I’m regularly struck by something American investors always seem to take for granted: The many choices we have available to gain financial independence.

And investors in closed-end funds (CEFs) make the most of these choices. These high-yielding funds kick out 8%+ dividends on average, and the portfolio of my CEF Insider service, which helps investors make the most of CEFs, pays even more, with its 18 holdings paying a rich average yield of 9.4%.

Plus, these funds offer stock-like upside, which makes them pretty much tailor-made for delivering financial freedom.

We’ll sketch out how two specific CEFs can help you find your way to an earlier, richer retirement in a bit. But first, back to that embarrassment of choices I mentioned a second ago.

What American Investors Take for Granted

Back in my 20s, when I was studying to get my PhD in Europe, I was told I had to pay into the national pension fund, and I would get that money back when I qualified for it. At that time, I qualified at 62, which seemed absurd—nearly 40 years for me (a severely underpaid academic!) to get back money I desperately needed today.

But as it turns out, I was lucky.

Europe’s mandatory retirement age is rising. Denmark, which currently has the oldest retirement age in Europe at 67, is raising that to 70. Germany, where a normal retirement age is currently 66, is discussing raising that to 73.

Whether you like the life of a worker or not, I’m almost certain that you like having the ability to choose that life without having to worry about governments changing the rules on you mid-game.

A Look at America

This lack of choice pushed me away from Europe in my 20s and led me back to America. Here’s what I found when I returned.

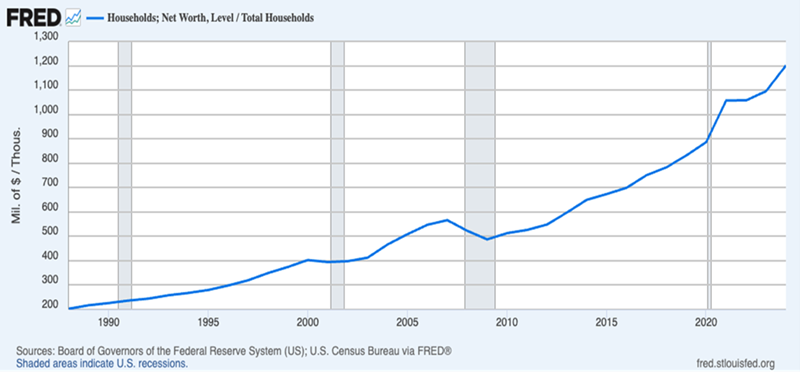

This chart shows that the average American household has gone from $200k in savings in the 1980s to $1.2 million now—and, no, that isn’t due to inflation. That $200k in savings would be $535k in 2025 dollars, so more than half of the jump to $1.2 million is due to actual value being created.

Of course, that wealth isn’t going everywhere. While all households have gotten richer on average, the top 0.1% of the population is attracting a greater proportion of overall wealth in the US, now near 14%.

The ethics of this aside, it’s clear that the households that have more wealth now have more choices—about when to retire, where to live, what lifestyle to adopt and so on.

In a way, it seems like Europeans have too little choice and Americans have so much that retirement investing can be tough for individual investors to navigate without either taking undue risks or locking themselves into weak returns.

CEFs: Your 8%+ Paying “Mini-Pension” (With Upside)

This is where CEFs come in, with their focus on assets from well-established companies. Plus their high yields almost act like a “mini-pension,” boosting your income without leaving you at the whim of the government.

This is the way I viewed CEFs in my late 20s, when I began using their high dividends to get the income I needed to make the choices I wanted. I still view them this way.

And in addition to their big dividends, these funds often chalk up strong returns, too, thanks in large part to their discounts to net asset value (NAV, or the value of their underlying portfolios). As these discounts—which only apply to CEFs, by the way—shrink, they put upward pressure on the fund’s price.

And the best part is that CEFs are easy to buy, trading on public markets just like stocks.

Consider the first CEF we’re looking at today, the Adams Diversified Equity Fund (ADX). It’s one of the oldest funds in the world, tracing its history back to the 19th century (and is a current CEF Insider holding, too).

This one is about as blue chip as it gets, with stocks like Microsoft (MSFT), Amazon.com (AMZN) and JPMorgan Chase & Co. (JPM) among its top holdings.

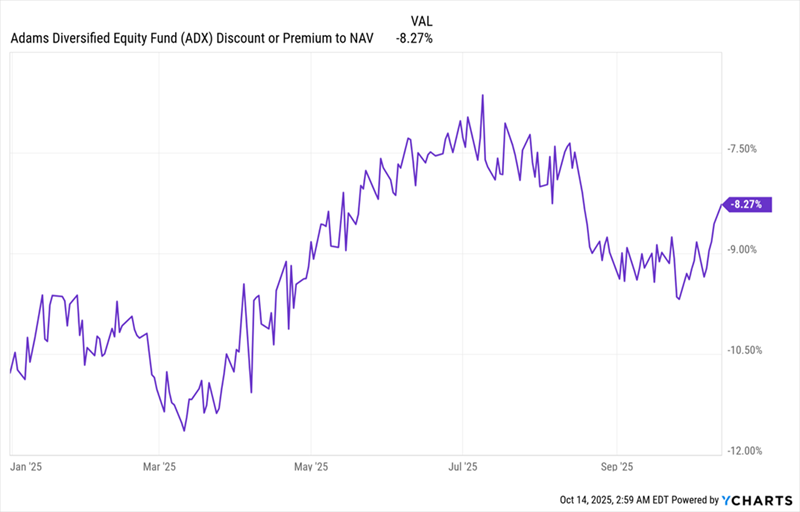

What’s more—and this is the key part—ADX trades at an 8.3% discount to NAV as I write this, and that discount is in the sweet spot, cheaper than it was a few months ago but carrying momentum as it steams toward par.

ADX Is a Rare Bargain in a Pricey Market

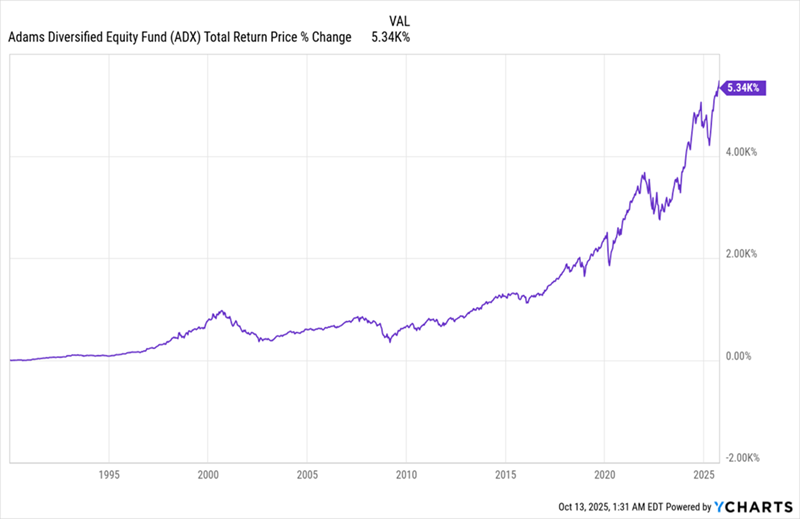

ADX has been paying dividends since before the Great Depression, and its 8.3% dividend yield is fully covered by the 13.3% total NAV return (or the return on its underlying portfolio) it’s enjoyed over the last decade. Moreover, ADX has delivered a 5,340% return to its shareholders, with dividends reinvested, since the late 1980s, when US household wealth just started to meaningfully tick higher.

ADX’s Long-Term Gains

That kind of performance—coming our way at a discount and with an 8.3% dividend—is exactly what we want from our “mini-pension,” and ADX delivers.

But, as I said, we do have choices here. And ADX isn’t the only US-stock-focused CEF that delivers a large income stream and has withstood the test of time.

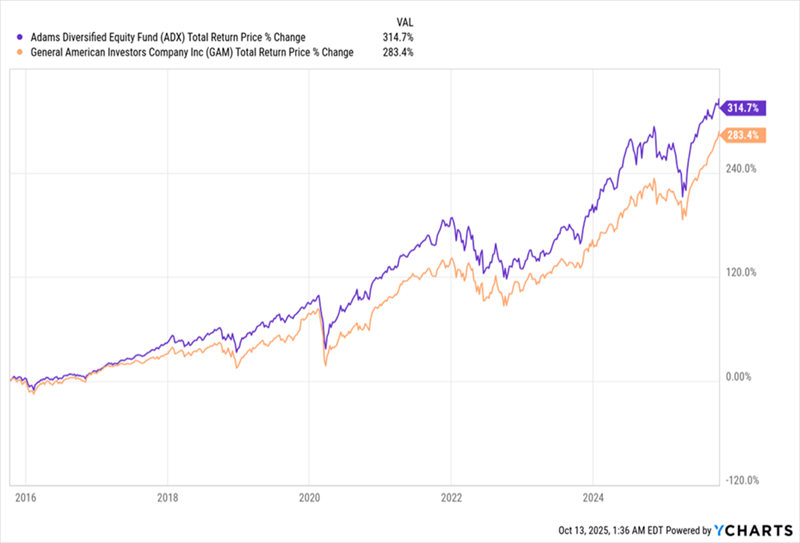

Another is the General American Investors Company (GAM), which was launched in 1927 and yielded an impressive 9.4% to investors in 2024. GAM also holds large caps, with Alphabet (GOOGL), Berkshire Hathaway (BRK.A) and Apple (AAPL) among its top holdings.

And, like ADX, this fund’s market price–based return has been strong over the last decade—though not quite as strong as ADX—with a 14.4% annualized return.

2 Strong Funds, But ADX Has an Edge

Moreover, GAM’s 9.3% discount sounds like a good deal, but that’s near its smallest-ever level, so we’re not rushing out to buy the fund today. But it is worth watching, and gets tempting when that discount drops to double digits.

But the larger point remains: With high-yielding CEFs like these, we can start generating a meaningful income stream we can choose to use however we like.

5 More “Mini-Pension” Funds Dropping 10.2% Dividends (Paid Monthly)

The beauty of CEFs is that you actually can have it all with these assets: huge dividends, market-beating performance and a deep discount, too!

Plus we get another big advantage over investors who stick with “plain vanilla” stocks and ETFs: dividends that come our way monthly!

I’ve pulled together my 5 top monthly paying funds into a “mini-portfolio” that, yes, acts just like a pension of our own, paying us every single month, right in line with our bills.

What’s more, these 5 rich monthly payers are cheap now—so much so that I’ve got them pegged for 20%+ price gains as their discounts disappear.

Don’t miss your chance to buy them now, while these deals are still available.