If anything taught me that buying real estate through stocks—or better yet high-yielding closed-end funds (CEFs)—is way better than brick-and-mortar, it was my experience renting my Manhattan apartment on Airbnb (ABNB).

If you’re reading this, you might feel the same way. Maybe you’ve had the same experience as the one I’m about to share.

It was about a decade ago, and it was, in short, a nightmare. It seemed like every time I turned around, there was a complaint that the place was too small, or someone had posted a bad review. Or I was staring down a pile of clean-up in the wake of careless renters.

To be fair, maybe the renters had a point that I wasn’t the best landlord. Even then, I was more interested in income investing!

In any event, I quickly concluded what many landlords do: Managing real estate (or doing so the right way, at least), calls for professional staff and management. And besides, as a renter of just one condo, I had little diversification—I was at the whim of the city’s condo market.

Speaking of professional real estate investors, there are signs they’re becoming a problem not only for individual landlords but also for families simply trying to buy their first home. According to a 2023 study by MetLife Investment Management reported by CNBC, institutional buyers may control a full 40% of single-family homes available for rent in the US by 2030.

These well-bankrolled firms are snapping up many of the best condos, and even single-family homes, in major markets.

I don’t know about you, but having little diversification, a lot of work, stiff competition and the hassle of dealing with renters, sounds like running a business—and a tough one at that! Which brings me back to my view that most people are better off with publicly traded CEFs that hold REITs. I base that on three factors (besides the fact that CEFs don’t ask us to do any work!):

- Big dividends: CEFs yield around 8% on average as I write this, with plenty of REIT-focused CEFs paying into the double digits, as we’ll see in the example below.

- CEFs are very diversified. Forget one or two houses or condos—CEFs often own hundreds of REITs that themselves hold hundreds of properties (from homes to malls).

- We get a “double discount” on real estate with CEFs. The first is on REITs themselves, which have lagged the S&P 500 since the pandemic. The second comes from CEFs’ discounts to net asset value (NAV). This essentially means these funds’ portfolios are worth more than their price on the open market.

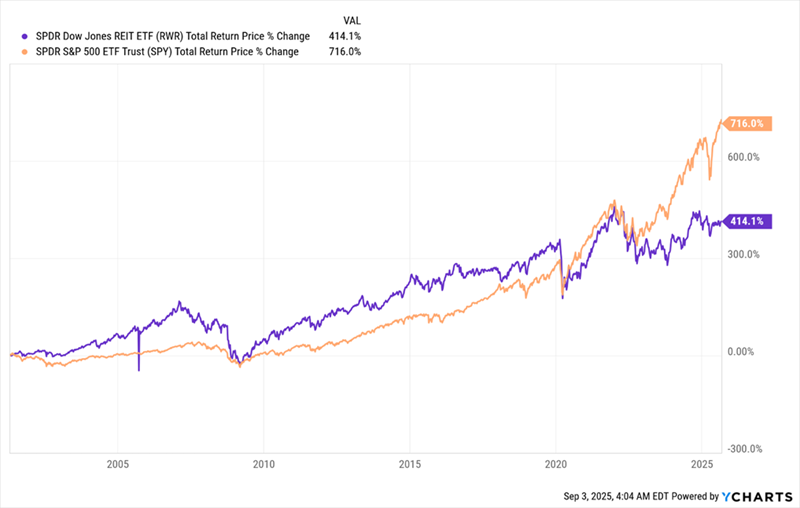

Let’s break down that REITs underperformance a bit more. You can clearly see it in the purple line below, showing the total return of the benchmark SPDR Dow Jones REIT ETF (RWR).

REITs Lead, Then Trail the S&P 500, Giving Us Our “In”

As you can see, from the early 2000s to the pandemic, REITs beat the S&P 500 (in orange) by a wide margin. When you consider that this period includes the subprime mortgage crisis of 2007–2009, you get a sense of the hold real estate has on investors’ imaginations.

REITs bounced back from that mess and resumed their outperformance, which continued up to the pandemic. The reasons for that post-2020 lag included lockdowns, high interest rates (REITs borrow to expand, and higher rates cut their margins), work-from-home and worries about a recession (which, as we repeatedly predicted in this space, never came to pass).

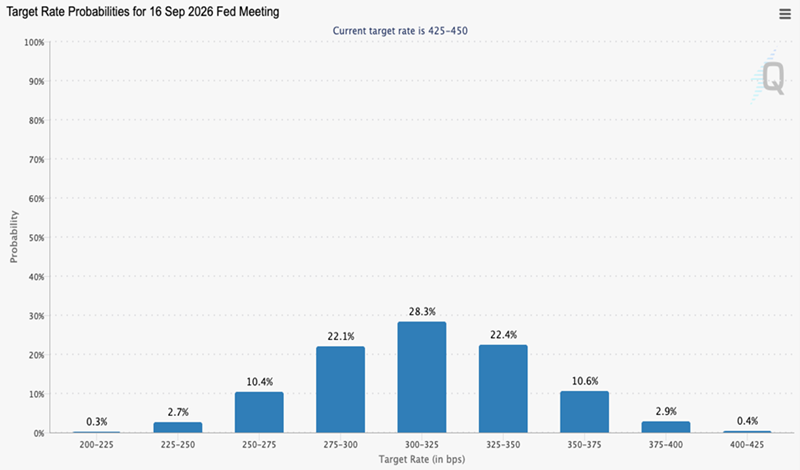

All of these weaknesses are either gone or fading fast. Lockdowns (thankfully!) are a dim memory. The Fed is likely to cut rates as soon as September. By this time next year, in fact, futures traders see the Fed’s target rate a full 150 basis points below where it is now.

Source: CME Group

Work-from-home? It’s obvious that’s fading fast, too, with more firms saying it lowers productivity and, let’s be honest, empowers workers a bit more than most employers would like.

All of this should kickstart real estate demand, which is why RWR (again in purple below) has started to recover in the last few months, although it’s still well behind the S&P 500.

We’re Still Early in REITs’ Redemption Story

Many people invest in REITs through RWR, which holds blue chip REITs like warehouse owner Prologis (PLD), data-center landlord Equinix (EQIX) and senior-care REIT Ventas (VTS). RWR also yields 4%, far ahead of the S&P 500’s 1.3%.

But we can do much, much better with CEFs. Consider, for example, the Nuveen Real Asset Income and Growth Fund (JRI), a holding of my CEF Insider service.

JRI is about as diversified as real estate plays come, with 460 holdings, including well-known REITs like senior-care specialist Omega Healthcare Investors (OHI), mall owner Simon Property Group (SPG) and Gaming & Leisure Properties (GLPI).

The fund also goes beyond REITs, to infrastructure plays like pipeline operator Energy Transfer LP (ET), which stands to benefit from the Trump administration’s increase in drilling permits. There are even utilities, like Dominion Energy (D). JRI has benefited from utilities’ big recovery since 2023, and more gains are likely, in part due to AI’s voracious power demand.

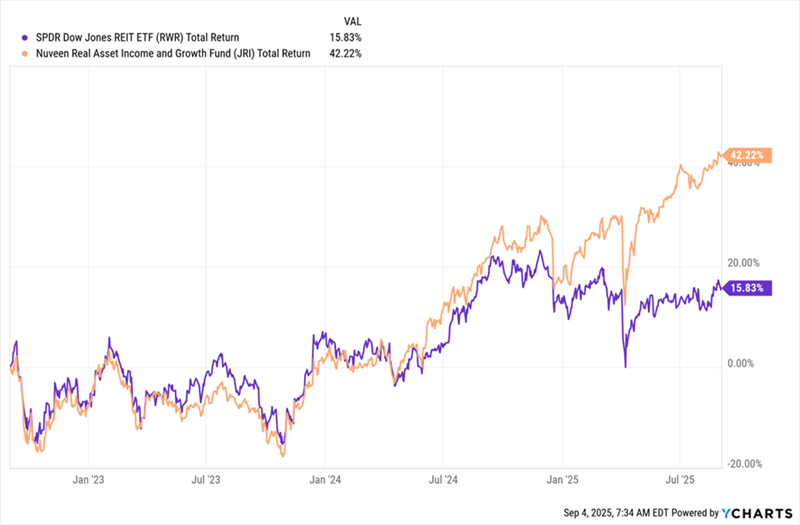

On the performance front, we see that JRI (in orange below) has posted a return nearly three times that of RWR (in purple) over the last three years, with dividends reinvested:

JRI Rebounds, Trounces Its Benchmark

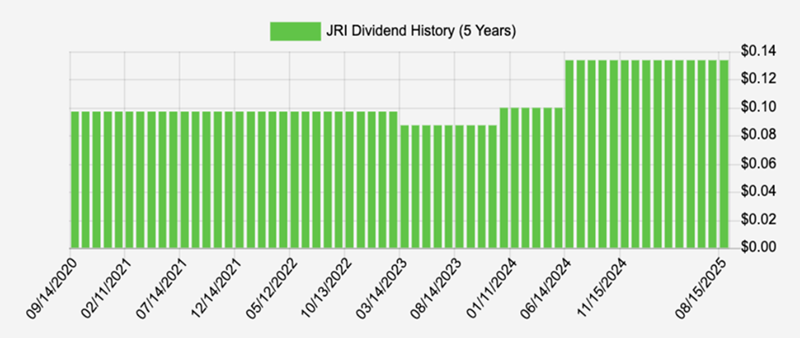

Speaking of dividends, JRI yields 11.9% today and pays dividends monthly. Moreover, Nuveen (a well-established CEF manager) has boosted JRI’s payout in the last five years.

An 11.9% Dividend That Grows

Source: Income Calendar

Sure, the payout did dip a bit in 2023, but it was modest (and understandable, in light of the sharp rise in rates). And management more than made up for that with two sizeable hikes, starting in late 2024.

Finally, the discount to NAV. As I write this, JRI trades around par, but with the tailwinds forming behind real estate, I expect a premium from this fund in the future. That should give its market price a lift, beyond the growth I expect from its portfolio of REITs and infrastructure plays.

All of this makes now a good time to buy JRI, collect its 11.9% dividend—and let management run the fund’s impressive real estate portfolio for us.

Urgent: These 4 Funds Are the Last Cheap AI Plays (And They Yield a Massive 9.7%!)

REITs are overlooked, but there’s a second, even better, income opportunity waiting for us now in AI.

It’s true! Fact is, AI investments are perfect for generating income. The 4 AI-focused funds I’m pounding the table on now prove it. These incredible income plays yield 9.7% on average. That’s nearly 10% of your upfront investment back in your hands, in dividends alone, every year!

AND these 4 criminally overlooked AI funds are terrific bargains, to boot!

I can’t wait to share all the details on these four 9.7% payers with you. Click here and I’ll tell you more about them and lay out for you, step by step, my personal plan for tapping the AI megatrend for huge dividend payouts.