There’s a “delayed reaction” dividend play (for tax-free 5% yields) waiting for us in municipal bonds right now—and it’s not going to last.

I know, I know. “Munis” don’t exactly get most folks’ hearts racing. But the fact that this corner of the market tends to lag behind stocks, bonds and the rest is exactly what’s behind our opportunity here.

Plus, we get to buy cheap and get our dividends monthly when we buy our munis through a closed-end fund (CEF). That’s because most muni CEFs pay monthly—including a 5.3% payer called the Nuveen Municipal High Income Opportunity Fund (NMZ), the particulars of which we’ll delve into below.

First, though, let’s talk about why this opportunity is available now.

The Latest “Bond Bounce” Hasn’t Hit Munis—Yet

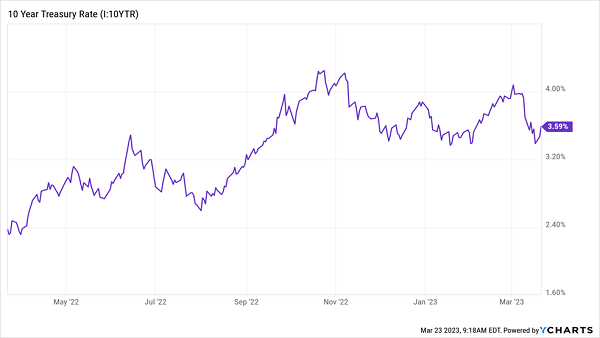

Over the last few weeks here on Contrarian Outlook, I’ve been talking a lot about the “4% ceiling.” It’s the tendency for the yield on the 10-year Treasury to collapse (sending bond prices soaring) once it hits 4%. You can see that over the last year below:

Yields Smack Into the 4% Ceiling (Again and Again)

It’s been one of the (very) few patterns we could rely on in the tire-fire of a year we’ve put in. And we’ve been busy riding it to quick gains (and dividends).

Like when we rode last autumn’s “Bond Bounce” to a fast 5.9% gain, or 28% annualized, between October 7 and December 21 in my Contrarian Income Report service. The key here was our timely swings into, and out of, the iBoxx $ Investment Grade Corporate Bond ETF (LQD).

But here’s the thing: as volatility picked up, our bond bounce plays got faster. Which is why we played this last one (a holding period of just three weeks, from February 23 and March 16) through my Dividend Swing Trader service. Our pick there, the iShares 3-7 Year Treasury Bond ETF (IEF), handed us an easy 3.4% gain in that time.

We can thank Silicon Valley Bank for that one. Its collapse caused the 10-year yield to bounce off the 4% ceiling after scared investors bid “safe” Treasuries to the moon.

The Easy Way to Grab (Tax-Free) “Bond Bounce” Gains

Here’s where the “sleepy” world of munis comes in—because while the latest Bond Bounce has come and gone in Treasuries, it’s still very much alive in munis—especially if we buy through CEFs that hold them.

In fact, we only buy munis through CEFs, for three reasons:

- Higher yields: The benchmark iShares National Muni Bond ETF (MUB) yields just 2%. Better to go with CEFs, where yields of 4%, 5% and up are common—driving taxable-equivalent yields of 7% or more for top-bracket ballers.

- Discount-driven upside: CEFs often trade for less than the per-share value of their portfolios. When those discounts to net asset value (NAV) close, they drive prices higher. That’s not a thing with ETFs like MUB—you’re stuck relying only on portfolio gains for upside.

- Outperformance: The muni market is small, opaque and tough for you and I to access. Not so for CEF managers. What’s more, a well-connected manager gets first crack when the best munis are issued—which is why well-run muni CEFs always crush their benchmarks.

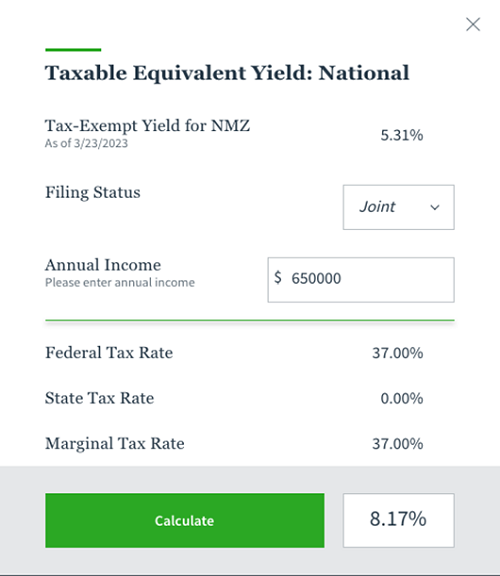

This Muni CEFs’ 5.3% Dividend Could Really Pay You 8.2%

Which brings me back to NMZ, which yields 5.3%—a payout that could be worth 8.2% to you if you’re in the top bracket.

Source: Nuveen

About 62% of the portfolio is rated BB or lower, with the other 38% in the “investment grade” bucket. That’s a nice blend for us, because non-investment-grade bonds are often off-limits to institutional investors, leaving more room for NMZ in the bargain aisle!

Meantime, the 38% in investment-grade paper adds extra stability (in the already very stable muni-bond space).

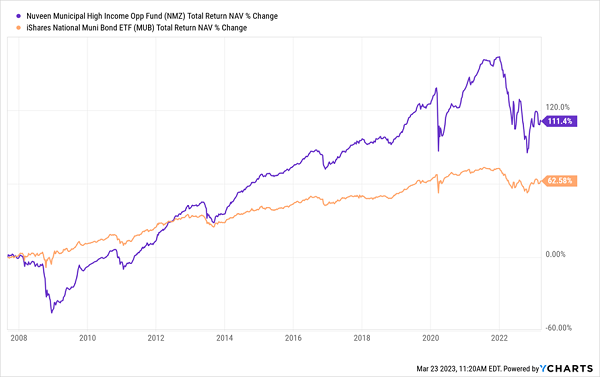

NMZ also has a nearly 20-year history behind it, having been launched back in November 2003. And as we expect from muni CEFs, its NAV return (or the return of its underlying portfolio) has easily beaten MUB since the latter was launched in ’07.

NMZ’s Managers Show Their Mettle

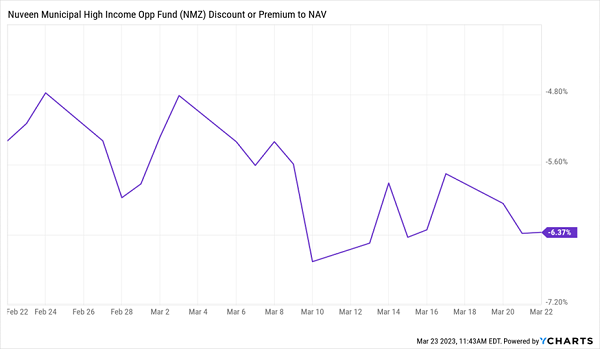

Let’s wrap with solid evidence that our Bond Bounce play is still alive and well here: despite the bond rally, NMZ’s discount has actually grown in the last month, dropping to 6.4%. So we’re essentially buying its 871-bond muni portfolio for 94 cents on the dollar!

Bond Bounce? What Bond Bounce?

As with our previous round of Bond Bounce plays, I don’t expect our deal on muni CEFs to last. In the case of NMZ, its 6% discount is just too far below its five-year average discount of 0.6%. As it narrows, it’ll pull the price up.

Yours Now: A Full Portfolio of 7% Monthly Payers Set to Bounce

NMZ is far from the only monthly payer out there that’s gathering steam in the SVB aftermath.

I’ve got a full portfolio of monthly paying REITs, CEFs and regular stocks that have serious upside as the market recovers from the banking mess. I’ve put them all in my exclusive “7% Monthly Payer Portfolio”—and I want to share everything I have on these income plays with you now.