The Internet is a wild place—and finally, we have irrefutable evidence! I mean, why else would investors dump this safe 12.8% dividend?

Hilariously, they are already feeling FOMO. After selling this stock low, it jumped 7.7% without them last Friday alone. Wow.

A basement blogger decided to pick on Arbor Realty Trust (ABR) in recent weeks. No name, no face, but hey, they whipped up a nifty little PDF saying they were short ABR, so we all should be too.

(Note: We don’t hate short sellers. In a world where every first-level investor wants to hear only the good news—true or not!—thoughtful, analytical, and careful short sellers provide a much-needed service. The catch here? Not one of those terms applies to our basement blogger.)

Others have already boarded this short bus. ABR has its swath of nonbelievers, with 29% of its outstanding shares sold short. Which tells us two things.

- There are others—perhaps more basement bloggers—who doubt this dividend.

- They are paying through the nose to short the stock. Even if the bloggers themselves are broke (they usually are), someone is paying 12.8% per year for the right to bet on an ABR decline.

Remember, short sellers are borrowing shares to sell now, hoping to buy them back (“cover”) later, at a lower price. Which is fine, except when we’re borrowing a dividend stock, we’re on the hook for the payout. Which, in ABR’s case, is 12.8%. (Plus the cost of the margin loan required for shorting!)

But Brett, you’re probably thinking, how can this many people be wrong about a stock?

Well, first, it happens all of the time. Investing herds behave like, well, herds. They follow each other without thinking.

Which feels safe but becomes dangerous as groupthink devolves into a short squeeze. As in oops we were wrong, we all need to cover (buy back our shares) at once.

The race to the exits sends the stock higher thanks to panic buying. Which is a thing too. (Remember GameStop?)

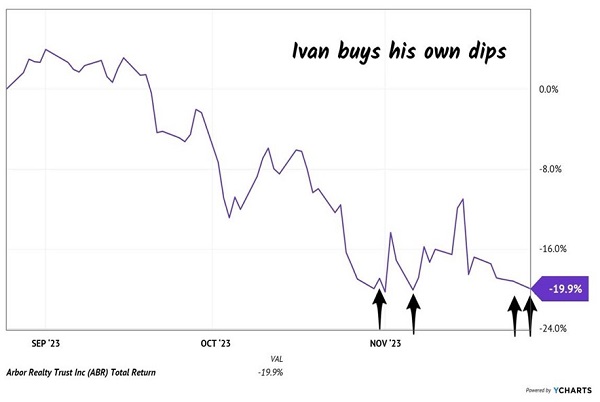

A potential catalyst for this upcoming purchase panic? How about big insider buying from the big boss himself! I’m talking about the company’s own Founder CEO doubling down after the dip.

But actually Arbor’s boss Ivan Kaufman isn’t just doubling down. He’s hit four times over the past two months, adding a cool $1,550,757.67 to his personal ABR position:

Arbor CEO Buys the Dip 4X

This brings Kaufman’s personal stake in ABR shares to nearly $13 million. The stock yields 12.8% as I write, which means our man is banking $1.6 million per year in his own dividends.

Kaufman founded Arbor 40 years ago as a lender for single-family mortgages. True to its name, the company sent every new homeowner a tree at loan closing!

In the 1990s, Arbor expanded its lending to multifamily and commercial properties. It found a “sweet spot” in loans between $1 and $5 million – too small for the big players, too big for the small players, but plenty profitable for Arbor in between. Arbor eventually sold its residential business to Bank of America in the 1990s to focus exclusively on this perennially underserved market.

Arbor has been named top small loan lender by partners such as Freddie Mac and Fannie Mae who have praised the firm for treating its small loans with the same importance as its large customers.

This was the first of many smart business pivots for Arbor. Founder Ivan is our type of entrepreneur. He still runs the company, and he’s always looking ahead.

Mortgage rates recently hit 23-year highs. Fortunately, Arbor is long gone from the residential lending business!

It’s also diversified away from commercial real estate. Which, quite frankly, is the reason the stock is so cheap today. “Going to the office” will never be the same after Covid. But Arbor is wrongly lumped with commercial lenders and landlords. It doesn’t plant in that forest.

Smartly, Arbor has had these cash flow diversification wheels in motion for some time. In the mid 2010s the company made a particularly big bet. At the time, Arbor was only valued at $325 million. Ivan threw down a chunk of change—$250 million!—to purchase a commercial mortgage-lending agency and its in-house technology platform.

Ivan didn’t have much margin for error acquiring something close to Arbor’s size. Fortunately, he knew what he was doing. The technology belonged to Arbor Commercial Mortgage, an independent company the big boss had previously spun off from the mothership in 2004. He knew what he was buying, inside and out!

It was a smart move because it created a new stream of loan servicing income. This grew to one-third of Arbor’s total sales in just two years—a diversified and protected income stream.

Today, Ivan refers to this as Arbor’s service income annuity. It amounts to $240 million of annual profits, which equates to $1.20 per share.

ABR’s quarterly dividend is $0.43 per share. This annuity covers two-thirds of the annual payout off the bat.

Plus, the company still makes money lending. When we initially added Arbor to Contrarian Income Report in 2018, we admired the Arbor’s loan portfolio:

Its own loan portfolio is now short duration (two to five years), which means ABR is positioned to make more money as rates rise. (It won’t be stuck holding the low-interest long-term loan bag!)

This was clutch in 2022 when rates finally began to rise for the first time in a long time. In total, the company earned $0.57 per share last quarter—plenty to cover its payout.

ABR has a comfortable 75% payout ratio. Plus, it doesn’t have to reinvest excess profits to grow: the biz is all human capital and computers.

Most importantly, Kaufman is the man. He stared down the end of the traditional office and smartly pivoted ABR away from commercial real estate. Just in time.

Is ABR perfect? Of course not. Some of the “short research” cherry picks negative Google and Yelp reviews of Arbor’s properties. Which, without context, seems worrisome. But my bet is that Kaufman knows where his corporate weaknesses are, which is why he shelled out another $1.5 million of his own money to take advantage of his low stock price and big dividend.

ABR not only pays 12.8% today, but also the company raised its payout twelve out of the last fourteen quarters for a cumulative increase of 43%. Forty-three percent!

Would you get in the way of this freight train, and pay 12.8% per year to bet against it? No way. We contrarians will gladly take the other side of this trade.

Sorry, basement blogosphere—we’re with Kaufman.

Hidden dividend gems like ABR are a product of my #1 income investing secret. Believe it or not, there are many more big dividends with serious upside. I call them “Perfect” Income Investments—click here and I’ll explain more.