The 10-year Treasury yield’s latest journey to the stars is setting up a terrific opportunity for us to “lock in” historically high dividend yields—and upside, too.

The time to make our move is now. Here’s why: the surging yield on the “long bond” has hit stocks—especially dividend stocks—hard. But this surge is completely unsustainable.

Look, over the last few weeks, I’ve been saying the 10-year would bump its head on the “4.3% ceiling” and retreat. The fact that it’s blown through that ceiling only means its coming fall will be that much harder—and our favorite dividend stocks will rip that much higher in response!

We don’t need to get too far into the economic weeds here: GDP, CPI, PCE—it’s all TMI!

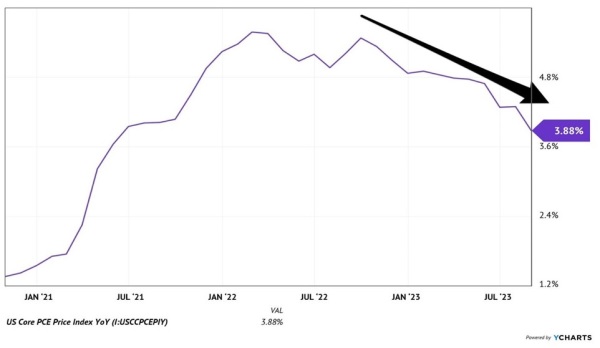

Here’s the upshot: this latest run in the 10-year yield is overdone because inflation isn’t really in a spiral higher. In fact, it’s the opposite. Core PCE (personal consumption expenditures—ok, we do have to talk at least one economic indicator) is falling fast:

Inflation Spiking? Fed-Preferred Measure Says the Opposite

This is the Fed’s preferred inflation indicator, which excludes food and energy prices. Which, some argue, is not appropriate because oil prices are high again.

I disagree that high oil is worrisome for inflation. Future inflation, that is. Fact is, high crude slows the economy. It probably already has, which is why we’ve seen crude fall off in the last few days. And the Fed’s rate-hiking mission will bring a recession.

Then, when the economy slows, the Fed will ease rates. And rate-sensitive stocks (read: dividend payers) will skyrocket from their current lows.

Here are two that have been (overly) washed out in the 10-year Treasury yield’s rise, making now a tempting time to buy and lock in their (temporarily) elevated yields.

This Dividend-Growth REIT Is Flashing 3 Proven Buy Indicators

In the short-term, REITs trade like bonds, which is why they’ve taken a header in the latest rate jump. But they’re even better because they’re real businesses with predictable cash flows, and dividends that often grow.

These days, we’re particularly keen on industrial REITs for one reason: the onshoring (mega)trend, which is driving more companies to pull out of basket cases like China and Russia and return to friendly US shores. They’re also nicely positioned as online shopping—the Energizer Bunny of investing trends—keeps on growing.

The biggest of the warehouse-owning bunch is Prologis (PLD), which has a staggering 1.2 billion square feet of manufacturing and warehouse space across the US. PLD yields 3.1%, which is okay, but focusing on that number misses the point.

Here’s the real story on that yield: it’s the highest it’s been in five years—and since yields move in opposition to prices, it’s our first indicator that this one is overly washed out.

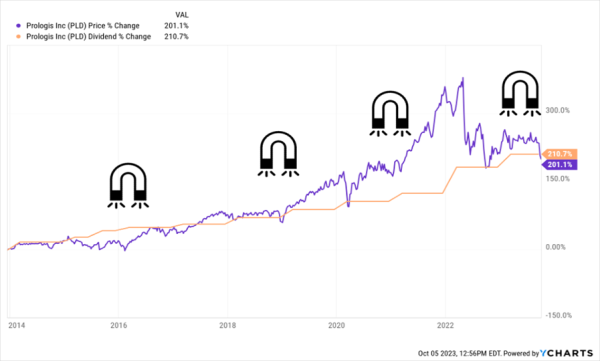

That fact becomes clearer when you see that its payout growth has found another gear lately. Check out the two larger-than-normal hikes on the right side of the chart below.

PLD’s Dividend Magnet Keeps Getting Stronger

Those confident payout hikes from management are our second indicator. There’s something else about this chart I want to draw your attention to, as well.

See how every time the stock drops below the payout trendline, it quickly bounces back?

The fact that PLD’s price is again behind its payout growth is our third indicator that it’s undervalued. Once the extreme fear we’re seeing bleeds out of the market, investors will bid the price back up above the payout, pushing the yield back down to its normal level in the mid-2% range.

Of course, we can’t talk about REITs without addressing borrowing costs, as they tend to carry a fair amount of debt to build and maintain their properties. This is why first-level investors often shun REITs when rates are high, and that’s been the case with PLD, which is about 3% below where it started the year.

But PLD’s balance sheet is tight, with debt amounting to just 25% of its market cap and 30% of assets. Those kinds of numbers are rare in REIT-land, and they’re enough on their own to wash away any worries about high rates.

It gets better: PLD pays a weighted average interest rate of just 2.9%, with a weighted average term of 9.7 years. And it has no major debt maturing until 2026.

Which brings us back to onshoring, which has had PLD’s warehouses 97% occupied as of the end of August. And the REIT’s steady rent hikes, thanks to a lack of warehouse space in the US, are expected to boost cash flow by about 8% this year.

All of this makes the stock’s latest pullback a buying opportunity. But that will end fast once the 10-year Treasury yield starts its descent back to earth.

This Big-Tech Dividend Is Finally on Our Radar

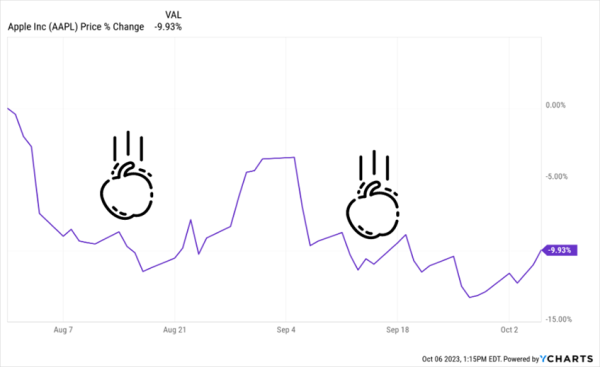

Normally, big-tech dividends don’t excite us here at Contrarian Outlook. Their current yields are just too small! But Apple (AAPL) is grabbing our attention after tumbling a stunning 10% from its all-time high, which it just hit on July 28, 2023:

Apple’s Overdone Plunge

See the stock’s momentum picking up on the right side of that chart? It’s a clear sign the herd is starting to pick up on that fact—and that nicely sets us up for quick gains here.

To be sure, the Cupertino colossus is no star on the yield front, paying around 0.6%. That’s the price of popularity!

But it’s tough to argue that Apple is not a value-creation machine. Share buybacks? Check. Tim Cook & Co. continued to repurchase the company’s stock, thereby lowering the number outstanding (purple line below) through the 2022 mess, at a sweet bargain, too.

Apple Knows Its Own Stock Better Than Anyone

That move looks particularly smart now, after the stock was caught up in the AI-powered run-up this year.

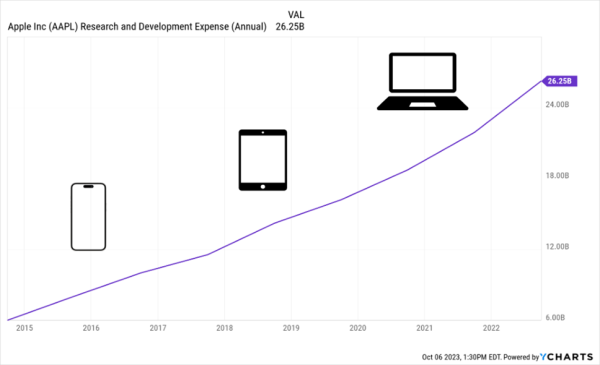

More impressive, the company manages to fund these buybacks and grow its payout (up 120% in the last decade) while funding the massive R&D spend it needs to keep leading the tech sector: from its 2015 fiscal year through fiscal 2022, it’s boosted research spending more than threefold, from $6 billion to $26 billion.

Apple’s Relentless R&D Spend

To be sure, this one doesn’t look cheap on a P/E basis, trading around 29-times trailing-12-month earnings as I write this.

But when a reliable cash generator like this (free cash flow is up 128% in the last decade) with a massive cash hoard ($165 billion as of April) takes a 10% header in weeks, it’s got to be on your radar. Especially as Treasury yields ease off, throwing a big lift under the rate-sensitive tech sector—and its undisputed leader.

Incredible Income Play Could Send You $1,000 in CASH in Days

As I write this, one of my top dividend plays is drawing up a list of savvy investors lined up for its next massive payout.

You do not want to be left off of it!

With a reasonable upfront investment here, you could trigger a regular monthly payout of $1,000. Invest more and you could see that shoot up to $2,000, $3,000 and beyond!

Like the two stocks above, this income play’s shares are primed to rip higher as the 10-year Treasury yield cools. The time to buy—and lock in this fund’s life-changing dividend payout—is now!