Do not miss these huge dividend yields we’re seeing today. In a year or two, you’re going to kick yourself for not locking these income streams in.

Take it from me. This bond guy nearly missed the great home refi opportunity of 2020-21. Fortunately, I managed to wake up and lock in a 2%+ mortgage before rates skyrocketed. Today, 30-year mortgage rates sit at 8%. Eight percent!

I mention that only because we have a similar setup in dividends today. In a moment, we’re going to discuss an elite dividend paying 8.5%. Let’s not miss it!

From Mortgage Refis to “Dividend Refis”

Here’s the upshot: the same trend that delivered that sweet refi opportunity three years ago is driving our dividend opportunity today—just in reverse.

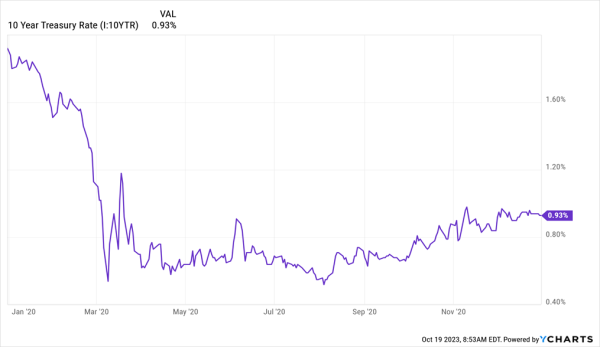

I know nobody wants to talk about 2020, with its lockdowns and backyard bars, but bear with me for a sec. In those days, to put it mildly, the economy was flat on its back. The Fed was pumping out printed cash, and the yield on the 10-year Treasury bottomed out around 0.5%.

10-Year Yield’s Historic COVID Crash

That decimated mortgage rates and sent dividend stocks through the roof, dropping their dividend yields in turn (because yields and prices move in opposite directions).

It all made sense—if you wanted yield, stocks were the only game in town!

Today, the script has flipped. Treasury rates just broke over 5%— drawing investors away from dividend stocks … and sending the yields on our favorite tickers soaring.

But that won’t last.

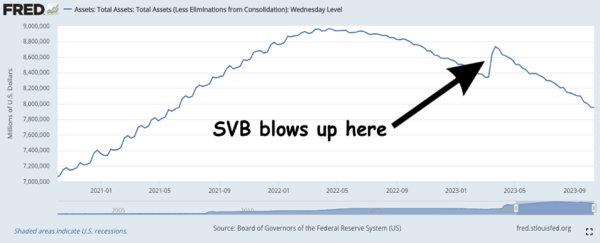

You and I both know this economy is slowing down. Powell almost broke the banks back in March, and he’s not going to risk another crisis. Just look at how quickly he changed course when Silicon Valley Bank, Signature Bank et. al. cracked:

What we’re looking at here is the Fed’s balance sheet—you can see how it started letting its bond holdings “roll off” as they matured, starting in mid-2022—so-called “quantitative tightening” in action.

That spike in early 2023? That’s when the Fed got spooked and temporarily reversed course, suddenly adding to its bond holdings out of fear of breaking the banks.

The Fed said little about this at the time. But it’s proof positive that as the economy slows, Powell & Co. will be quick to can their tough talk and cut rates. And the 10-year, which is much more dialed to investor moods than the Fed, will likely head lower before that.

And that will trigger a flood of folks out of treasuries and back into dividend stocks. The time to “front run” them is now, so we lock in today’s high yields for the long haul. But what do we buy?

Add an “X” to This Ticker for a Deep-Discounted 7.7% Dividend

When looking for investments that will soar out of a downturn, it pays to look for the ones that were pounded the hardest in the crash. These “garbage pail moments” are gifts to savvy contrarians like us, and right now we’re looking squarely at tech, which took a header in ’22. It’s rebounded this year, but the tech-heavy NASDAQ still sits about 8% below its peak.

For tech exposure, first-level investors often look to the Invesco QQQ Trust (QQQ), an ETF that tracks the NASDAQ, so it’s no surprise that the main holdings are companies like Apple (AAPL), Microsoft (MSFT) and Amazon.com (AMZN).

Trouble is, QQQ is a pathetic payer, yielding just 0.6%. But if you go one step further and add an “X” to that ticker, you get a closed-end fund (CEF) called the Nuveen NASDAQ Dynamic Overwrite Fund (QQQX). This one holds all the same stocks but with a twist—two, actually:

- A 7.7% yield, which it generates from income from its portfolio and a savvy covered-call strategy that delivers extra cash, and …

- A big discount to net asset value (NAV), which, at 6.6%, is lower than it’s been at any point since late 2020—and far below the fund’s five-year average of a 0.6% premium.

One drawback of selling covered calls is that it can weigh on returns over the long haul, as the fund’s best performers rise to the option-selling price and get sold, or “called away.” But pushing against that is QQQX’s far below-average discount. Plus, the fund’s price would get an assist from a declining Treasury yield, too.

The kicker? If we get more volatility in the near term, this dividend gets safer, thanks to that same covered-call strategy, as QQQX’s options are likely to expire worthless, letting the fund keep its holdings and the fee, or “premium,” it sells option buyers, too.

An 8.5%-Yielder With More “10-Year-Powered” Upside

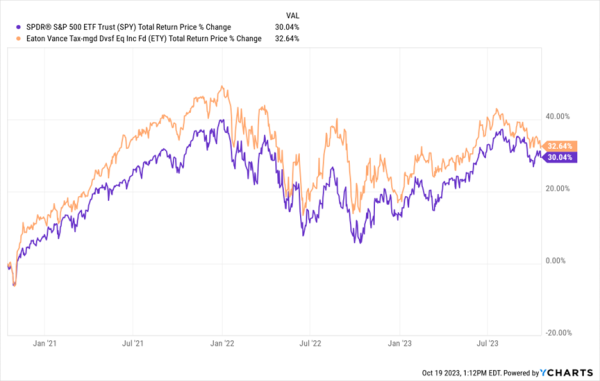

Next, consider “swapping out” your S&P 500 index fund for another deep-discounted CEF, the Eaton Vance Tax-Managed Diversified Equity Income Fund (ETY). The name is a mouthful, for sure, but it’s worth our time due to its higher payout—a sweet 8.5%—and the fact that it pays dividends monthly.

ETY is a standout because it gives us the best of both the ETF and CEF worlds: it’s actually outrun the ETF over the last three years, but it’s done so mainly by delivering its return in dividend cash, as it’s a high-yielding CEF.

ETY Outruns Stocks With an 8.5% Dividend (Paid Monthly)

Management pulls this off by selling covered-call options on part of the portfolio, similar to QQQX, while zeroing in on “growthier” stocks like Microsoft and Apple, as well as Meta Platforms (META), MasterCard (MA) and Alphabet (GOOGL). In other words, the same stocks set to benefit from a decline in the 10-year yield.

Finally, this one trades at a 5.5% discount, just above its 52-week low of 5.9% and far below its five-year average of 0.8%. So we can expect extra upside as that discount flips back to normal, propelling ETY’s price higher as it does.

Life-Changing Portfolio Lets You Live on Dividends Alone—Potentially Forever

Make no mistake: “locking down” big payouts at times like these is the key to building lasting wealth—and sending your retirement income soaring. Because when you’ve got 8%+ dividend payouts rolling in, you have less of a need to sell stocks to generate income—boosting your chances of living on dividends alone!

Shifting your return from shaky stock prices to the steady drip of dividends really is the “holy grail” of investing. And I want to show you a portfolio that does exactly that, potentially setting you up to live off a $500,000 nest egg, practically forever.