The yield curve is now “inverted.” This warning has preceded “seven of four” recent bear markets (more on this in a moment). Time to be safe and sell everything?

Before we stash cash in the mattress, let’s review the actual facts. Fundamental Capital’s Troy Bombardia, one of my favorite historical finance quants, has run the numbers on what happens to the S&P 500 when the 10-year “long” yield dives below the three-month rate:

- In 1966, 1973, 2000 and 2006, an inverted yield curve indeed preceded a big stock market pullback (usually by a year or two).

- Meanwhile in 1978, 1980 and 1989 it didn’t mean much. Investors who sold on this indicator likely regretted it.

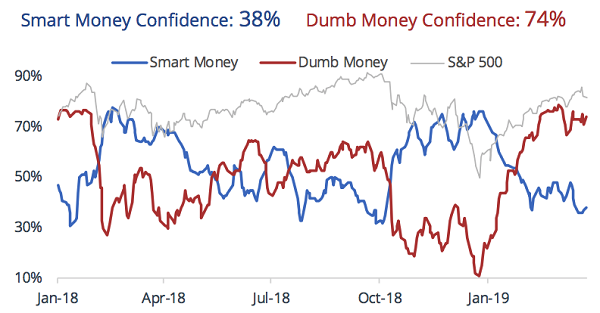

I’ve actually grown wary of the stock market’s short-term outlook in recent weeks, but not because of any particular yields. The “dumb money” hasn’t been this confident of further market gains since January 2018. Dumb was dumber, because the stock market proceeded to crash swiftly and quickly:

Source: Sundial Capital

(Most individual investors would be categorized as “dumb money” because they get greedy when markets are hot and tend to buy high. Professionals, on the other hand, are more likely to stay calm at tops and smartly buy the dips.)

To me, this positive sentiment among classic “contrarian” indicators is scarier than any difference in bond yields. Now I’m not saying cash is the solution. Most perma-bears are broke because they aren’t in the market often enough. (Even those that know when to sell usually don’t know when to get back in.)

A cash position is, quite honestly, dead weight. As I write our Contrarian Income Report portfolio yields a generous 7.4%. Every million dollars in cash that sits on the sidelines misses out on $6,166.67 in monthly income. That adds up quickly!

Fear, even when justified, can be quite costly. A better idea with markets (again) a bit frothy is to invest in pullback-proof dividends.

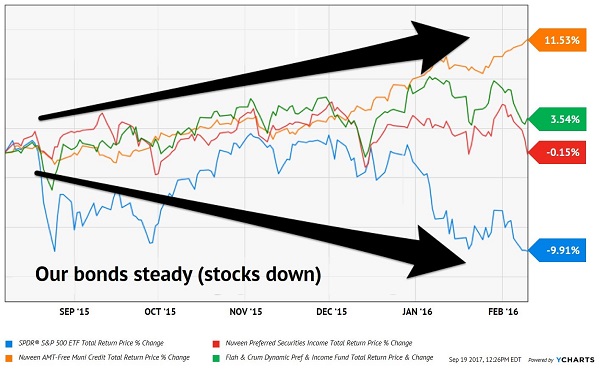

For example, we fittingly launched the Contrarian Income Report months before the market’s tantrum in 2016. The S&P 500 promptly dropped 10% as a welcome present!

It was no problem for our strong dividends, however. In fact, subscribers who focused on their own holdings rather than the financial news likely have missed the broader carnage altogether. Our core bond fund holdings (orange, red and green lines below) not only continued to pay their 7% dividends, but they also averaged a 5% price gain while stocks were swooning:

What Pullback? Contrarian Bond Funds Sail

My bet is that carefully curated bond funds will repeat their resilience during the market’s next pullback. And honestly, it shouldn’t matter to you with a true “no withdrawal” portfolio that lets you focus entirely on dividends and ignore price action altogether. Here’s why.

We Avoid Reverse Dollar Cost Averaging

Most investors practice “buy and hope” investing. They pick up shares and root for them to appreciate in price. And that’s it.

These first-level types have no plan on how to generate cash flow from their holdings. They think they’ll sell someday, and hope it’s at a higher price. But they don’t have a set game plan to sell and methodically collect regular, sustainable cash payments from their portfolios.

Many financial advisors step into this void, pitching a “4% withdrawal rate.” These guys (who have not retired successfully themselves, by the way) say that you can safely withdraw 4% or so every year from your portfolio and use this as spending money.

Generally, they’re right. But when they’re wrong, it’s disastrous.

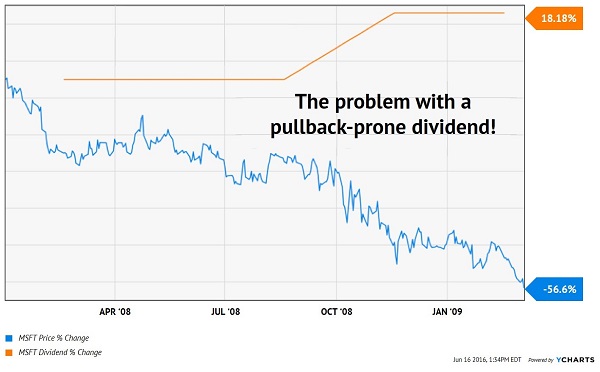

The fatal flaw with the 4% annual withdrawal strategy for retirement is that every few years, you’re faced with a chart like this:

Selling Here is Reverse Dollar Cost Averaging

Investors who practiced the 4% withdrawal “strategy” with Microsoft shares in 2008 were forced to take out money at exactly the wrong time. If they didn’t have enough dividend income to support themselves at the time, they had to sell even more shares for additional income.

Sadly, this is reverse dollar cost averaging–selling even more shares when prices are low, which reduces upside when markets normalize. This is the same phenomenon that built your wealth, except now it works against you!

The solution is to transition away from ever having to sell a share. And pullback-proof dividends of 6%, 7% or 8% are a great solution. They give you a means to collect regular, secure cash from your nest egg on a monthly and quarterly basis, without being forced to sell low (or sell ever).

In fact, you can do even better – you can step in and add money (and reinvest dividends) when prices are low and yields are high.

Because Upside Matters, Too

You’ve probably been told you should dump—or at least reduce—your stock holdings and focus on fixed-income investments as you near and enter retirement. It sounds like a smart move, but going lean on stocks leaves you open to three big risks:

- Outliving your savings,

- Missing out on the long-term gains only the stock market can offer. And, of course,

- Inflation.

So why not blend a portfolio of 7%+ bond funds with smart stock picks that provide you with similarly high yields with upside to boot? Sure, they may “sell off” a bit if the markets pull back. But who cares. Like a savvy rich investor, you’ll be able to step in and buy more shares when they are cheap – without having to worry about your next capital withdrawal.

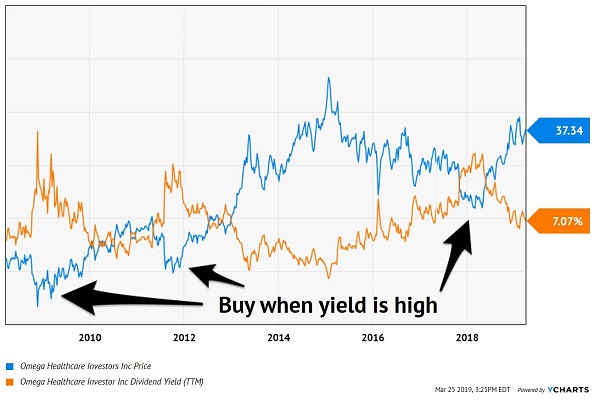

Let’s take healthcare landlord Omega Healthcare Industries (OHI). The firm’s payout is usually generous, and always reliable—yet, for whatever reason, its sometimes-manic price action gives investors heartburn.

But it shouldn’t. It’s actually quite predictable. Check out the chart below, and you’ll notice:

- When the stock’s yield is high (orange line), its price is low. Investors should buy here.

- When the stock’s price is high (blue line), its yield is low. Investors should hold here, and enjoy their dividend payments.

Investing is Easy: Buy When Yield (Orange Line) is High

Today OHI’s yield is neither opportunistically high nor offensively low. It’s a respectable “hold” in a high yield portfolio. If yield curve or tariff or recession fears drive the price lower, I would recommend buying more shares at their higher yield without hesitation.

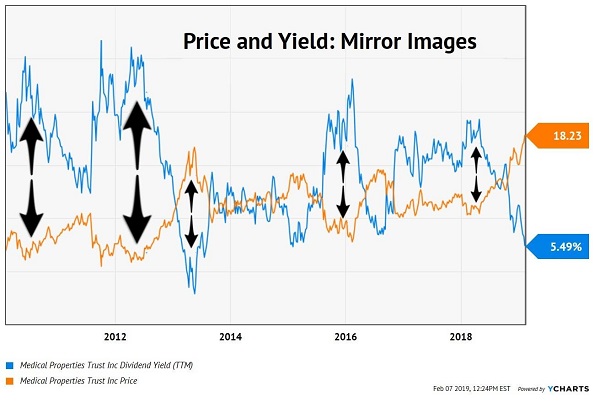

On the other hand, the recent “market froth” prompted me to sell one of our favorites. Fellow landlord Medical Properties Trust (MPW) is about as recession-proof and pullback-proof as it gets. The firm provides financing to hospitals and pays most of its profits to investors.

As with OHI, MPW’s stock price and yield are usually mirror images of each other:

With its yield near its all-time lows, it made sense to sell (and book our 109% total returns). Even the sleepy high yield space can experience mild bouts of irrational exuberance! Fortunately there are investments with more price upside that will actually give us a raise to boot (from 5.5% to 7.4% dividends).

Introducing the “Pullback-Proof” Income Portfolio Paying 7.5%

The “cash or bear market” no-win quandary inspired me to put together my 5-stock “Pullback-Proof” portfolio, which I’m going to GIVE you today.

These 5 income wonders deliver 2 things “blue-chip pretenders” like General Mills and Target never could, such as:

- Rock-solid (and growing) 7.5% average cash dividends (more than my portfolio’s average).

- A share price that doesn’t crumble beneath your feet while you’re collecting these massive payouts. In fact, you can bank on 7% to 15% yearly price upside from these five “steady Eddie” picks.

With the Dow regularly lurching a stomach-churning 1,000 points (or more) in a single day during pullbacks, I’m sure safe—and growing—7.5% every single year would have a lot of appeal.

And remember, 7.5% is just the average! One of these titans pays a SAFE 8.5%.

Think about that for a second: buy this incredible stock now and every single year, nearly 9% of your original buy boomerangs straight back to you in CASH.

If that’s not the very definition of safety, I don’t know what is.

These five stout stocks have sailed through meltdown after meltdown with their share prices intact, doling out huge cash dividends the entire time. Owners of these amazing “pullback-proof” plays might have wondered what all the fuss was about!

These five “pullback-proof” wonders give you the best of both worlds: a 7.5% CASH dividend that jumps year in and year out (forever), with your feet firmly planted on a share price that holds steady in a market inferno and floats higher when stocks go Zen.