AI is in and energy is out. As usual. Which is just dandy for contrarian dividend investors like us.

Let’s talk about dividends up to 6.6% and stock prices that are dirt cheap. How cheap? Stocks trading for as little as half their sales!

The best time to buy energy is before the next supply shortage. I was just “upwind” of Hurricane Hone on the Big Island of Hawaii—‘tis the season for storms. Plus we have a volatile Middle East. And an economy that may get a bit of juice as the Federal Reserve begins to ease.

The 2020s, make no mistake, are a bullish decade for energy. We are only in the middle innings of a “Crash ‘n Rally” cycle, which goes like this:

- Demand for oil evaporates because of a recession. Oil prices crash as a result.

- Energy producers scramble to cut costs, which means aggressively cutting production.

- The economy slowly recovers. Energy demand picks up.

- Because supply fell off a cliff, the price of oil climbs and climbs and climbs.

- Energy producers eventually bring supply back online. But this is a long process. It takes time to explore and drill. Supply can lag demand for years. Prices keep rising in the meantime.

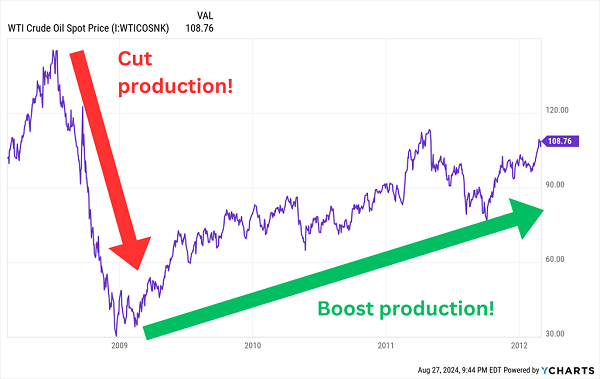

A memorable instance of this scenario started to unfold in 2008. Late that year, oil collapsed (as did virtually every other asset). “Texas tea” went from trading at over $100 per barrel to plunging below $40 within months, only to rebound back above the $100 mark within a few years.

The 2008-2012 Crash-‘n’-Rally

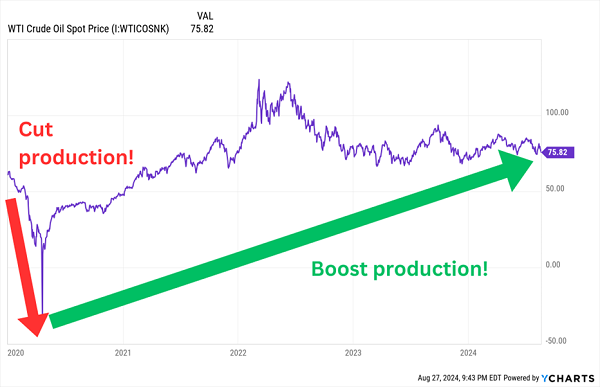

We’re now well into the most recent crash ‘n’ rally—a pattern that obviously started with oil’s pandemic-fueled descent into negative territory.

The 2020-24 Crash-‘n’-Rally

The current pattern might be a little long in the tooth, but that doesn’t mean it’s not long for this world.

Prices for West Texas Intermediate currently sit around $75 per barrel; U.S. Energy Information Administration estimates for Q1 2025 are for $84 per barrel, and that’s after a recent downgrade to expectations. World consumption of oil and liquid fuels should continue to grow, too, the EIA says.

In addition to several geopolitical conflicts, oil could enjoy several short-term tailwinds, including slower growth in electric vehicle sales and the U.S. replenishing its strategic petroleum reserve.

That rising tide could lift all boats, but if we want to maximize our yield, we want to target ships on the other side of the Atlantic. Foreign producers are cheaper, and they yield more than their American counterparts.

Just consider the following energy titans, which yield between 4.5% and 6.6% right now, and which trade for as cheap as half their revenues:

TotalEnergies SE (TTE)

Dividend Yield: 4.5%

I’ll start with TotalEnergies SE (TTE), a French multinational integrated oil-and-gas giant that was known as just “Total SE” until it rebranded in June 2021.

TTE deals in oil, natural gas, green gasses, biofuels, renewables and electricity primarily in Europe, North America and Africa, though it boasts operations in a total of 120 countries. And its five divisions—Exploration & Production, Integrated LNG, Integrated Power, Refining & Chemicals, and Marketing & Services—span the entire energy “stream.”

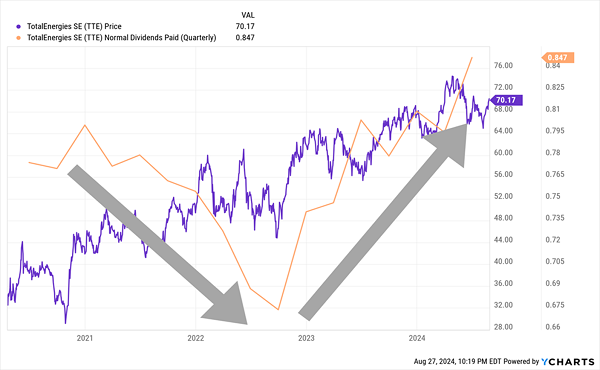

TotalEnergies has marched higher virtually uninterrupted since the COVID lows. Yet it’s still about 10 percentage points behind both the energy sector and broader market over the past five years—and it trades at a scant 8 times earnings estimates and 0.8 times sales.

The cool, calm and collected nature of TTE’s share movement is largely a reflection of a stable underlying business.

Net debt (ex-leases) has plunged from nearly $30 billion in 2020 to less than $14 billion as of the most recent quarter. And TotalEnergies is a cash-flow machine, though it certainly doesn’t need it—its pre-dividend free cash flow (FCF) breakeven point has been dropping for a decade and currently sits below $25 per barrel of oil equivalent (BOE). That’s helped by a sizable renewables portfolio that generates more than $2 billion in annual cash flow from operations (CFFO).

That’s good news for the dividend’s stability and growth prospects. TTE yields a comfortably above-average 4%, and the payout only accounts for a little more than a third of earnings.

TTE’s Dividend Is Trending in the Right Direction Again

BP Plc (BP)

Dividend Yield: 5.6%

BP plc (BP) has come a long way since it took a pummeling from COVID—and yet, at the same time, its progress hasn’t been nearly so promising.

BP is another integrated energy giant—this one, a British multinational that has done business for more than a century and currently operates in 61 countries. It produces crude oil and natural gas; deals in wind power, as well as hydrogen and carbon capture; owns thousands of miles of pipelines; has commercial operations such as convenience and retail fuel stations, Castrol lubricants and EV charging; trades oil, gas, and renewable and non-renewable power; and even has a bioenergy business.

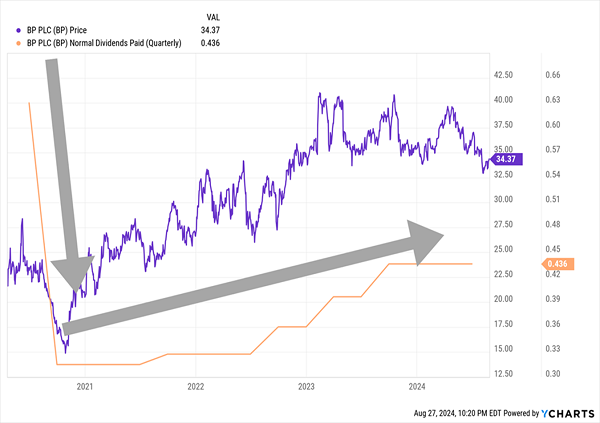

Unfortunately, BP’s massive scale and scope weren’t enough to protect it from the COVID crash in energy prices. BP shares lost more than half of their value from pandemic peak to valley, and the firm was forced to cut its dividend by 50% in 2020—a move that many (including myself) saw coming from a mile away.

BP has recovered since then; revenues doubled between 2020 and 2023, while 2020’s deep-red ink gave way to solidly green results over the past three years. The dividend has snapped back considerably—BP’s September dividend will be 10% higher than the previous payout, and more than 50% higher than after the cut. While the distribution remains well below its pre-pandemic 63 cents per share, a payout ratio of less than 50% suggests BP can continue to make amends.

BP’s Dividend Isn’t There Yet, But It’s Getting There

And recently, the company followed through on finishing off $3.5 billion in stock buybacks during the first half of 2024; it plans on repurchasing an equal amount in the back half of this year.

Yet, BP has been a relative dog among international energy giants—it’s up 17% since the start of 2020, which is a full 70 percentage points worse than the broader energy sector. Clearly, investors are holding back. BP also trades at around 8 times earnings estimates, and it’s priced at just half its trailing sales!

But they might be wary for good reason. BP isn’t flashing any severe warning signals, but the company is highly leveraged—its debt-to-capital ratio sits at 44%, dwarfing most of its energy peers. And given that BP has signaled dedication to both growing the dividend and buying back huge swaths of shares, it seems that debt payoffs are low on the totem pole.

It’s not an untenable position given current energy prices, but BP might not be the safest of shelters should catastrophe strike.

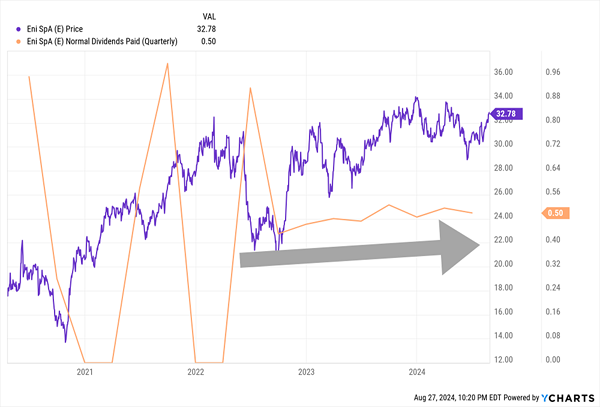

Eni S.p.A. (E)

Dividend Yield: 6.6%

The biggest payout of the group comes from Eni S.p.A. (E), an Italian integrated energy giant whose operations span E&P, manufacturing, transport, and marketing of oil, nat-gas, oil-based fuels, chemical products, and renewable energy products.

Eni sits in the middle—its recovery hasn’t been as persistent as TotalEnergies’, nor has it been as lackluster as BP’s. But it has at least managed to crack its pre-COVID prices.

It also has adopted an American-friendly dividend schedule. While it once used the interim-and-final dividend system favored by many European firms, Eni joined the quarterly club a few years ago.

That’s a Little More Like It, Eni

Perhaps more importantly, the dividend has been on the upswing since COVID—and the company plans on spending even more cash, upgrading from a distribution target of 25% to 30% of expected annual CFFO to a target of 30% to 35%. (Cash spending isn’t limited to dividends, either; earlier in Q1, Eni raised its 2024 buyback by 45%, from 1.1 billion euros to 1.6 billion euros.)

And Eni is the cheapest of the bunch, if only marginally, trading at about 7.5 times earnings estimates and roughly half of sales.

Past the metrics, whether an investor likes Eni or not largely comes down to their view on energy prices. Eni is highly exposed to E&P, meaning it’ll be the most sensitive to price swings—for better or for worse.

With a Little More Yield, You Can Retire on Just $500K

A true energy blue chip that pays us 6.6%? It’s a rare find, but if we raise the bar just a little bit more, we can put ourselves into a completely different tier of retirement planning.

I’m talking about retiring on dividends alone.

It’s not hype, it’s not hope—it’s simple math. My 9% “No Withdrawal” Retirement Portfolio aims to do what your typical blue-chips-and-basic-bonds retirement portfolio can’t: Allow you to retire on dividend and interest income alone, without ever having to touch a penny of your nest egg.

I’ll even show you my work:

If you put just $500,000 to work in a portfolio yielding 9%, you’ll earn a $45,000 “salary” of dividends from your retirement account. Now tack on your Social Security payments, and you’re looking at a much friendlier retirement budget once you call it quits at work.

And if you have an even bigger pile of cash to plug into our 9% “No Withdrawal” Retirement Portfolio? Well, even just the thought brings a smile to my face—and I bet you’re wearing one, too.

You won’t find these yields in mega-caps like the energy names above. But I can show you the stealth payout plays that Wall Street overlooks—names that do yield the 9% or more that we need to coast forever on dividends alone. Please click here and I’ll share the details on these secure funds with very generous dividends!