Here’s something most people forget about interest rates: The Fed does not call all the shots here.

This means that, in the coming months, we may see a setup where the Fed’s rate—the “overnight” rate at which financial institutions lend to each other—and the 10-year Treasury rate (pacesetter for business and consumer loans) part company.

Today we’re going to dig into a “stealth” 5.7%-paying stock that’s a perfect contrarian play on this situation. This one pays us every month, too.

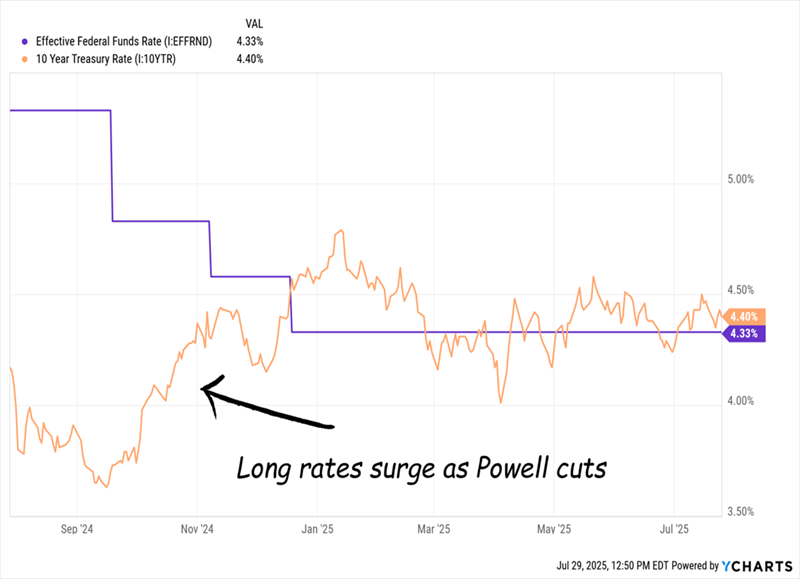

Fed Cuts … and Rates Soar!?

I say that this “rate split” is possible because, well, it’s already happened in the last few months. Let’s rewind to last September, when the Fed brought in its first rate cut since 2020, after hiking rates during the 2022 inflation spike and holding them steady since.

The bond market, however, was having none of it. Even as the Fed cut, 10-year Treasury rates soared, sending Powell a clear message: Slow your roll.

Powell Gives the “All-Clear.” Bond Market Says “Not So Fast”

When the Fed cut rates last September, it ironically sparked a serious rally in long yields. The 10-year rate soared from 3.6% to 4.8%. That’s a 33% move! Once Powell backed off, leaving the Fed’s rate where it is now, the 10-year yield leveled off, as you can also see at the right side of the above chart.

We could very well be in for a repeat of last September, and here’s why: The Atlanta Fed’s GDPNow model has the economy clipping along at a 2.9% rate as I write this. That’s solid growth. Plus we’re heading into (ugh) another election cycle, which means more stimulus is likely.

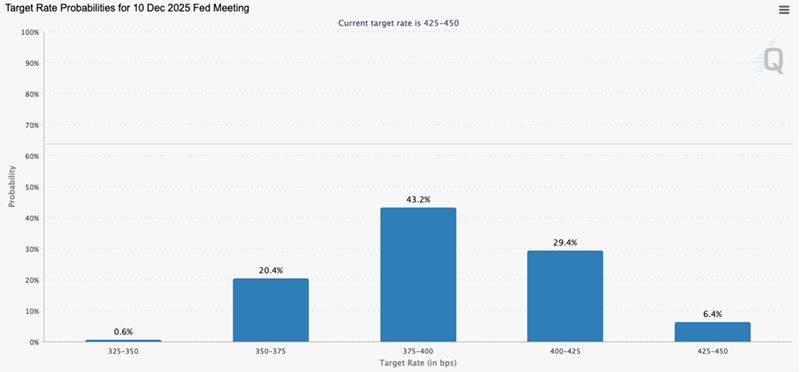

Meantime, option traders have the Fed cutting rates by at least 50 basis points by the end of the year:

Source: cmegroup.com

Remember, too (and how could we forget?) that Powell’s term ends in May, and he’s likely to be replaced by someone who will work with the administration to lower rates.

Our “Stealth” Monthly Dividend Play on a Potential “Rate Split”

Put it all together and we could easily have a setup where the Fed cuts and reignites a rally in 10-year Treasury yields, a la 2024. One stock poised to profit is a business development company (BDC) called Main Street Capital (MAIN).

Now first let me say that we’d normally be cautious around BDCs in such a rate environment. That’s because they lend money to small- and mid-sized businesses (think regional manufacturers, healthcare providers and the like), with MAIN going after firms with $25 million to $500 million in revenue.

Moreover, a large slice of their loans tend to be floating-rate, and as such tend to move with the Fed funds rate (which, as we’ve been discussing, looks set to decline from here).

But even if a rapid fall in the Fed rate were to play out (and it isn’t likely to be abrupt, as it’s not just the Fed Chair, but the entire Open Market Committee, that has a say on rate moves), it’ll likely be accompanied by still-strong economic growth.

And that means more chances for BDCs to spur new loans—with MAIN, as one of the leaders in the BDC market, likely to grab a healthy share. Moreover, while MAIN doesn’t get specific, it did note in its latest investor presentation that its floating-rate loans “generally” include minimum “floor” rates.

The firm also says that 77% of its outstanding debt obligations are fixed rate, while on the lending side, 68% of its debt investments (i.e., loans outstanding) are floating-rate. That gives the company some built-in insulation on both sides of the balance sheet.

About That 5.7% “Stealth” Yield

Then there’s the company’s dividend yield, which, if you look it up on a free stock screener, will show up at around 4.7%. But that’s the forward yield, annualized based on the latest monthly payout. And it’s likely an understatement.

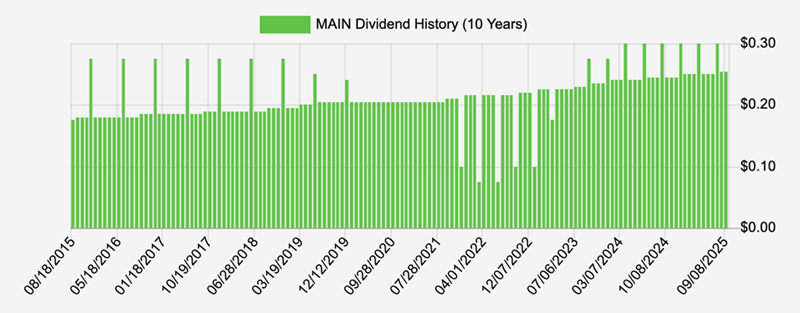

A better measure for stocks like MAIN, which issue regular special—or as the company calls them, “supplemental”—dividends, is the trailing-12-month yield. In the last 12 months, MAIN has issued three supplementals, making its trailing yield a much higher 5.7%.

Moreover, over its 18-year history, this ironclad lender has never cut or suspended its payout, even during the pandemic or financial crisis. Check out this happy payout chart:

MAIN’s Dividend Keeps Pace, Backed By a Rock-Solid Loan Portfolio

Source: Income Calendar

(And to be clear, those dips in the chart above aren’t reductions—they’re those “supplemental” payouts I just mentioned, as are the spikes.)

The BDC’s payout gets an assist from the fact that, like real estate investment trusts (REITs), BDCs must pay 90% of their income in order to be exempted from corporate taxes by the federal government.

And its portfolio is impressively diverse. Right now, MAIN holds investments across 189 companies. And its largest holding makes up just 3.2% of investment income. In fact, most investments represent less than 1%, spreading the risk nicely.

Even better, these holdings span dozens of industries, and MAIN doesn’t let any one industry dominate (none currently tops 10% of its investments). It’s exactly the kind of broad diversification that helps manage potential portfolio heartburn.

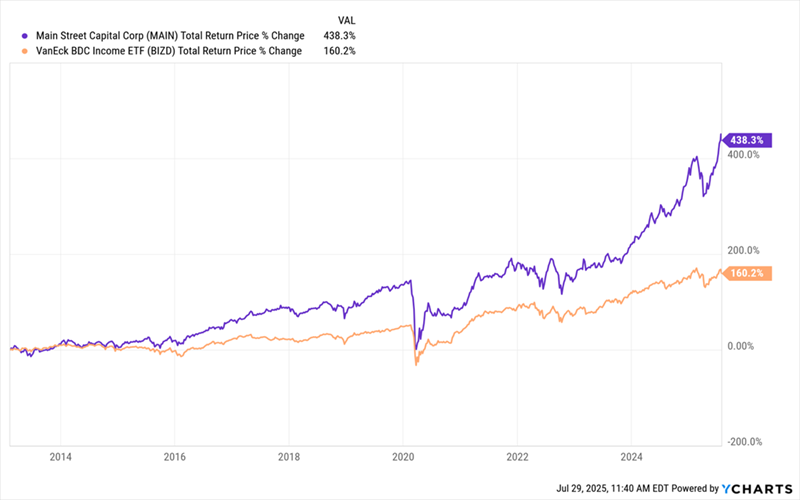

No wonder MAIN has trounced the BDC index fund since that fund’s launch in 2013:

MAIN Gives Us ETF-Style Diversification—While Crushing ETFs

We’re up 22% on MAIN since our buy in May 2025—less than three months ago! That’s good for 91% on an annualized basis. The stock is now above the buy-up-to-price I recommend in my Contrarian Income Report service. So we’re not buying more now, but we are more than happy to keep holding and collecting MAIN’s healthy payout.

If you missed our May call, you do not want to miss our next buy window. I expect that one to open when the Fed restarts rate cuts—and that could come as soon as September. When the next opportunity shows up, I’ll let Contrarian Income Report members know.

Get an Instant Buy Alert On MAIN and My Top Monthly Dividend Buys

Not only do Contrarian Income Report members get instant alerts when I change my buy/sell/hold recommendations on stocks like MAIN, but they also always have access to the service’s full portfolio of picks.

Within that portfolio, in fact, is another BDC that’s a top buy now. This one yields more than MAIN, too, with an outsized 8.5% payout. In other words, buying it now gets you a higher income stream while you wait for our next buy window on MAIN to open.

Here’s how to get the name of this top-flight 8.5% payer and instant access to the full Contrarian Income Report portfolio of high yielders:

I’ll also reveal how to get a free Special Report of my favorite monthly dividends to buy now, as well as a chance to road test Contrarian Income Report for 60 days with no obligation whatsoever.

That trial gives you instant access to the portfolio, as well as that 8.5%-paying BDC!

But there’s no time to wait. This opportunity could vanish as the rate path shifts again. Click here to get VIP access to this complete wealth-building package now.