Today I want to go over what the economic data is telling us about the future of the financial markets in 2024.

Truth is, we are likely inching toward a recession, which means it’s time to be a bit more cautious. But at this point I only see us “backing into” a recession—and likely not till 2025, 2026 or maybe even later.

The upshot here is that when a recession does hit, we’ll want to make sure we have a steady income stream so we can keep on collecting our high payouts right through to the other side. As part of this strategy, we’re going to “lock in” the 8%+ yields (often paid monthly) available on some of our favorite closed-end funds (CEFs) while they’re still cheap.

Before we talk about a recession, though, let’s put this prediction in context, because it relates to economic forecasts I’ve made early in the last few years since the pandemic. Plus, this exercise gives you a good chance to see how right or wrong I’ve been on my calls over the last few years.

Let’s start with a prediction I made back in the first quarter of 2021.

My Prediction for 2021: A Big Stock Rally

In March 2021, when vaccines were being distributed and most investment experts were pivoting away from focusing just on medical data and more on economic data, I wrote in a March 25 Contrarian Outlook article that I saw a future of major gains, particularly for tech stocks.

My rationale was that newly freed-up shoppers were going to engage in a kind of mass consumption to make up for lost time. Back then I wrote:

“Truth is, today’s setup, with tech stocks as a whole still lagging the broader market, reminds me a bit of where tech was a year ago—as lockdowns kicked in, investors sold off the sector, totally missing the boat on what a critical lifeline tech firms would be, for everything from connecting with loved ones to shopping, in the following months.

Fast-forward to today and the strong clip of vaccinations in the US means more Americans will be getting out of lockdowns and quarantines, many with fresh stimulus checks in their pockets. They’ll still be dropping that cash online, and the spending spree will also fuel advertising-focused companies like Amazon (AMZN), Alphabet (GOOGL) and Facebook (FB), as shoppers use their services to hunt for the goods they’re after.”

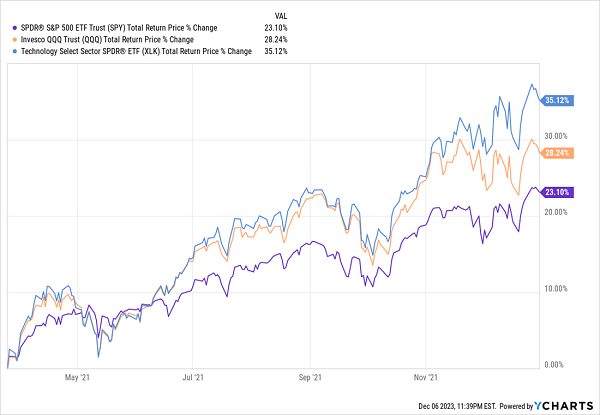

That year, the benchmark ETF for the technology sector, the Technology Select Sector SPDR ETF (XLK), in blue below, outperformed those of the tech-heavy (but not tech-exclusive) NASDAQ 100 (in orange) and S&P 500 (in purple).

Tech Outperforms as Promised

The prediction was clearly correct, but my suggestion in that March 25, 2021, article to moderate this exposure with a CEF that was not entirely tech-focused, the Eaton Vance Enhanced Equity Income Fund II (EOS), proved to be too conservative, closely matching the S&P 500’s 22.8% total return.

For that reason, let’s rate this prediction a B on an A-to-F grading scale.

My Prediction for 2022: Strong Economic Data Would Top Drummed-Up Fear

As we all know, 2022 proved challenging, as the media (both professional and amateur pundits across social media) began to fan the flames of fear.

In a March 7, 2022, Contrarian Outlook article, I highlighted this as a risk factor:

“With so many strong economic indicators and a lot of earnings growth behind us, stocks should be going up. So why aren’t they?

While geopolitical chaos is definitely a drag in the short term, stocks began falling before the Ukraine crisis, as investors weighed the risks of inflation to the broader economy. That risk was augmented in article after article in the press saying that skyrocketing prices for food and gas were driving more people into economic stress.

The only problem? This isn’t exactly true.”

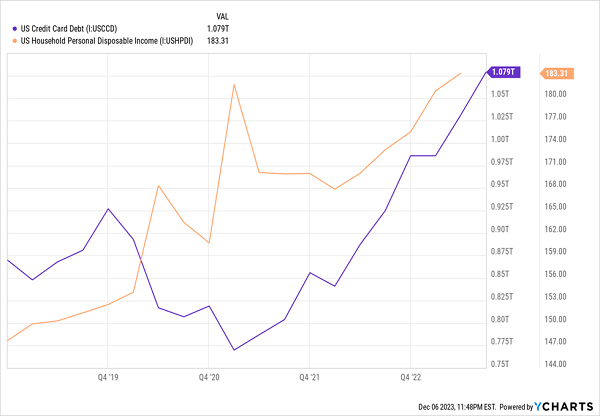

I then pointed to credit-card debt and personal-income levels to show that Americans were getting richer and not getting more dependent on high-interest debt, two clear indicators of a strong economy.

This turned out to be kind of right.

Richer Americans With More Debt

Because the Federal Reserve raised interest rates to a high level very quickly, banks were able to raise interest rates on credit cards. The media then reported that this was the result of inflation making Americans poorer and more reliant on credit cards, hence the cries for a recession in late 2022. And hence the 100%-recession chances in 2023 that we heard about in late 2022 (and our forecasts at CEF Insider that those stories were wrong).

In the end, our call was correct, but the financial media created a false narrative throughout 2022 that caused more panicked selloffs than I’d expected.

For this reason, let’s give this prediction a C.

My Prediction for 2023: The S&P 500 Would End the Year Up 20% to 25%

Okay, sometimes my predictions can be a bit “macro,” so at the start of 2023, I wanted to do something different: make a public prediction that was clearly and easily verifiable.

So I went on a podcast. The episode was released on February 9, 2023 (it was recorded not long before that) and in it I say:

“The market has begun to realize that [there won’t be a recession], so that’s why the market soared in January.

I think that momentum is most likely to continue. We’re going to have corrections, of course—we can’t end the year up 100%—but, you know, could we end up 30% like we did in 2013? I think it’s pretty possible. More probable is we end the year up, you know, 20% to 25% for the S&P 500, that’s what I’m targeting.”

(You can listen here–I begin to say this at 57:20).

How did I do?

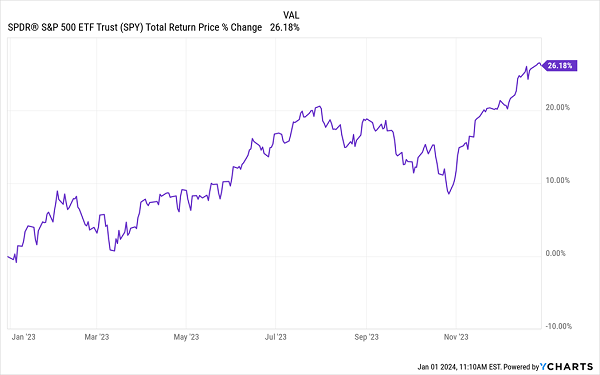

Did We Get 20% to 25% Gains?

At a 26.18% total return, the S&P 500 ended up a little above the range I predicted, so let’s maybe give this prediction an A-.

My Prediction for 2024: The Economy Will Ease Into a Late-Year Recession

Currently, a number of macroeconomic data points are suggesting we are flirting with a recession in the next 12 months. And while there’s no way to know if it will hit in 2024—I am leaning toward it hitting late this year in unnoticeable ways at first—it could come in 2025 or 2026. Maybe even 2027.

What does that mean in practice? It means being able to harness volatility by, for instance, protecting your portfolio from being solely exposed to stocks without an income stream.

Look at, for instance, using a covered-call strategy across the entire market with the Nuveen S&P 500 Dynamic Overwrite Fund (SPXX), which yields 7.8% as I write this. Selling covered calls is a smart strategy that adds extra income, and helps bolster the high dividend payout from SPXX, which, as the name suggests, holds the companies in the S&P 500.

Another option is to pick up a portfolio of high-yielding, low-risk municipal bonds like the 9.3%-paying Guggenheim Taxable Municipal Bond & Investment Grade Duration Trust (GBAB). Or, if it suits your portfolio, consider a more aggressive, high-yielding tech fund like the BlackRock Science and Technology Term Trust (BSTZ) which yields 7.4% and trades at a 22.4% discount to net asset value (NAV, or the value of its underlying portfolio). That big discount means we’re picking up BSTZ’s holdings, including stocks like NVIDIA (NVDA) and Tesla (TSLA), in addition to stakes in a number of private-equity firms, for 78 cents on the dollar.

In other words, there are plenty of ways to invest in the economy we’re facing now, which is more prone to a pullback, sure, but still looking strong in the short and medium term. And with high-income, diversified portfolios, you can build a healthy income stream to get you through for future corrections without selling and missing out on gains before that happens.

Recession or No, We Want High Dividends (and We Want ’Em Monthly)

I’m sure I don’t have to tell you that when it comes to dividend payers, the rare birds that pay us every single month are in a league of their own. After all, when we get our payouts every month, we can divert that cash toward our bills as soon as they come in.

What’s more, monthly payouts are a sign of management confidence—and that’s something we want all the time—especially in an economy that could downshift in the coming months.

With all that in mind, I’ve assembled a FREE Special Report naming my top 5 monthly paying funds to buy now. Yielding 9.2% on average, these 5 stout payers have what it takes to keep our income stream strong, no matter what comes our way.

Click here and I’ll share the details on these unique income plays and give you the opportunity to download that Special Report, which names names, gives you the tickers to track and hands you a full breakdown of each fund, including current yields, discounts and more.