We’ve got a once-in-5-year buy window open to us in one of the highest-yielding investments out there.

And (for once) we can thank the Fed for these cheap 8%+ payouts!

I’m talking about closed-end funds (CEFs), a corner of the market where rich 8%+ yields (and monthly payouts) are the norm.

These (too) often-ignored funds are set to spike because the last time Powell & Co. acted like they are now, CEFs’ prices soared—and they handed their lucky investors big price gains to go along with their huge dividends.

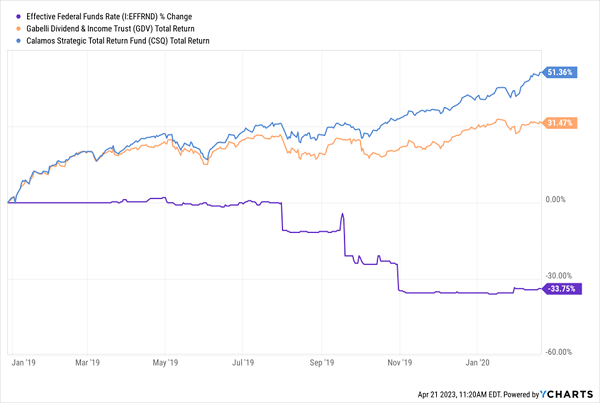

If 2023 Is 2019 Redux, CEFs Will Explode Higher

To see what I’m getting at here, think back to late 2018. The Fed had just brought in its last hike of a cycle that started in late 2015.

It then held rates steady until mid-2019, when it made three rate cuts between then and the societal dumpster fire that hit in March 2020. That’s a similar scenario to what we’ll likely see later this year, with the Fed holding rates for a while and gradually unwinding them (though not to the bottomed-out levels we saw in the pandemic).

How did CEFs do back then? Just fine! Two of the stock-focused “go-tos” in the space—the Gabelli Dividend & Income Trust (GDV) and Calamos Strategic Total Return Fund (CSQ), soared 31% and 51%, respectively:

CEFs Soar When the Fed (Gradually) Cuts

It makes sense: CEFs use leverage to bolster returns, and the resulting lower borrowing costs flow straight to their bottom lines (and to us through their rich 8%+ dividends!). Meantime, the strong economy balloons their share prices.

But buying CEFs isn’t like buying a mutual fund or ETF—truth is, there are more CEF dogs than stars out there, so we need to take a few extra steps to get the most price upside and the safest payouts.

With that in mind, let’s roll through the six steps you need to take to unlock retirement-changing income, and price upside, from your CEF buys:

Step 1: Look Beyond “Price-Only” CEF Performance Charts

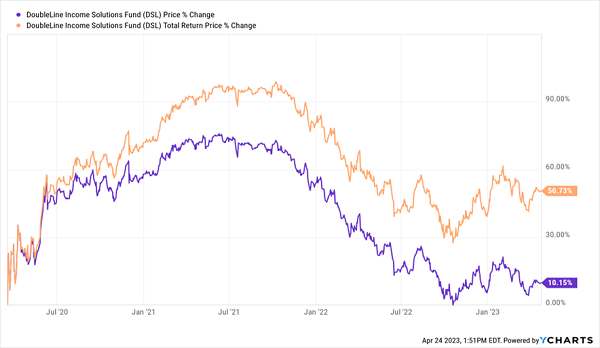

The DoubleLine Income Solutions Fund (DSL) has been a strong performer since we added it to our Contrarian Income Report portfolio in April 2016, giving us an 11% yield when we bought in—and that’s where its yield sits today: at 11.4%, to be precise.

And it’s performed well for us, beating its benchmark and delivering a 35% return during our holding period despite a tough stretch for bonds that included two rising-rate spans, from 2015 to 2018 and 2022 into 2023.

But traditional analysts have always missed the beauty of DSL and other CEFs because they only focus on price charts. But because CEFs throw off huge dividends, looking at price alone gives you at best half the picture, and sometimes much less than that!

DSL’s performance from the trough of the COVID crash in March of 2020 until today illustrates the point perfectly:

Dividends Make All the Difference to CEF Performance

As you can see above, the price action (in purple) diverts sharply lower in this time frame, which is only a bit over three years! And that gap will only grow wider the more time goes on. That’s not an indictment of CEF price performance, by the way. It simply shows that we need to look at CEFs—especially those with truly massive payouts like DSL—much differently than stocks and ETFs.

The bottom line: Take price-only CEF charts, which are the norm on screeners like Google Finance and Yahoo! Finance, with a grain of salt. Brokerage statements typically report price-only returns, too.

Step 2: Know What’s Funding Your Distributions

A closed-end fund can pay you from some combination of:

- Investment income,

- Capital gains, and/or

- Return of capital.

Of the three, investment income is preferable because it’s usually the most reliable. Many CEFs pay monthly distributions, so it’s best if they match up their payouts with steady income streams.

Capital gains from rising bond or stock prices can further boost distributions. But they are at risk of disappearing if the markets drop.

Finally, everyone assumes that return of capital is bad because it’s simply shipping your money back to you. But if the fund trades at a significant discount, this can actually be a savvy way to kick-start the closing of a discount window. More on this shortly.

Step 3: Collect Your Buy Price (and Then Some!) in CEF Dividends

In less than six years, we’ve collected 72% of our original purchase price in dividends from DSL, likely headed to 100%. And once you clear that level, everything else you pocket—in dividends and price upside—is gravy.

That’s what makes CEFs so compelling for retirement investing—when you buy the CEFs with high, steady payouts, like those we recommend in my Contrarian Income Report service, they act like an annuity, but better!

Step 4: View CEF Fees Differently Than “Bargain-Basement” ETF Fees

Most investors are conditioned to a fault by their experience with mutual funds and ETFs to search out the lowest fees. This makes sense for investment vehicles that are roughly going to perform in line with the broader market. Lowering your costs minimizes drag.

Usually, but not always. Closed-end funds are a different investment animal. On the whole, there are more dogs than gems. It’s a necessity to find a great manager with a solid track record. Great managers tend to be expensive, of course—but they’re well worth it.

The stated yields you see quoted, by the way, are always net of fees. Your account will never be debited for the fees from any fund you own. They are simply paid by the fund from its NAV. You receive the yield you see—a rare and happy case of truth in packaging!

Step 5: Demand a Discount

One aspect of the CEF structure lends itself perfectly to contrary-minded investing: a fixed pool of shares.

Mutual funds issue more shares whenever they want, fixed each day at NAV. But CEFs have a fixed share count, with their units trading like stocks. As a result, from time to time a fund will fall out of favor and find its shares trading at a discount to its NAV.

This is basically “free money” because these underlying assets are constantly marked to market (unlike mutual funds). If a CEF trades at a 10% discount, management could theoretically liquidate it and pay everyone $1.10 on the dollar. Or it can buy back its own shares to close the discount window (and boost the share price).

A discount is a great start, but do make sure that management has a plan to close that window! Sometimes the discount exists for a reason, so we dig deeper.

Step 6: When Possible, Look to Buy Alongside Insiders

It’s rare to see any fixed-income manager put his or her own money on the line at all, unfortunately. Barron’s research showed that out of 558 closed-end funds at the time of its study, nearly half (269) had no insider ownership whatsoever. And only 70 had insider ownership above $500,000.

I’ve seen no evidence that insider ownership is any higher today, which raises the question: why would we want to own any of them, if the managers have no skin in the game?

What we want is a Bradford Stone, one of the managers at the Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP), whose 26,667 shares of DFP are worth around $481,339 today.

My “Perfect Income Portfolio” Could 4X Your Dividends—Starting Now

Sure, you could spend hours poring over CEFs’ quarterly reports, scanning for these 7 telltale signs of a winner yourself. Or you could let me and my research team do it for you!

In fact, we’ve already done it.

The result is my “Perfect Income Portfolio,” which contains my very best CEFs and other high-yield plays for new buying today. I call this portfolio “perfect” because it delivers everything income investors crave, including:

- High, steady payouts that pay triple—and even 4X—the 2% or 3% most S&P 500 stocks dribble out (if they pay a dividend at all!)

- Undervalued, overlooked investments, which research shows have a far better chance of delivering big gains than the overvalued, popular names most people buy.

- Simplicity and convenience: This portfolio needs very little handholding from you, really just a few minutes a month!

I’ll also throw in a no-risk trial to my monthly Contrarian Income Report service, which delivers you new high-yielding (and often monthly paying) picks on the regular. Don’t miss out. Get access to the Perfect Income Portfolio and start your no-risk 60-day trial to Contrarian Income Report now.