When it comes to the economy, we’re in a bit of a weird spot: The data tells us that, despite inflation fears, interest rates are likely to fall in the year ahead.

Falling rates point in one clear direction for us contrarian income-seekers: corporate bonds. Our preferred way to tap into them? Discounted closed-end funds (CEFs) with big dividend yields.

If investors know any corporate-bond CEFs at all, they probably know the PIMCO Dynamic Income Fund (PDI). It’s the biggest of the bunch, with a $5.1-billion market cap and a monster 13.3% yield.

With that in mind, PDI is a good gauge of investor interest in corporate-bond CEFs, and that interest is booming, as we’ll see in a moment.

First, though, with all the worry that tariffs will cause inflation, you’re probably wondering why I’m saying rates will drop in the coming months, so let’s square that circle first.

My reasoning here is in (small) part due to a drop in consumer confidence, indicating shoppers are indeed pulling back. And yes, that does raise the risk of a recession. Which, in turn, would lead to lower rates.

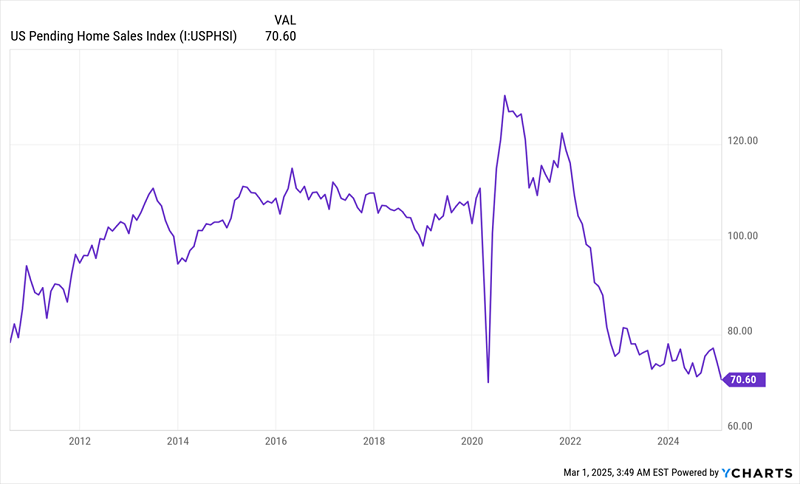

But the real reason for my call for falling rates is something much more concrete: pending home sales in America, which have pulled way back. (Note that falling rates mean rising bond prices, as bonds and rates move in opposite directions, like two ends of a teeter-totter)

Pending Home Sales Dive

The years-long slide means that now-pending home sales are lower than they were at their lowest point during the pandemic.

The reasons why are pretty clear: high interest rates and home prices stuck at pricey levels. While this can persist without causing an economic slowdown for a while, it can’t do so forever. Americans’ wealth is too tied up in the value of their home.

Falling home sales will likely pressure the Fed to cut rates, which would boost stocks and corporate bonds. So this is actually a tailwind for investors while also being an indicator of worsening economic times.

The key takeaway for us is that despite this disconnect between stocks and the economy, we need to be in the market, even if volatility is likely to increase (as it has been in recent weeks). But we also want to build on our stock holdings with other assets, and corporate bonds are a timely pickup now.

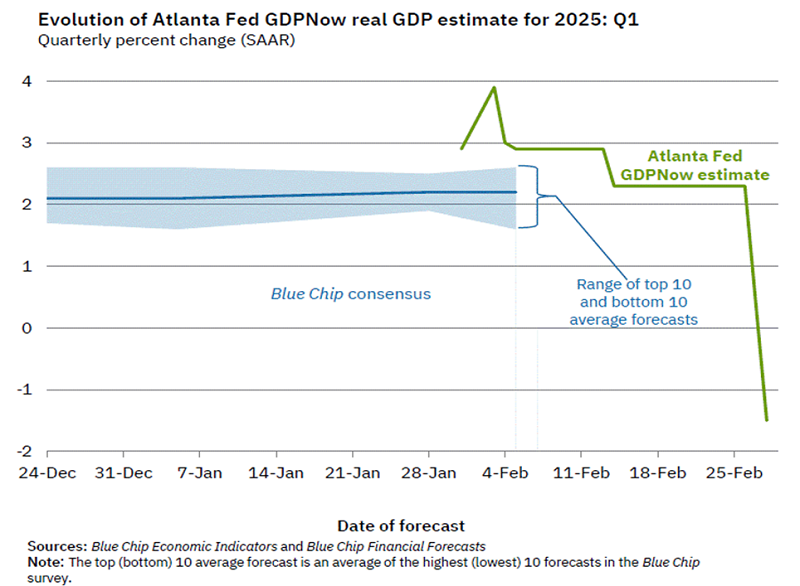

Why a (Mild) Recession is Getting Likelier

This chart suggests that the recession we’ve been waiting for since 2022 might indeed be around the corner.

With data now pointing to a GDP decline in the first quarter of 2025, it is clear there are more risks building up in the US economy after years of inflation, alongside those stubbornly high house prices.

But there’s still plenty of good news, too. Unemployment is still very low, at 4%, and wages continue to grow, at a roughly 5% year-over-year pace.

In short, this tells us the economy may shrink in the first quarter of 2025, but consumers could still spend enough to turn things around.

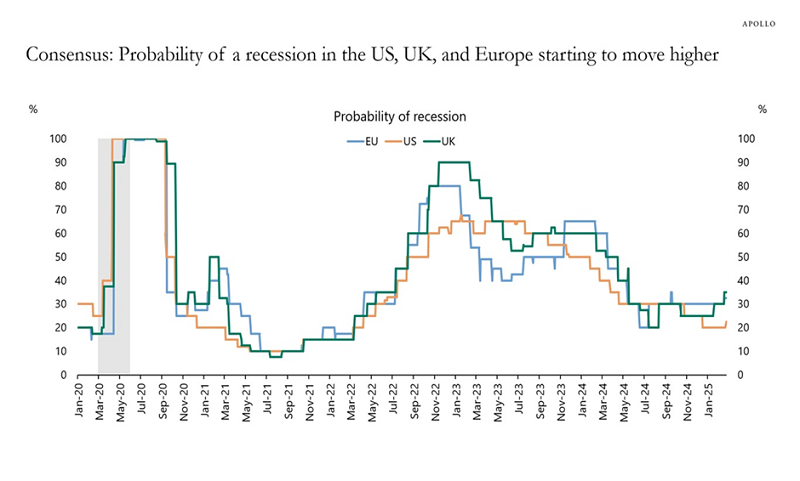

Even so, the overall probability of a recession is trending up, while still staying at a relatively low level—and a much lower level than the EU and the UK.

With America’s economy the best of the bunch and the likelihood of recession still at a meager 25% percent, it’s time to be just a bit more cautious.

What to Do Now

Economists call this “mid-cycle,” where we’re not recovering from a downturn (as in 2023 and 2024), but it’s not an obvious time to go on a stock-buying binge, either.

This is where corporate-bond CEFs come in, for three reasons.

- High yields. With an average 6.9% coupon yield, investors in high-yield corporate bonds get a lot of cash from their holdings. And that cash stream is relatively safe, with corporate-default rates still very low.

- The Fed’s future moves. If the Fed is going to cut rates faster in 2025, as housing data suggests, companies that issue bonds will find them easier to pay off. That lowers risks for investors, who will see the value of their holdings rise as rates decline.

- Movements out of stocks. If we see more short-term volatility, we’ll see more demand for corporate bonds. That means anyone owning them today will have more buyers tomorrow, and the law of supply and demand means prices will rise as a result.

This has already been happening.

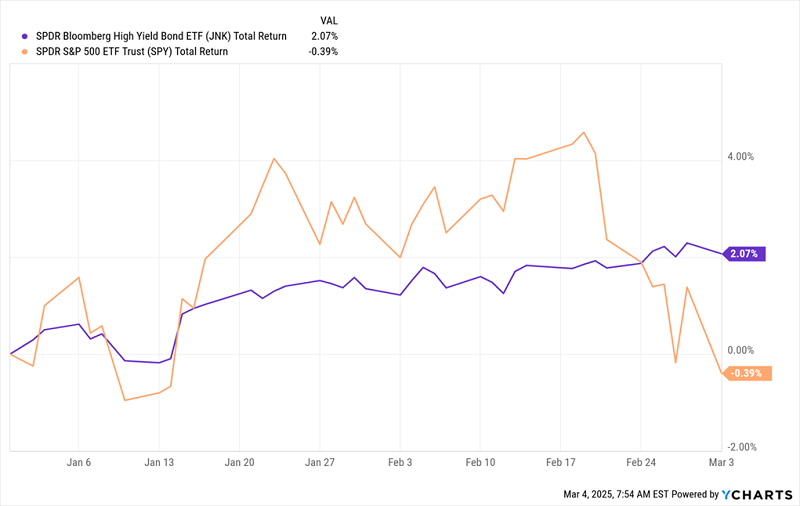

Junk Bonds: Out of the Dumpster

With the corporate-bond market boasting high yields and stocks looking priced to perfection, the corporate-bond benchmark SPDR Bloomberg High Yield Bond ETF (JNK) is beating the S&P 500 in 2025, as I write this. That’s an incredibly rare (honestly, a better word would be “bizarre”) occurrence.

That is likely to continue if stock volatility keeps up, with investors looking for income and realizing the low default rates among these assets make them very compelling.

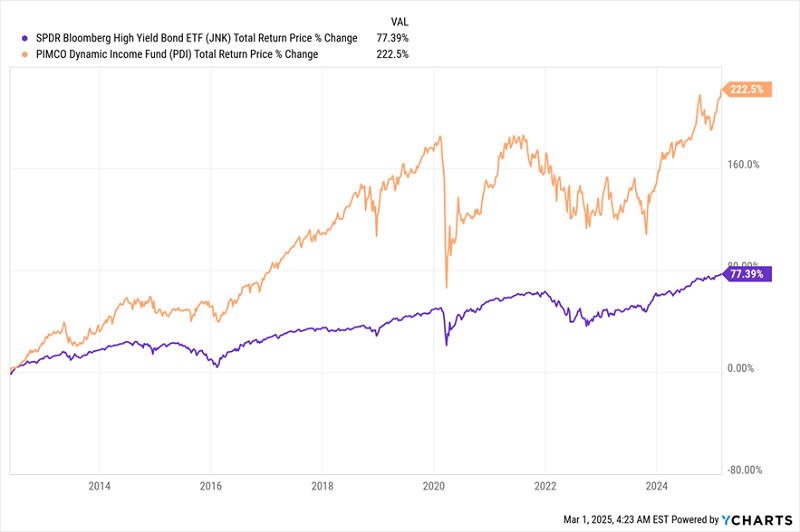

JNK is not your best option to capture this trend, however. CEFs are. The biggest of them, as mentioned, is PDI, and it tells the tale of CEF superiority here, tripling JNK’s performance since its inception back in 2012. That’s helped PDI’s assets under management balloon to $7 billion while the fund also pays out that 13.3% dividend.

PDI Keeps Growing and Growing

That growth is key because it means PDI is attracting more attention to CEFs as a way to invest in high-yield bonds. That, in turn, is driving up demand for all corporate-bond CEFs. And that is causing their discounts to net asset value (NAV, or the value of their underlying portfolios) to shrink and, in an increasing number of cases, turn into premiums.

That’s another way of saying that already cheap bond CEFs are getting “less cheap” and boosting their total returns as that happens.

These 5 CHEAP CEFs Drop Monster 10%+ Divvies, Pay Monthly

The really cool thing about CEFs—including PDI above—is that many of them pay us dividends every single month.

So not only are you getting access to double-digit yields here, but you’re saving yourself the time (and hassle) of managing a “lumpy” income stream from quarterly payers, too!

This is a good time to go over all the benefits that monthly dividend CEFs give us, so let’s do that:

- Big yields (of course!), giving us more of our return in safe dividend cash.

- Discounts to NAV (letting us buy in and ride along as those discounts flip to premiums, driving our returns higher as they do).

- Instant diversification (for even greater safety), and …

- MONTHLY payouts (for extra convenience).

With all that in mind, it’s no wonder why wealthy investors favor CEFs. AND we can get the same access to them that billionaires do, since these funds trade on the public markets.

I want to give you a head start with my 5 top picks among monthly paying CEFs. I’ve hand-picked these 5 winners for their high yields (I’m talking 10% average yields here), deep discounts and, yes, rock-solid monthly payouts.

You do not want to be without these sturdy income plays in the volatile years ahead. Click here to learn more about them and download a free Special Report revealing their names and tickers.