The hardest part of convincing folks they can lock in high dividends for the long haul (I’m talking 9%+ yields here) is that many just don’t believe it.

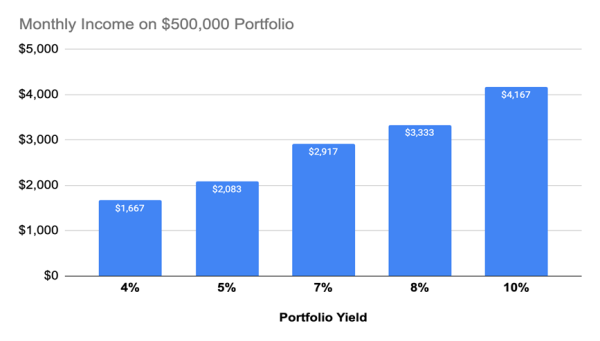

And frankly, I can’t blame them. Too many people are paid a lot of money to tell investors that yields like that are impossible. But the truth is you can get a 9.5% yield today—and even more. But even at 9.5%, we’re talking about a middle-class income of $4,000 per month on an investment of just a touch over $500K.

Source: CEF Insider

Below, I’ll reveal how to start building a portfolio that could get you an even bigger income stream than this today. But before that, I want to show you the three funds I suggested buying to do this over six years ago and look at how they’ve performed since. It’s a good way to demonstrate how a high-income portfolio can deliver the goods for many years, despite what the naysayers say.

The Pre-Pandemic 9.5% Portfolio

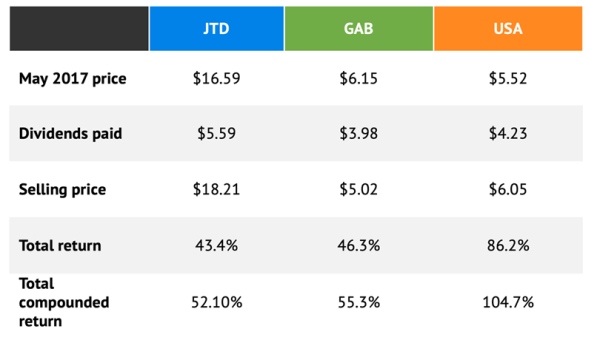

In a 2017 Contrarian Outlook article, I suggested a portfolio of three closed-end funds (CEFs) yielding an average 8.2% between them: the Nuveen Tax-Advantaged Dividend Growth Fund (JTD), Gabelli Equity Trust (GAB) and Liberty All-Star Equity Fund (USA). This “mini-portfolio” was designed to do three things:

- Provide lower-volatility returns, thanks to broad diversification across high-cash-flow companies (JTD), deep-value companies (GAB) and large-cap value and growth firms (USA).

- Offer a higher income stream than index funds (paying at the time, as now, less than 2% yields).

- Offer opportunities to rebalance when fund discounts shrank too much.

How did it go? Let’s take a look:

Source: Ycharts, SEC.gov, Nuveen Asset Management

(Total return calculates if all dividends are taken simply as cash; total compounded return calculates if all dividends are reinvested into the same fund.)

Investing in this portfolio in May 2017 yielded a 70.7% return in total. Not bad! Plus, our three-fund portfolio’s 8.2% yield brought in regular cash we could use elsewhere as we liked. That’s a key advantage over investing in lower-yielding index funds, which would entail selling—and trying to time the market in doing so—to generate extra cash.

One note on the table above: the sell dates occur as of this writing (October 16), while I’ve placed JTD’s sell date in November 2021, when investors had the option to sell all their shares or trade them for shares in a new fund: the debt-and-stock-focused Nuveen Multi-Asset Income Fund (NMAI). Because NMAI’s strategy is very different from JTD’s equity focus, we’re assuming investors sold JTD instead of trading their shares in for those of the new fund.

It is clear by this quick look in the past that, indeed, CEFs can fund a retirement for years. But what about dividend cuts?

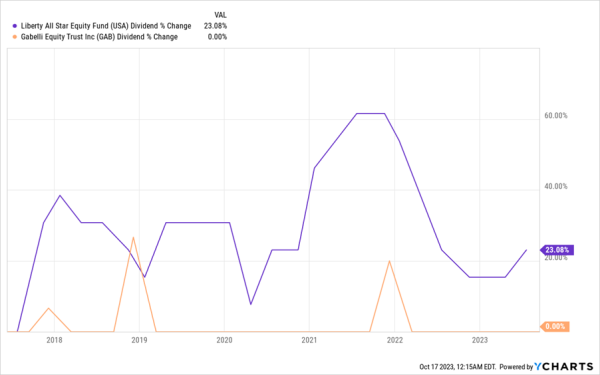

No Cuts Here

While GAB, in orange above, kept its dividend steady (and paid out some nice special payouts along the way, as shown by the three spikes), USA, in purple, hiked its payout overall (note that USA pays out a percentage of net asset value—NAV, or the value of its underlying portfolio—which is why its payout floats a bit).

JTD, admittedly, did cut its dividend by 5% from May 2017 until its merger with NMAI, but the fund still paid 7.5% on average during this period and the overall portfolio’s dividend yield didn’t just cover the 8.2% I initially promised. It offered more.

Combined with GAB’s and USA’s 11% payouts on average (including special dividends), the portfolio ended up yielding 9.5% for years.

Replicating That 9.5% Payout Today

Could you use GAB, USA and NMAI to replicate the same portfolio today?

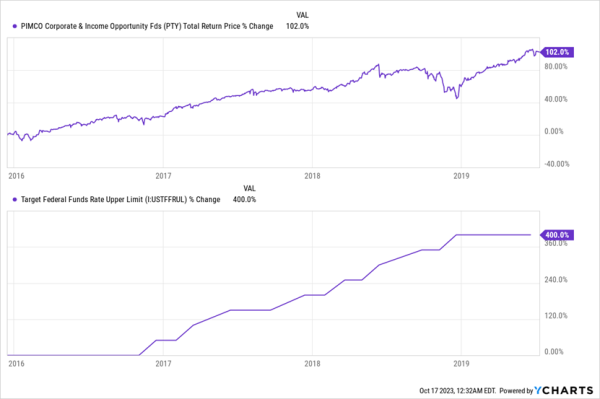

While you could, it’d be very different, both because NMAI isn’t the same as JTD and because markets have changed a lot. In 2017, it was easy to be bullish on stocks, and while I still am, the really big yields available in bonds might mean that a diversified portfolio of bond funds, like the PIMCO Corporate & Income Opportunity Fund (PTY), could be a compelling alternative.

PTY is an 11.5%-yielder that brings retirement even closer (a $4,000-a-month income stream would entail a $417,391.13 investment). And with corporate bonds now yielding over 8% and mortgage rates at 8%, a fund like this, which buys corporate bonds and mortgages from banks, could provide even bigger returns than stocks if rates stay high. Last time we saw rates rise, PTY soared, too—and it kept its gains as rates stayed high.

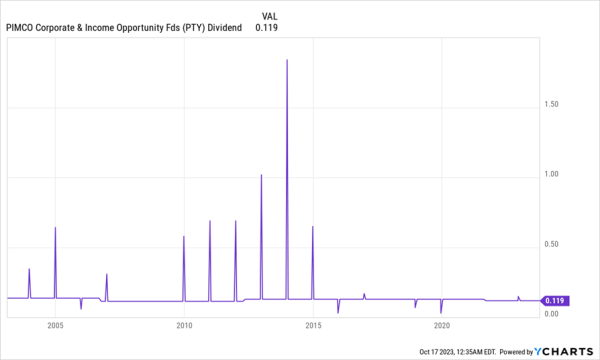

PTY Loves Higher Interest Rates

Worried about longevity? Six years is nothing. PTY has not only paid out dividends close to its current rate (dividends have fallen less than two whole pennies over the last 30 years), but it has also paid out big special dividends—shown in the spikes and dips below—that have brought its annualized yield upwards of 15% at times:

Long-Term Reliable Payouts and Big Special Dividends, Too

Those big payouts were due to uncertainty in markets in the early 2010s that PIMCO exploited. I suspect the next generation of bond uncertainty is something PIMCO will easily exploit, too, since the firm quite literally invented the concept of bond trading back in the 1970s.

Finally, let’s talk valuation, because even a cursory analysis of the fund will tell you that it trades at a 20% premium to net asset value (NAV, or the value of its underlying portfolio) today. But with CEF premiums and discounts, we always need to look at historical context, too.

And the truth is, PIMCO funds almost always trade at premiums—and often much larger ones than this, because of the firm’s deep expertise in bond-land. And you could say PTY is undervalued, as its five-year average premium is even higher, at just under 24%.

5 More CEFs That Pave the Way to Financial Independence (With 10.5% Yields)

Unlike PTY, my top CEFs to buy now trade at deep—and totally unusual—discounts, and pay huge 10.2% dividends, too!

These are the kinds of discounts and yields that can deliver true financial independence. Which is why I urge you to act now—before these absurd discounts close and this opportunity races away from us.