunged by 30% since peaking in September 2024.

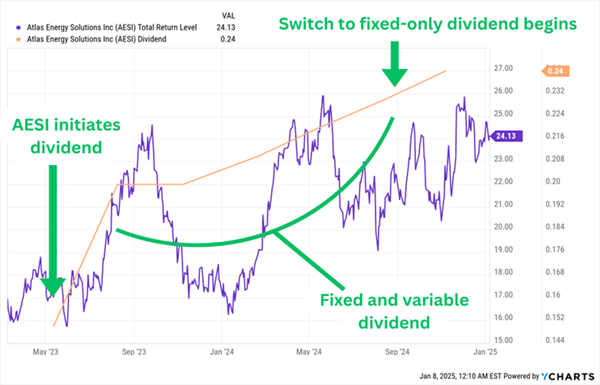

Atlas Energy Solutions (AESI)

Dividend Yield: 4.3%

2024 Increase: 20% (across 4 hikes)

Projected Q1 Dividend Announcement: Early February

Atlas Energy Solutions (AESI) is an energy equipment and services company that provides transportation and logistics, storage solutions, and contract labor services to oil and natural gas E&P firms, as well as oilfield services companies, in the Permian Basin of Texas and New Mexico. Most notably, it provides mesh frac sand—a “proppant” that props open the fractures created in the hydraulic fracturing process.

Atlas Energy is another recent public listing that had its IPO in March 2023, then announced its first dividend (as a publicly traded company, but its sixth overall) just a couple months later.

A quick look at just its payouts would indicate a generally rising regular dividend, but the reality is something much different.

- Q1 2023: 15 cents (15 cents fixed, no variable)

- Q2 2023: 20 cents (15 cents fixed, 5 cents variable)

- Q3 2023: 20 cents (15 cents fixed, 5 cents variable)

- Q4 2023: 21 cents (16 cents fixed, 5 cents variable)

- Q1 2024: 22 cents (16 cents fixed, 6 cents variable)

- Q2 2024: 23 cents (Atlas changes program from fixed-and-variable to entirely fixed dividend)

- Q3 2024: 24 cents (and announced a $200 million share buyback authorization)

AESI: A Complicated But Promising Young Dividend

What we’re looking for in early February is any further indication that AESI has plans to be a rare quarterly dividend raiser.

It’s a tough test—the company’s expected to finish 2024 with a 33% drop in profits to $1.03 per share, which would put its dividend coverage around 93%. But profits are estimated to nearly double in the year after, putting its coverage at a much more comfortable 50%—if Atlas management is confident about continued growth, it could signal that with yet another quarterly hike within its fully fixed dividend program.

Penske Automotive Group (PAG)

Dividend Yield: 3.1%

2024 Increase: 51%

Projected Q1 Dividend Announcement: Mid-January

Penske Automotive Group (PAG) is an international automobile retailer that operates dealerships not just in the U.S., but also the U.K., Germany, Italy, Canada, and Japan. These dealerships cover just about every international brand under the sun.

Source: Penske Automotive Group Q3 2024 Earnings Presentation

It also boasts a thriving commercial-truck retail business across North America, and it distributes and retails commercial vehicles, power systems, engines, and more across Australia and New Zealand. In addition to all that, it owns roughly 29% of Penske Transportation Solutions, a North American transportation services, logistics, and supply-chain management services provider.

Penske has an almost uninterrupted run of quarterly dividend hikes going back more than a decade—PAG did suspend its payout for two quarters in 2020, but resumed payouts that same year at the same level, then just went right back to raising and raising and raising.

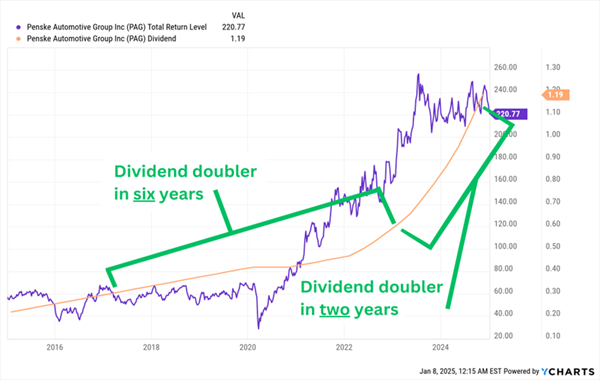

Penske’s dividend finished 2024 at $1.19 per share. That’s nearly double the 63 cents it started at in 2023! In fact, PAG actually accelerated as the year went on—its Q4 dividend hike was the largest year-over-year improvement of 2024. And that’s despite a largely down year that should see profits finish about 16% lower before bouncing back a little in 2025.

PAG Just Shattered Its Previous Dividend Doubler Lap Speed

For now, Penske’s quarterly dividend announcements are must-watch events for dividend growth investors. The next one should come in mid-January.

My 2025 Dividend Plan: Buy the Best Yields of 2035!

I’m going to be laser-focused on stocks like these all year long.

That’s because my 2025 investment plan is to buy “Dividend Magnets”—stocks that boast some of Wall Street’s fastest-growing payouts, which in turn attract more investors and “pull” prices higher, providing us with the potential for a wicked 1-2 punch of total returns.

Some of these stocks are in Wall Street’s far-flung corners, and a few of them are hiding in plain sight. In fact, one of my favorite Dividend Magnets is a blue-chip Dow component!

I’m currently zeroed in on 5 stocks I see as the next Dividend Magnet winners. They’re my top picks for the fastest-growing payouts—and share prices—through 2025 and beyond.

And I want to share them with you right now. Simply click here for more about these 5 “Dividend Magnet” winners, plus access to a free Special Report revealing their names and tickers.