Remember a few months ago, when the “buy Europe” trade was red hot?

Well, if you’re like me, you’re wondering where all the hype went! Now “buy America” is back on, but European markets are still sky-high—well ahead of their American cousins.

That spells trouble for anyone with a portfolio that’s still tilted too much toward Europe.

So today we’re going to look into where things are headed (hint: back to the US in a big way!). We’ll also delve into three funds with European exposure (two of which are closed-end funds sporting double-digit dividends) that I urge you to hold off on now.

Headlines Drove “Buy Europe,” But Corporate Profits Failed to Materialize

The Financial Times was one of many outlets cheerleading a shift to Europe from America back in the spring. At the time, this sentiment was driven by tariffs, seemingly overextended US tech stocks and surging US markets.

“There’s all sorts of reasons to like Europe, all sorts of reasons to hate the US,” contributor Katie Martin said in an April 25 FT podcast.

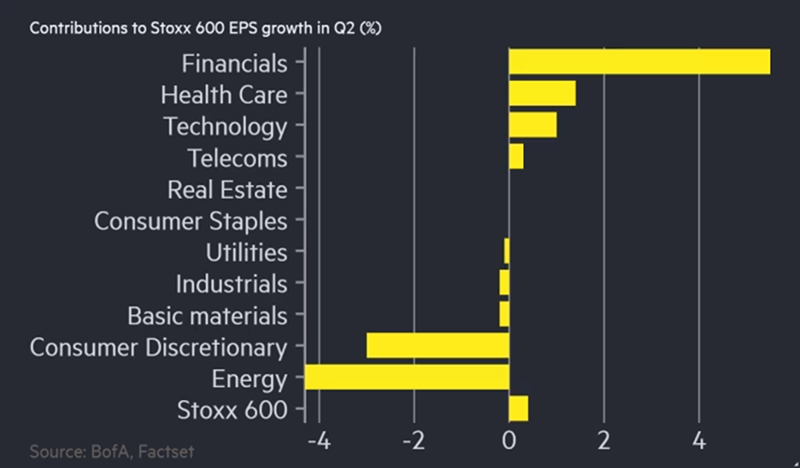

The buy Europe trade was working well as recently as June, when the FT again reported that “European small-caps outshine US rivals as investors bet on growth revival.” Note the phrase growth revival here: The idea was that European stocks were overlooked and would gain attention when their earnings grew. Except that didn’t happen, with European firms posting disappointing earnings, as shown in the table below (more on this in a moment).

European Firms’ Second-Quarter Profits Fail to Impress

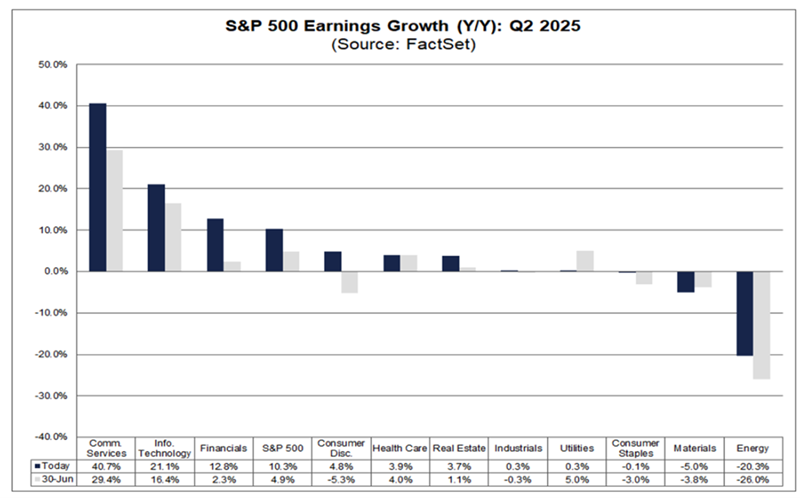

Meanwhile in the US, companies saw 9% year-over-year earnings gains in Q2, meaning their average profit growth was much higher than the best sector in Europe (financials). And if you compare the best sector in the US—communication services (see chart below), which includes firms like Alphabet (GOOGL), Meta Platforms (META) and Netflix (NFLX)—to its cousins in Europe, the difference is staggering.

As you can see at left above, the US sector’s 40.7% earnings growth is many times greater than the best European companies can produce. Meantime, Europe’s tech and telecom companies combined can’t even muster more than 1% average growth between them.

Where does that leave the European markets? Well, they’re simply not reflecting this reality.

European Stocks’ Big, and Flimsy, Lead

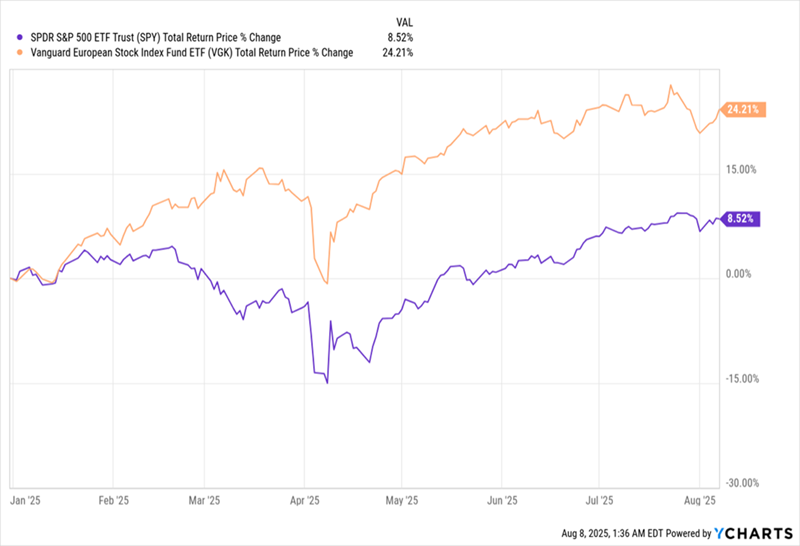

With S&P 500 benchmark SPDR S&P 500 ETF Trust (SPY)—in purple above—far behind the Vanguard European Stock Index Fund (VGK), in orange, as of this writing, it’s clear, based on our look at earnings, that European stocks are overbought.

This makes VGK a fund to avoid. But ETFs aren’t our main focus at CEF Insider. So let’s turn to two CEFs that could face similar pressure.

That, by the way, doesn’t mean these are bad funds—quite the contrary. But now is not the time to buy them, as they do have significant European holdings likely to weigh on them in the coming months.

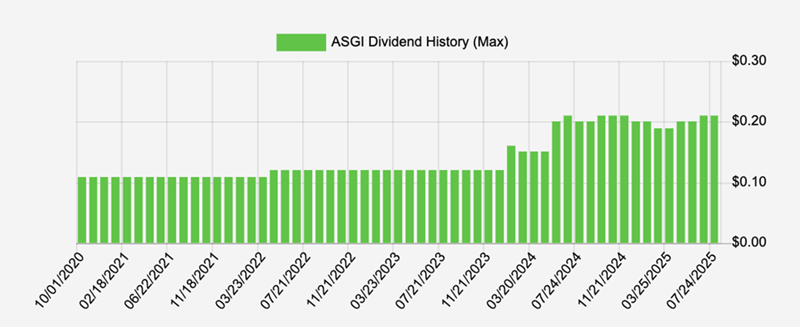

The first one is a good example of a fund I’ve liked in the past and will surely like again at some point: the abrdn Global Infrastructure Income Fund (ASGI). This fund yields a rich 11.8%, and its payout has been steady—it’s even moved up recently (though the dividend varies based on management’s assessment of the market and other factors).

ASGI’s High, and Growing, Dividend Masks European Overexposure

Source: Income Calendar

Moreover, the fund isn’t inherently European—in fact, it has 55% of its portfolio in US stocks, including cornerstone infrastructure players like Norfolk Southern Corp. (NSC) and NextEra Energy (NEE). Still, it has 22% of its holdings in continental European stocks, plus another 2.6% in the UK.

That’s enough to put a drag on the fund’s portfolio when European stocks snap back to reality. Plus there’s ASGI’s rich valuation.

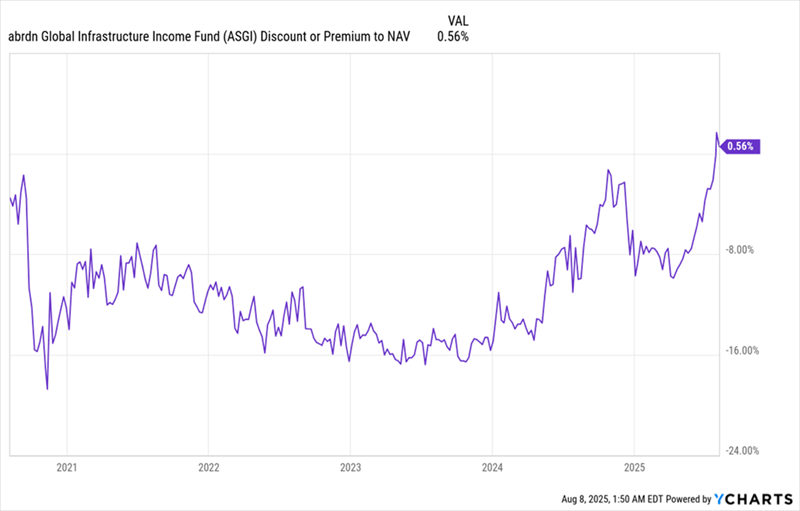

ASGI’s Vanishing Discount Is a Big Risk

ASGI has been riding the enthusiasm about foreign assets, causing its discount to net asset value (NAV, or the value of its underlying portfolio), which was averaging around 12% going into 2025, to evaporate. When European stocks correct, this fund will likely see a discount—and a consequent drop in its share price.

Our second, and final, CEF to be wary of now is the PIMCO Income Strategy II Fund (PFN). This corporate-bond fund yields 11.5% and has held its payout steady since the pandemic days of 2021.

However, as I write this, PFN trades at a 5.6% premium to NAV. And while it does have about 77% of its portfolio in the US, its largest allocations by country include European nations—France (3.2%), Spain (3%) and Germany (2.4%), to be precise—and Brazil (2.5%), which faces particularly steep tariffs from the US.

To be sure, these are conservative allocations, but throw in PFN’s premium and you get a real risk of a pullback, in both the fund’s NAV and its market price, on any significant European selloff. And lower returns, especially in the fund’s NAV, could put pressure on PFN’s payout.

The bottom line on all three of these funds? While geographic diversification is key for any portfolio, it’s only a matter of time until European stocks drop to reflect their meager earnings growth. Until European firms start booking bigger profits, we’re best to look elsewhere for growth.

These 4 Ignored Funds Give Us the Best US Companies (With 9.7% Dividends)

US stocks are clearly crushing Europe on the earnings front, and nowhere is this clearer than in artificial intelligence. US companies aren’t just leading the development of this breakthrough tech—they’re implementing it at speed.

That’s supercharging their profits and cutting their costs. We’re already seeing it in the numbers.

It’s not too late to buy the biggest American AI winners—and you can do so now through 4 bargain-priced CEFs paying 9.7% in dividends between them. PLUS, thanks to their unusual discounts, we can look forward to more upside as AI supercharges the already dynamic US economy.