Beware of Wall Street “wisdom” now more than ever. Especially when it comes to the most commonly quoted maxim for retirement: it’s based on a rule that was never designed for times like these!

I’m talking about the so-called “4% rule,” which says you should sell 4% of your nest egg every year in retirement.

Sounds simple, right?

Trouble is, it slashes your income stream and caps your upside in one go! It’s especially dangerous advice to follow in a downturn like the one that’s hit us in the last few months.

Let’s say, for example, you own $200,000 worth of Cisco Systems (CSCO) shares. The company is one of the most reliable dividend payers in the tech space, hiking its payout for years and continuously growing it (though not spectacularly: Cisco’s annual hikes usually only come in at just one or two cents a share).

Your holding would pay $1.52 per share in dividends on an annualized basis, for a 2.8% yield, based on today’s share price. Let’s also say you were slated to sell 4% of your holding—or $8,000 worth—on December 29, 2021, just before year end, when the stock hit an all-time high of $63.53. To get your $8K back then, you’d have had to sell 126 shares.

With 126 shares gone from your account, your yearly dividend income drops by $192. Plus, you’ve got 126 fewer shares to appreciate in the future. It’s the worst of both worlds!

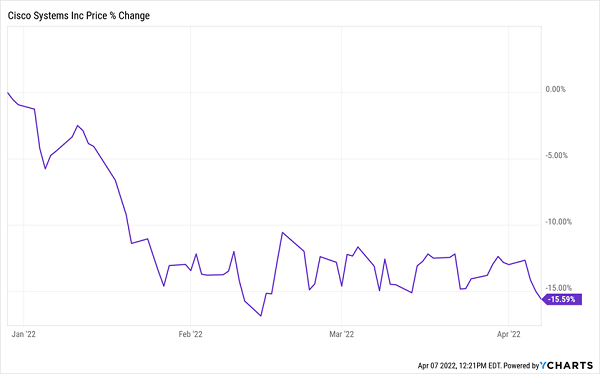

That’s bad enough, but it gets worse when these sells fall in the depths of a pullback. Imagine what would happen if you had to sell on April 5, 2022, just a few days ago:

The Worst Kind of Market Timing

Cisco’s dividend is still fine, but the stock cratered 15% from its December 29 high. So now you’d now have to unload more shares (149, to be exact) to get your $8K.

That puts an even harder cap on your future gains and slices your yearly income even more: by $226. Get hit by a few pullbacks like that and you’re well on your way to running out of money in retirement!

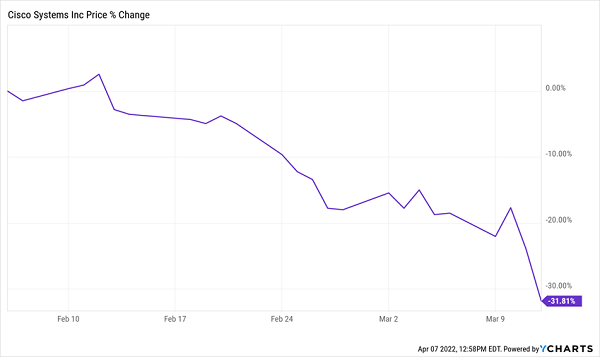

And you and I both know that crashes like these are far from uncommon. Take a look at the header Cisco took in just two weeks during the March 2020 crash:

You Do Not Want to Be Caught Selling Into This

Your Return: From Sketchy to Serene

Luckily, there’s a better way than Wall Street’s flawed 4% approach. It involves moving more of our return away from wild stock charts like Cisco’s and toward a huge cash stream that holds up through a crisis.

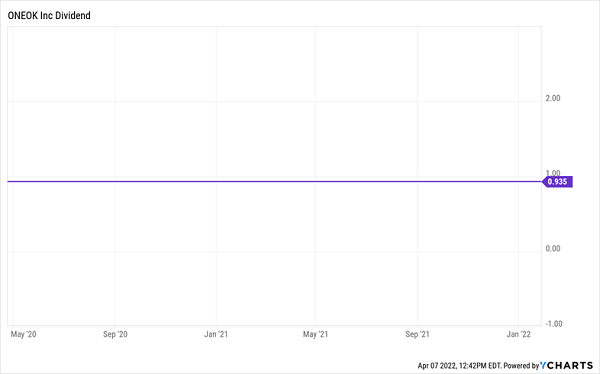

Swap This Wild Ride …

… For a Smooth Cash Stream Like This

That smooth payout stream is what members of my Contrarian Income Report service have collected since we bought pipeline operator ONEOK (OKE) in April of 2020, right in the middle of the COVID collapse.

That was no easy feat from an emotional perspective, but investors who went with their gut and took the plunge locked in an 11.8% dividend at the time (because dividend yields rise as share prices fall, and OKE was a bargain thanks to overblown fears of a pandemic-driven depression).

With a yield like that, you can forget about the 4% rule! On a $200K stake, your dividends would amount to $23,600 a year. That’s nearly 12% in dividends coming into your portfolio annually, which you can use to pay your bills or reinvest, perhaps through a dividend reinvestment plan (DRIP).

That’s a particularly savvy move because buying a fixed amount through a DRIP lets you buy more shares when they’re cheap (like during a crash, for example) and fewer when they’re pricey.

Think about that for a second: it’s the reverse of the flawed 4% rule—and it’s a proven way to build wealth over the long haul.

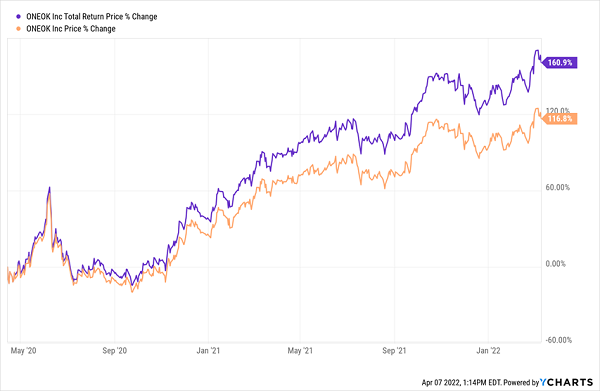

And we haven’t even talked about price gains yet: CIR members who bought on my recommendation did quite well indeed, whether they DRIPed in following their initial buy or not: the stock has soared 117% since our buy call, for a 161% total return, including dividends!

OKE’s Price—and Total Return—Soar

That gain has whittled OKE’s dividend yield down to a still-decent 5.3%, and with the oil shortage showing no signs of abating, its payout looks solid.

Buy Alert: My Best Dividend Picks Yield 7% (and Pay Monthly!)

Look, I’m not going to tell you that ONEOK is the kind of stock we hold for the long haul.

Because the old adage still applies: “the cure for high prices is high prices.” When oil supply and demand (inevitably) meet, it will be time to bid adieu to our OKE’s 11.8% “dividend pipeline” and move on to our next megatrend-driven high yielder.

While we wait for that time to come, we’re going to keep collecting OKE’s massive payout—and add to our income stream with my “7% Monthly Payer Portfolio.” As the name says, the stocks and funds inside yield 7%, on average, with some paying much more.

Also as the name says, these payouts come your way monthly, nicely lining up with your bills. Or if you’re reinvesting your payout, monthly dividends let you do so faster than regular quarterly payouts—building your upside potential (and income stream!) as you do.