There aren’t many things we can say for certain these days, but there is one: We dividend investors are far better off than the mainstream crowd!

Consider the poor souls holding “America’s ticker”—my name for the SPDR S&P 500 ETF Trust (SPY). I call it that because, well, pretty well everyone owns it. These folks white-knuckled it through the April “tariff tantrum” and are now on a knife edge as the ETF bobs around near all-time highs, boosting the odds of yet another sharp drop.

Of course, pullbacks are a constant in investing (and something we contrarians love to tap for bargains!). But the trouble with holding something like SPY, with just a 1.2% payout, is that, if you need cash from your holdings, you run the very real risk of being forced to sell at a loss in a downturn.

That risk gets higher if you’ve spread your holdings across just a few stocks, or lean too heavily on one sector, like tech. (SPY “bakes in” this fault, by the way: A third of its portfolio is tied up in tech, far and away its biggest allocation.)

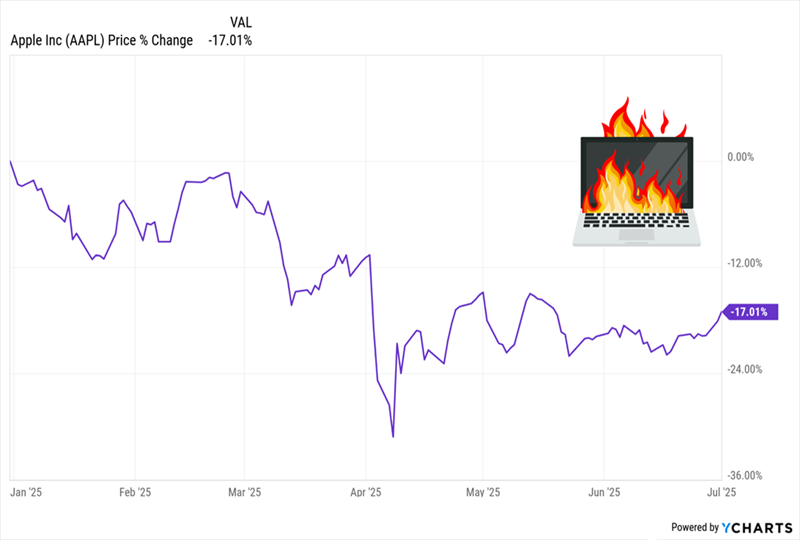

Consider a stock like Apple (AAPL), whose dividend is fine, but whose share price has cratered. Tim Cook’s company shed 17% over the first half of 2025.

Sell Into This Dumpster Fire? A Nightmare for Any Retiree

Having to sell into a drop like that to get the cash we need can be a retirement killer.

Our Dividend Picks Are Built for Trying Times

Situations like that spotlight the value of high, safe payouts that help keep our bills paid no matter what. They also let us reinvest, boosting our income and upside as we do.

Even better if we use a dividend reinvestment plan (DRIP), which automatically reinvests our payouts at a fixed level and a regular frequency. That way, we’ll automatically buy more shares when they’re down and fewer when they’re pricey.

This is how lasting wealth is created. And it’s yet another reason why dividends are crucial. But there is one thing that is, frankly, a pain when it comes to dividends: They can be a nuisance to track.

To be fair, more brokerages do offer accounts with built-in dividend trackers. But they’re only useful for any investments you hold with that particular broker.

What if you have more than one account, or invest through more than one brokerage? Or you want to project income from an investment you don’t own (yet) but are considering?

For those situations, brokerage-run apps are clumsy at best. Useless at worst.

There are a bundle of “outside” apps out there, too. But switching to one likely means manually entering your tickers and/or learning a whole new system. No thanks!

Know What You’re Getting Paid—and When—With Income Calendar

Here at Contrarian Outlook, we’ve tried a lot of dividend-projection tools, and we didn’t find any we loved (or even liked much). So we created our own. It’s called Income Calendar, and it quickly and easily ensures your dividends are in your account before your bills come out.

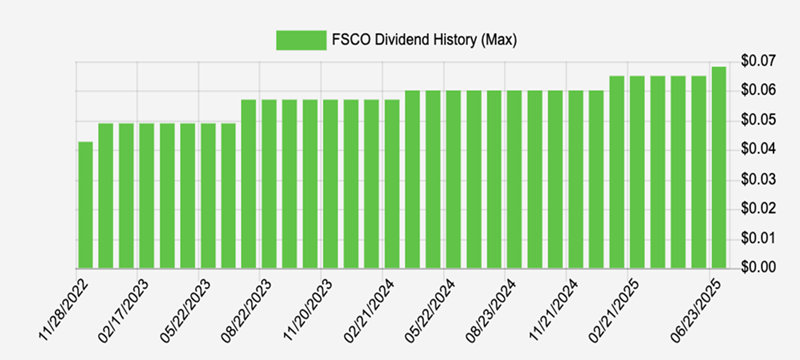

Let’s walk through this handy tool with a ticker subscribers to my Contrarian Income Report service will recognize: FS Credit Opportunities (FSCO). This closed-end fund (CEF) has returned a tidy 19% for us since we bought it last October, as of this writing.

FSCO is really a business development company (BDC) in a CEF wrapper: it offers loans in the private market, where it can dictate favorable terms. This, in turn, steadies its net asset value (NAV, or the value of its underlying portfolio). That gave its holdings a far calmer ride than our poor SPY investors endured in the first half of ’25!

Steady Lender Sails Through the 2025 Tariff Storm

The fund takes the returns from this rock-steady portfolio and hands them to us in the form of its outsized 11.2% dividend. Payouts come our way monthly and steadily edge higher over time, in tune with FSCO’s NAV. Take a look at this chart, generated through, you guessed it, Income Calendar:

A Rare 11% Dividend That Grows

Source: Income Calendar

Note that we only have a few years’ worth of dividends to look at here. That’s because FSCO only launched in November 2022. That newness is a big part of our opportunity here.

Since CEF investors hate new issues, we get to buy at a slight discount to FSCO’s NAV, around 2% as I write this. I see a big premium in the future as more income-seekers catch on to FSCO’s growing double-digit payout.

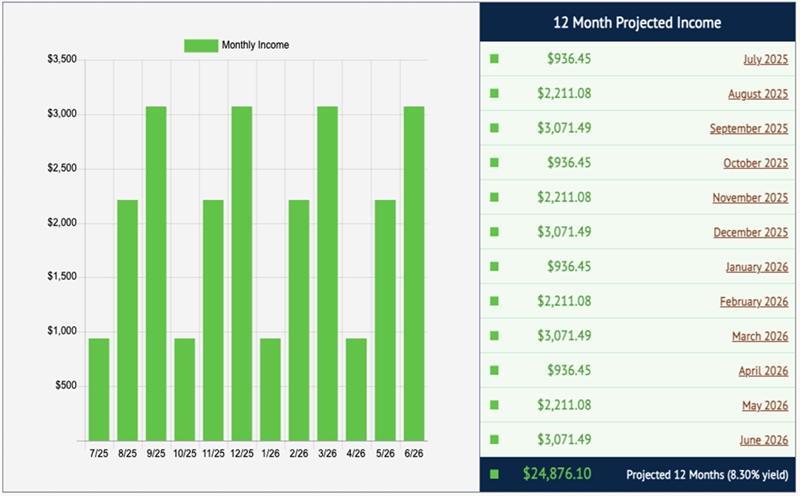

Now let’s swing over to Income Calendar and plug in FSCO, along with a couple other Contrarian Income Report holdings that pay quarterly, so we can get a good sense of how our tracker helps us navigate a range of payout frequencies.

Those would be gas-pipeline operator Antero Midstream (AM), which stands to gain as the Trump administration’s new tax-and-spending law helps the gas producers using its pipelines—and Ares Capital (ARCC), a lender to small businesses that’s set to write more loans as these firms adopt AI, boost their productivity and expand.

Let’s say we invest $100,000 in each. Income Calendar tells us, immediately, what we can expect in terms of dividends every month from our 3-buy “mini-portfolio”:

As you can see, with just these three buys, we’ve got dividends ranging from $936.45 in a month up to $3,071.49, and a total of $24,876.10 in the year, on just $300K invested. That’s a rich 8.3% yield. (Bear in mind, too, that to be overly conservative, we don’t project dividend growth here, so our “real” payouts could end up higher.)

You can get complete breakdowns by stock, plus a month-by-month calendar giving you a heads-up on earnings dates, ex-dividend dates and other critical periods for every one of your holdings. Instantly!

Check it out. Here’s what our three-buy portfolio shows us for September 2025, one of our highest-paying months:

We can see our projected pay dates, as well as ex-dividend dates (the dates before which we need to be “in” the stock to get the next payout) and even things like market holidays. We even get a heads-up on when our stocks are due to report earnings—though there are none of these for our trio in September.

There’s more, too, like real-time email alerts every time a dividend drops into our account, a “week-ahead” summary telling us exactly how much we’ll get paid and when, a handy tool that instantly tells us our “yield on cost” (so we can see the “true” yield on each of our stocks, based on the timing of our original buy) and more.

Now—with dividends (and the need to stay on top of them) more important than ever—is a perfect time to try Income Calendar.

Click here and I’ll tell you more about this powerful dividend planner and give you the opportunity to “road test” it out for yourself. I’m sure you’ll love it.