If you’re a serious dividend investor, you should never trust a stock screener.

They might be OK for blue-chip stocks like Pfizer (PFE) and Procter & Gamble (PG). But these stocks don’t pay enough to properly fund a retirement portfolio powered by dividends anyway.

The big problem with screeners is that they get tripped up when yields get serious. They handle the 2% and 3% payers alright. They’ll spit back a fairly accurate dividend payout ratio based on earnings, and give you price-to-earnings metrics that are fair enough.

But high-yield structures like REITs and BDCs? Forget it. They break the machines.

The cash cows we buy to secure yields of 6%, 7% and 8% or more are unique. Traditional “earnings” don’t really matter. Each vehicle has its own measure of profitability that traditional screeners can’t deal with. For example:

- Real estate investment trusts (REITs): Funds from operations (FFO) adds in factors such as depreciation and amortization to get a truer sense of the real estate business.

- Master limited partnerships (MLPs): Distributable cash flow (DCF) is the cash left over after obligations to the general partner have been paid out, and debts are paid.

- Business development companies (BDCs): Net investment income (NII) is pretax income generated from investments such as stocks, bonds and loans, minus expenses.

Stock screeners tend to get the stats on these firms dead wrong.

The solution? We must calculate these numbers ourselves. It’s a bit of work, sure, but it’s also how we bag big dividends that most investors don’t even know about.

To evaluate the dividend safety of a REIT, I add up per-share FFO on my own, then use that to calculate price-to-FFO (valuation) and FFO payout ratio (which determines how safe the dividend is).

I’ll discuss three high-paying REITs that the machines get wrong, but first, let’s do a couple real-life examples.

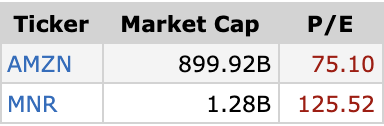

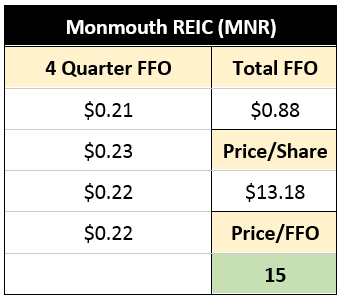

First up, let’s look at Monmouth Real Estate Investment Corporation (MNR). I recently highlighted this warehousing REIT because the screeners flagged its seemingly outrageous payout ratio.

The screeners got that wrong, of course, and they’ve flubbed MNR’s valuation, too. By a lot.

Source: FinViz

I like warehousing REITs as much as the next guy. But would you pay a massive 67% premium to Amazon.com (AMZN)—one of the most perpetually expensive stocks on Wall Street—to get in?

I wouldn’t. And I don’t have to.

A manual calculation shows that Monmouth trades at 15 times its trailing 12-month FFO. That’s not the cheapest price you’ll ever buy a REIT at, but it’s a fair (and more importantly, accurate) valuation.

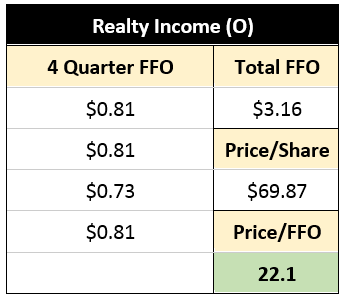

This doesn’t just happen with smaller, less covered REITs like Monmouth. Screeners give even the most popular real estate plays a bad name.

Source: FinViz

Here, “Monthly Dividend Company” Realty Income (O) appears priced to perfection, with a P/E of 52 that’s typically reserved for newly profitable technology upstarts. But again, FFO tells a different tale.

Realty Income is one of the most respected stocks in retail real estate, and it boasts one of the best dividend track records out there. It’s going to trade at a premium. But its price/FFO is at least within the confines of reality. That 52 P/E simply isn’t.

If this sounds frustrating, it is. But remember: Screener errors like this work in our favor, because they allow us to secure yields that simpler dividend minds don’t even see.

Now, let’s look at a few more P/E fakeouts that scare normal investors out of high yields of 5.0%-11.1%.

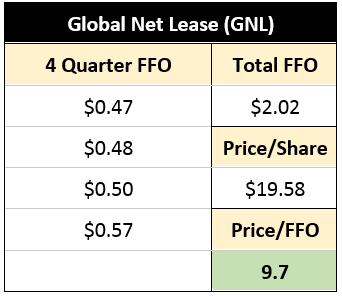

Global Net Lease (GNL)

Dividend Yield: 11.1%

TTM P/E Ratio: 391.6

Global Net Lease (GNL) is somewhat similar to Realty Income in that it’s a single-tenant, net-lease REIT. But it’s actually more diversified than Realty Income in that it operates not just in the U.S., but also the U.K., Germany, France, Belgium, the Netherlands, Luxembourg and Finland.

The portfolio isn’t as expansive, but there’s still some breadth. Global Net Lease owns 343 properties leased out to 112 companies across 45 industries, including the likes of America’s FedEx (FDX), German utility RWE and Netherlands bank ING Groep (ING).

So, what does a company like this go for?

Source: FinViz

GNL’s 11% yield is the obvious draw, and if earned the right way, that’s a dividend worth overpaying a little for. But 1.) I wouldn’t pay 390 times earnings for a rock-solid 20% yield, and 2.) GNL’s dividend hasn’t budged since it was initiated in 2015—the yield is a product of a falling share price.

On an FFO basis, it’s a different story—but still not a picture-perfect one.

Global Net Lease looks downright cheap at less than 10 times trailing adjusted FFO, but I think you should avoid this stock nonetheless, for three reasons:

- GNL’s dividend is set at 53.25 cents per quarter—that’s $2.13 per year, which is well more than the $2.02 per share it has earned in FFO over the past 12 months.

- The recent trend for its FFO is down, too. It earned $2.09 per share over the previous 12 months.

- The dividend recently switched from monthly to quarterly. That’s not a warning sign, but monthly dividends are a sweet perk that you hate to lose.

In short, everything having to do with the dividend is heading in the wrong direction. I’m not inclined to bite—even at this cheap price.

Stag Industrial (STAG)

Dividend Yield: 5.0%

TTM P/E Ratio: 46.7

Stag Industrial (STAG), I’m happy to say, is better about living within its means.

Stag Industrial, like Monmouth, operates in the industrial space, which is a massive $1 trillion market opportunity. But Stag has a very specific tenant in mind. Stag targets single tenants, which is closer to a $500 billion opportunity, though when you whittle that down to potential tenants that meet Stag’s investment criteria, its target asset universe is whittled down to $250 billion.

While it owns and/or operates 81.2 million square feet of space across 409 buildings in 38 states, that represents a 1.5% sliver of that target asset universe.

The P/E screener gets yet another REIT wrong, though even by sheer net income, Stag Industrial isn’t as ludicrously overpriced as other real estate plays.

Source: FinViz

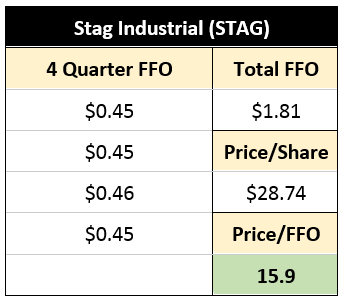

And from an FFO standpoint, STAG’s valuation is downright typical.

Stag has routinely improved its funds from operations, which at $1.81 per share over the past 12 months is more than enough to cover its 11.92-cent monthly dividend.

Stag deals in a large, stable market that’s organically growing thanks to the expansion of e-commerce. The U.S. Census Bureau and Moody’s say e-commerce, which currently makes up just 10% of U.S. retail sales, will rise to 23% by 2025—but only time will tell if this warehousing REIT can stay on course.

Gladstone Commercial (GOOD)

Dividend Yield: 7.1%

TTM P/E Ratio: 931.3

Now, let’s look at a member of the Gladstone family.

Gladstone Commercial (GOOD) is one of a group of public investment vehicles that also include Gladstone Investment Corporation (GAIN), Gladstone Capital Corporation (GLAD) and Gladstone Land Corporation (LAND). As a group, they invest in (and buy) lower middle market companies, and deal in commercial and farmland real estate.

Gladstone Commercial, as the name would imply, is a commercial REIT that invests in a diversified group of single- and anchored multi-tenant properties in 24 states. Its 102 properties are primarily office (63%) and industrial (32%) in nature, though it does have a little exposure to retail (3%) and medical offices (2%). Better still, it has a diversified tenant list that includes General Motors (GM), Automatic Data Processing (ADP) and Morgan Stanley (MS), and no single tenant makes up more than 4% of rent.

Importantly, Gladstone isn’t a passive rent collector. Its management team will actually work with tenants to make value-add capital improvements ranging from repaving parking lots to full building expansions, and even help them reduce their regular operating expenses.

Revenues have steadily climbed the wall over the past few years, from $73.8 million in 2014 to $106.8 million last year. (And Gladstone is on pace for another year of growth.) FFO hasn’t grown as consistently but is up each of the past two years. I’m also willing to give a pass on that given what the company is doing to cut back its leverage.

Source: Gladstone Commercial June REITweek Presentation

What would I pay for a company like this?

Source: FinViz

No. I wouldn’t pay 930 times earnings.

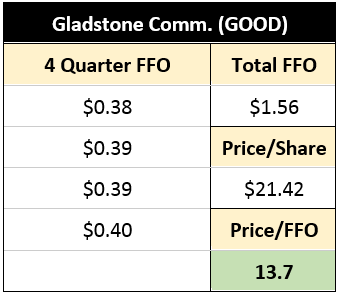

But a price/FFO of less than 14 sounds acceptable for a company with Gladstone’s growth potential? That I can live with.

This REIT has outperformed the Vanguard Real Estate ETF (VNQ) on a total return basis since I last analyzed it early January, and nothing has happened to change my mind.

Gladstone looks pretty good. But I’ve got two ideas that look even better.

Urgent REIT Alert: 2 Picks for 100%+ Gains and 8.9% Yields

Real estate investment trusts (REITs) are such a powerful dividend tool that they can make the difference between just getting by in retirement… and breezing by.

Retirees that have a healthy allocation to REITs clip vacation pictures for their photo albums.

Retirees that don’t? They greet you at Walmart.

But the need to buy REITs for your retirement portfolio has gone from “pressing” to “urgent.” Because my Triple-Digit Profit System just did something it hasn’t done since 2015: It tripped its final indicator for us to dive into a totally ignored corner of the market.

The last time all five of my indicators flashed green (like they are this very minute), the group of stocks I want to show you in my 2019 REIT Playbook—where cash dividends of 6%, 7% and even 8% are commonplace—started red-hot rallies that resulted in triple-digit profits.

One member of this snubbed group of stocks—a rock-steady “landlord” spinning off a 7%-plus cash dividend—did something that income plays just aren’t supposed to do:

It soared for a market-crushing 580% return.

Doubling the Market With Real Estate Sounds Crazy, But …

It wasn’t alone. Another one of these overlooked cash machines produced a total return (so, including dividends) of 379% in just more than six years. You’re lucky to get 100% out of the market in that amount of time.

And because this stock had such a large dividend, a big slice of those returns were in cold, hard cash.

That was four years ago. Fast-forward to today, and the Federal Reserve has put its hand on the easy-money spigot, triggering the last of my five buy signals. And now, I have another pair of urgent REIT buys—boasting triple-digit price potential and yields of nearly 9%—that I want to email to you now.

The payouts are simply “going parabolic,” but it’s important that you add these stocks to your retirement portfolio now. Because when their prices go out, you won’t just miss out on their triple-digit gains—but those dividends will shrink on new buyers by the day.