Ignore the doom-and-gloom “predictions” about 2026. There are plenty of gains—and growing dividends—to be had for us this year.

And if we do see a short-term pullback—possible, as we discussed a few weeks ago—the “smart money” is already setting up for a rebound. We’re going to join them by targeting three “depressed” corners of the market. We’ll get into those (and three tickers) below.

DC Stacks the Deck

Why am I so optimistic? Because, to be frank, the fix is in.

We are entering a year of “administered growth.” The Trump team has made its wishes clear: It wants lower mortgage rates, cheaper borrowing costs and a laissez-faire backdrop for American businesses.

And no matter who takes over at the Fed when Jay Powell leaves in May, they’re certain to push for lower rates out of the gate—in line with the administration’s stated (and stated, and stated) wishes.

Plus, midterm elections! We all know the administration wants a strong economy heading into the midterms. There will be money pumped into the economy this year.

In the meantime, growth remains robust, with the Atlanta Fed’s GDPNow measure giving an initial reading of 3% for Q4. That’s solid—and economists see S&P forecasts popping 15.5% next year. It’s tough to get a recession when bottom lines fatten like that.

… But We Still Need to Be Picky

That said, this is still a stock-picker’s market, and we contrarians will still do what we always do: Go where everyone else is not.

Buy an S&P 500 index fund now and you’ll lock a third of your investment in the Magnificent 7: Apple (AAPL), Amazon.com (AMZN), Alphabet (GOOGL), Meta Platforms (META), Microsoft (MSFT), NVIDIA (NVDA) and Tesla (TSLA).

I’m an AI bull. But I see the biggest gains flowing to the insurance, pharma, agriculture and other firms using the tech—less so the providers themselves.

I think other investors will see things this way, too, and they’ll rotate into other corners of the market as they do. These three tickers are a great way to “front run” them.

Consumer Spending Is Soaring. Mastercard Is Here for It

Consumers are still spending, though higher income earners are driving most of those gains, while lower-income folks cut back.

No matter how we feel about that, with productivity (and corporate profits) surging thanks to AI, consumers will likely keep tapping their cards in 2026.

That’s great for Mastercard (MA), which, along with Visa (V), essentially holds a duopoly on transaction processing. Every time a card (or phone, or mouse) is used to make a purchase, this duo gets a piece of the action.

Yes, Mastercard’s 0.6% current yield is uninspiring. But dividend growth is where the party’s at. Over the last five years, MA has essentially doubled its payout, and the share price has followed along—the “Dividend Magnet” effect we’ve talked about before. And now we have a gap between the two to take advantage of.

Dividend Doubles—Share Price Primed to Follow

Management knows this stock is strong: They’re hiking the divvie at an accelerating clip, with the last hike coming in at a rich 14%. And they’ve got a free hand to add more payout fuel to the fire, with a mere 17% of free cash flow going to dividends.

At that rate, investors don’t have to worry about a recession. Mastercard can keep the payout popping through any storm!

That payout resilience gets a boost from buybacks: Over the last decade, management has taken 10% of Mastercard’s shares off the market, leaving fewer on which it has to pay out—and setting the stage for even stronger per-share payout growth down the road.

A Low-Risk Play as AI Supercharges Medical Research

Healthcare is one place where we can clearly say there’s no AI bubble. Which is funny, because it’s where the tech can drive the biggest gains, as it slashes the amount of time needed to develop new drugs and medical devices.

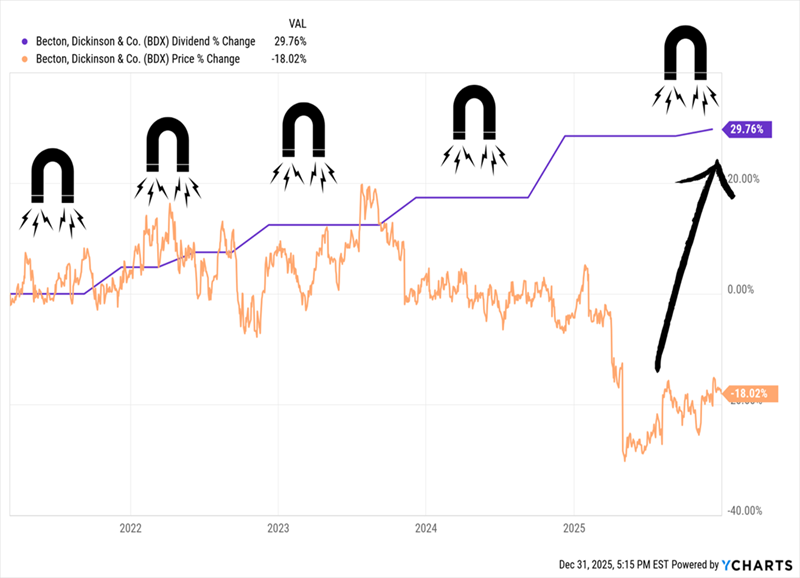

Enter Becton, Dickinson & Co. (BDX), which yields 2.2% and makes hospital mainstays like syringes, catheters and blood-flow monitors.

Our opening? BDX’s Dividend Magnet, which had been working well until a disappointing earnings report in May. That pulled down the stock and gave BDX a “dividend gap” I see as an opportunity.

Another “Dividend Gap” for Us to Play

Meantime, I see dividend growth accelerating, for a couple reasons.

First, demand for BDX’s products will naturally float higher as the population ages. Further growth comes from its Life Sciences division, maker of products every lab needs, like flow cytometers, used to analyze immune cells, cancer cells and biomarkers.

Then there’s the upcoming merger of its bioscience and diagnostics businesses with Waters Corp. (WAT). Management sees the deal teeing up 5% to 7% yearly growth for Waters, and here’s the real upside for BDX: Its shareholders will own 39.2% of the combined firm, letting it book a slice of those profits passively. Management can then focus on BDX’s remaining products.

The kicker: BDX also gets $4 billion in cash, half of which will go to buybacks, with the rest paying down debt. As with Mastercard, this opens the door to higher future payout hikes.

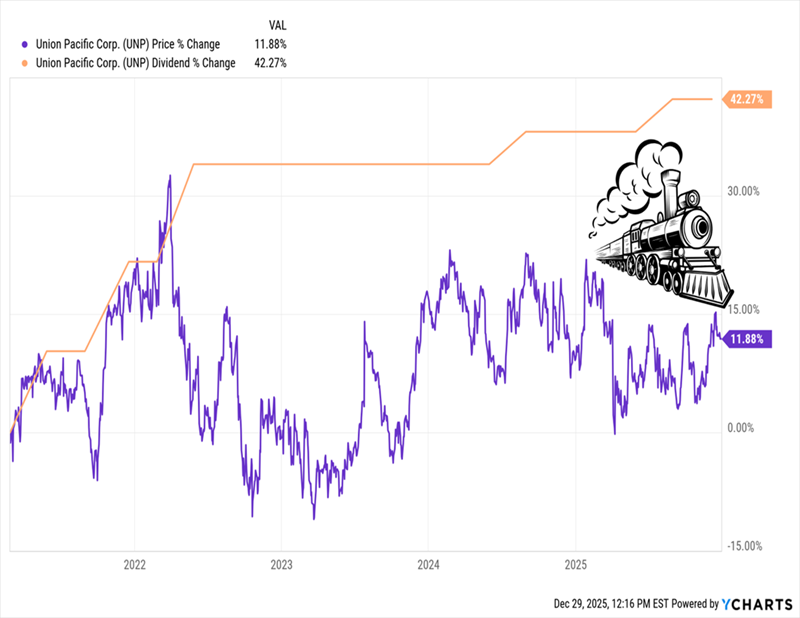

UNP Is About to Leave the Station

Trump’s tariffs hammered shippers in 2025, including railroads. Union Pacific (UNP), whose lines spread across the west and into Mexico, felt the heat. Now the company aims to capture more US business through its merger with eastern-focused Norfolk Southern (NSC).

Regulatory approval is far from certain, but either way, the “trade” winds are about to swing behind railways, and UNP’s soft stock price—which moved sideways in 2025—makes it a contrarian standout.

For one, the administration is being hammered on affordability, and it’s responded by cutting tariffs on over 200 food items. That’s a big “tell” that if inflation doesn’t let up, more tariff cuts are likely.

Then there’s the USMCA, which is up for renegotiation this year. In hearings held so far, US businesses have clearly said they want the deal to stay. And it’s always a safe bet that business—especially American big business—will eventually get what it wants.

Meantime, UNP is performing well, with EPS up 7% year-over-year in Q3. Management has also boosted efficiency, cutting UNP’s operating ratio (operating expense divided by operating revenue, the lower the better) by 1.8 points, to an adjusted 58.5%. That’s a solid result, with most Class I railroads in the 60% to 65% range.

UNP’s dividend growth has slowed recently (though it’s still up nicely in the last five years). The stock, too, has fallen off the pace. But I see that changing as trade worries wane and the NSC merger becomes clearer.

UNP’s Dividend Leaves the Station—Its Share Price Runs Late

That lag makes now a good time for a contrarian pickup—before unloved sectors like railways start to look very appealing to mainstream investors shifting out of tech.

5 Urgent Buys Set to Gain 15% Yearly Forever (Tickers Revealed Below)

Buying stout, but unloved, payers like this trio is absolutely vital to building lasting wealth.

Then we simply hold them and collect their rising dividends, which pull their share prices up over time. Boom, bust, it doesn’t matter. As the dividend rises, so too does the share price over the long haul.

Sometimes investing really is this simple!

These 3 stocks dividend histories and bargain valuations are why they’re on my watch list now. But not quite on my buy list just yet.

Topping that are 5 other stocks even deeper in the bargain bin. But I’ve got all 5 pegged to gain in 2026 (yes, with an assist from AI-driven productivity boost!).

Taken together, I see these 5 stocks delivering 15% annualized yearly returns over the long run.

That’s enough to double your investment every 5 years!

And now, while all 5 are at a low ebb, is the perfect time to buy. Click here and I’ll walk you through these 5 robust dividend growers and give you a free Special Report revealing their names and tickers.