We’re more than halfway through Year 1 of Trump 2.0, and I stand by what I said before Inauguration Day: This administration has ushered in a stock picker’s market.

In other words, investors who make smart moves into, and out of, individual dividend payers will do the best in the coming three-and-a-half years.

That puts holders of SPY, which must hold the entire S&P 500, in a jam. The S&P 500 trades at a nosebleed 25-times earnings, and SPY has no manager to shift away from overbought names and toward overlooked bargains. That’s dangerous ground.

With that in mind, let’s run through four tickers (all of which, yes, are SPY holdings) I urge you to avoid—or dump if you’re sitting on them now.

2 Food Stocks to Fade as Trump 2.0 Rolls on

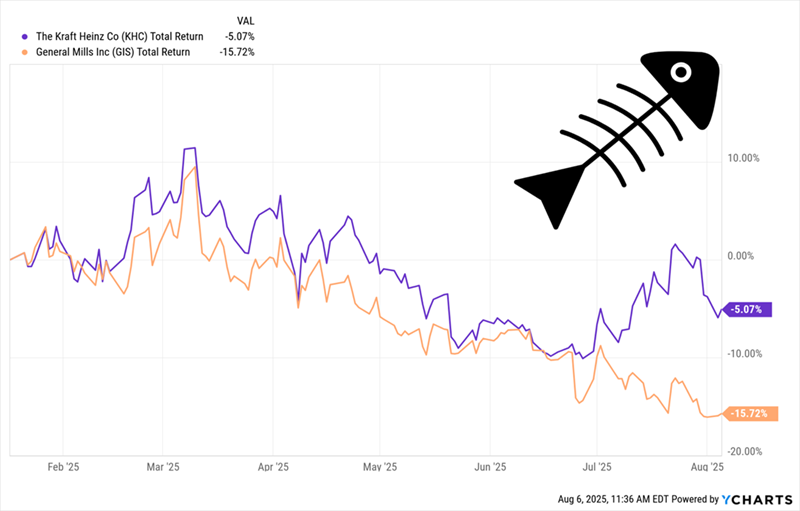

Let’s start with General Mills (GIS) and The Kraft-Heinz Co. (KHC), the latter of which we’ve long criticized for being out of step with the times. Both have fallen hard since Election Day—a period when the S&P 500 has gained.

Now that might trigger your “bargain radar.” If so, let me quickly banish that notion. Because the truth is, buying either of these laggards here would be a costly mistake.

Food Giants Fall Flat in Trump 2.0

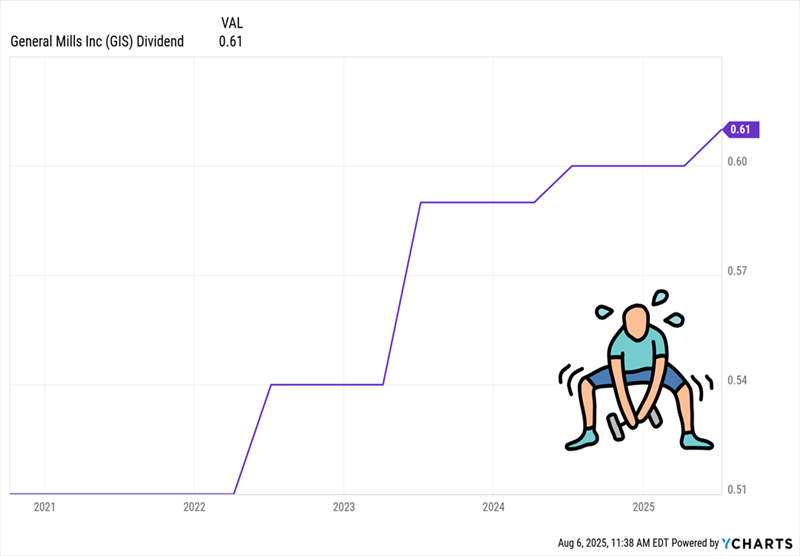

Since we mainly buy blue chip names like these for dividend growth, this duo has naturally fallen off our buy list. General Mills, for example, has seen its payout growth slow sharply, rising by just a penny in each of the last two years:

General Mills’ Decelerating Dividend

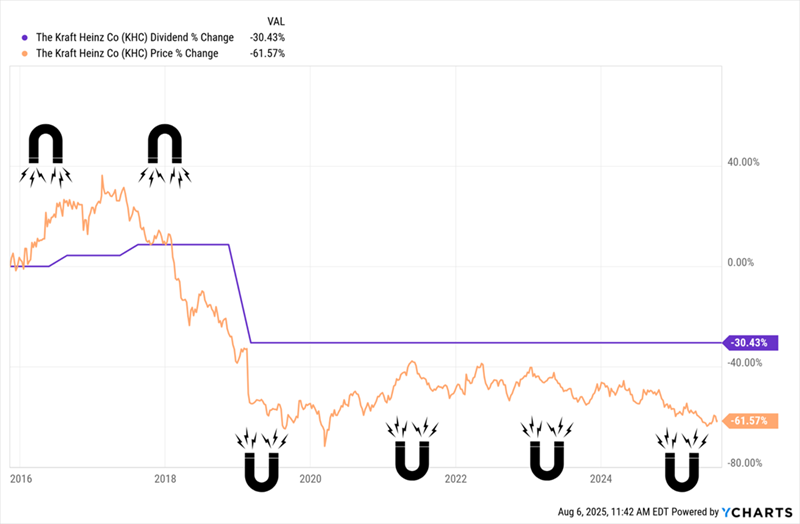

KHC? Its 5.9% dividend yield might grab your attention, but that high yield only exists because the stock has plunged in the last decade (and share prices and dividend yields move in opposite directions).

The last move KHC’s dividend made was actually a cut announced in early 2019, which took the share price down with it. That’s proof positive that our Dividend Magnet—or the tendency for dividend growth to propel share prices higher—also works in reverse:

KHC’s “Reverse Dividend Magnet” Sinks Its Stock

Throw in revenue growth that’s gone nowhere for the better part of a decade and the fact that the company has a negative payout ratio (i.e., paying dividends while losing money over the last 12 months), and the odds of this payout getting off the mat, and giving the share price a lift, are slim.

Now there are reports that KHC is considering spinning off its grocery business into a new firm, effectively undoing the merger that created it in 2015. Normally, spinoffs are good for both the parent and the new company. But in this case, there’s little value to be unlocked by replacing one lagging company with two.

2 Toymakers Facing Tariff (and Demographic) Pain Without End

One thing there’s no doubt about: However President Trump’s team negotiates trade deals from here on out, we can assume that overall tariff rates will be higher than they were during the pre-Trump era.

As a result, companies that source a lot of products in places like Vietnam and China will remain vulnerable.

Two I’m particularly worried about are toymakers Mattel (MAT) and Hasbro (HAS). The tariffs are already affecting their profit outlooks, and there’s a limit to how many toys they can make in America, given the low margins on these products.

Beyond that, though, demographic changes are an overhang, with people having fewer children, especially in wealthier countries. In 2024, for example, there were just over 3.6 million births in the US, according to the Centers for Disease Control and Prevention. That was up 1% from 2023, but it’s still a historically low figure when you consider that 2023’s total was the lowest since 1979.

To be clear, I should say that both companies deserve credit for their efforts to shift production away from China, which has taken the brunt of the administration’s ire on trade. In early May, Mattel execs said they got about 20% of their toys from China, and they aim to cut that to 10% by 2027.

Hasbro gets around 50% of its products from China, with the goal of cutting that below 40% in 2026. That’s still a significant reliance, and you and I both know that relocating big parts of a supply chain isn’t something that happens overnight. Moreover, there are few, if any, other places in the globe these companies can source from in order to avoid tariffs outright.

Beyond that, Hasbro gets a large slice of its sales (about 45% in the second quarter of 2025) from its consumer-products segment, home of its physical toys and games—even as more kids get their fix online.

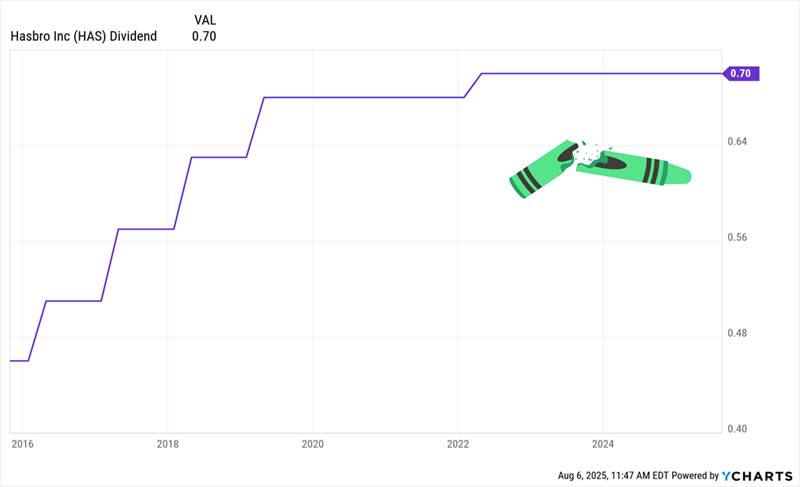

The dividend? The stock yields a “ho-hum” 3.6% today, but its payout has gone nowhere since before the pandemic:

Hasbro’s Broken Payout Streak

Moreover, like KHC, the stock boasts a negative payout ratio. That risks turning slowing dividend growth into something much worse: a payout cut. Mattel, for its part, is off our list because we’re dividend investors first and foremost, and MAT doesn’t pay a dividend, having suspended its payout in 2017.

The bottom line is that the winds have shifted against these two, and there’s no sign of that changing. That’s not only bad news for MAT and HAS—but for our SPY holders, too. But for savvy stock pickers, it sets up opportunities, especially if we look for stocks with safe dividends and strong Dividend Magnets that pull their prices higher.

The Dividend Magnet: Our Roadmap for the Rest of Trump 2.0

There’s one “truth” we can count on, no matter who holds power in DC: A stock’s dividend growth is the No. 1 driver of its share price.

That makes our strategy simple: Buy stocks whose payouts are growing—and accelerating—backed by rising sales, earnings and cash flow.

Even better? Buy when their stock prices “lag” their payout growth. Then we ride along as they “snap back” to catch up.

This is easier said than done, of course: Tracking dividend/share price correlations requires complex charting tools and a lot of time reading earnings reports.

But I’ve done the legwork for you. The result: my 5 top “Dividend Magnet” picks to buy NOW.

These 5 stocks have what it takes to keep both payouts and share prices popping. Click here and I’ll tell you more about these 5 undervalued “Dividend Magnet” picks and give you a free Special Report revealing their names and tickers.