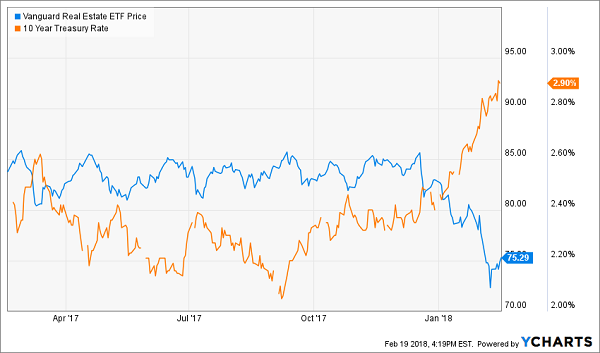

Let’s assume that higher long-term rates (3%+) are here to stay. Can REITs (real estate investment trusts) and high rates co-exist? Or must there be just one winner in this suddenly one-sided tug of war?

After all, as the 10-year Treasury’s yield has rallied, REITs have suspiciously suffered:

REITs and Rates: Oil and Water?

And the headline arguments against REITs during rising rate periods seem to make sense:

- REITs need cheap money to grow, and

- When risk-free assets pay more, income investors will buy them instead of REITs.

These knocks may apply to low-yielding shares, especially static payers, but they historically haven’t applied to firms (REIT or otherwise) that have been able to grow their payouts meaningfully as rates have risen. REITs that have been able to raise their rents have done quite well in rising rate environments – banking their investors up to 160% in total returns in just three years.

How 3 Blue Chip REITs Returned 33% to 160% as Rates Rose

Let’s review the three-year period starting in May 2003 when the 10-year rate climbed a full two hundred basis points – from 3.2% to 5.2%. I don’t think rates will actually get that high this cycle – but let’s consider the possibility.

Back then, familiar rent raisers like Realty Income (O), Simon Property Group (SPG) and Ventas (VTR) climbed higher right alongside long-term rates. Their secret? Their payouts simply outran the steady – but slow – bond market:

Dividend Growth Drives Big Returns (June 2003-06)

Will this rising rate cycle be any different? Only in name – of the REITs leading the charge, that is. The winning strategies remain the same for this rate hike cycle. Buy the stocks of the companies that are:

- Growing their payouts the fastest, or

- Paying the most today.

High Current Yield Can Work, Too

But what if a REIT isn’t raising its rents? How much current yield is enough to buffer the stock against competition from bonds?

In recent years I’ve described “meaningful yield” as 6% or better. But we’re no longer in a 2% world – so we need to adjust our payout standards higher.

For static payers, we should now require a 7% to 8% current yield. This gives us a sufficient margin of safety if long-term rates do indeed run to 5%+.

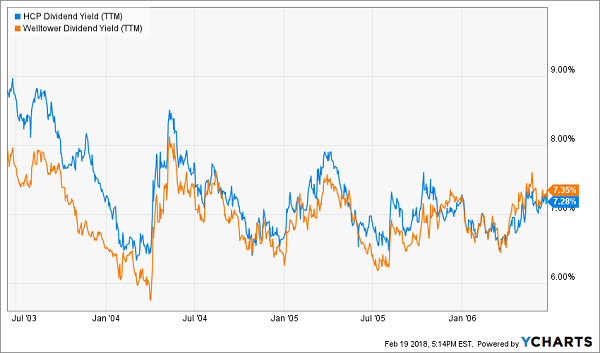

Let’s consider static payers HCP (HCP) and Welltower (HCN), which rang up anemic 2% and 9% dividend growth over our 2003-06 rate hike cycle. They still clocked impressive returns near 50%:

High Current Yield Drives Big Returns (June 2003-06)

Their secret? High initial yields (of 8.8% and 7.9%) which investors actually bid lower (to 7.3% each) as rates rose. In other words, investors paid more for the same dividend three years later – even as the risk-free rate rose to 5.2%!

Investors Bid Yields Down as Rates Rose

7 Rate-Proof & Recession-Proof REITs, Averaging 8.5% Yields (with Upside!)

All seven REITs in my 8% No Withdrawal Portfolio check one of the two “dividend growth” or “high current yield” boxes for rising rate environments (with most actually checking both).

As a group, they pay an impressive 8.5% average yield today. That’s outstanding in a 3% world.

Combine 5% to 10%+ dividend growth with these high-single-digit current yields, and we have a formula for safe 15% to 20%+ annual gains from REITs. With a significant portion of that coming as cash dividends.

And thanks to the new tax plan, there’s never been a better time to buy REITs and live off their dividends.

(REIT investors will benefit from the tax breaks that “pass through” businesses will receive in the new code. Investors will be allowed deduct 20% of their REIT dividend income, which means the 37% tax bill will drop to 29.6%.)

But it’s important to choose your REITs wisely.

Don’t buy low-yielding static payer. Don’t buy a retail REIT, either (with that entire industry is in a death spiral, future rent checks will be dicey for years to come).

Instead, focus on recession-proof firms, such as those that rent hospitals, business lodging and warehouses filled with Amazon packages. Landlords that own properties that will be in high demand no matter what happens to interest rates or the economy from here, in other words.

I’d love to share my seven favorite recession-and-rate-proof REITs with you – including specific stock names, tickers and buy prices. Click here and I’ll send my full 8% No Withdrawal Portfolio research you to right now.