This market rally could roll right through the summer (so much for “Sell in May and go away!”), and we’ve got two sweet bond buys to play it.

That’s right, I said bonds because there are more bargains in bond land than in stocks right now. While stocks could keep floating higher, the last thing we want to do is chase this rally.

Instead, we’re going to ride along on the stock side of things. In bonds, though, the state of play is a bit different.

We’re going to list our two bond picks in order of appeal shortly, capping this article off with our top selection—an unsung closed-end fund (CEF) trading for 12% below its “true” value and yielding a stout (and tax-free) 5.8%.

Powell’s “Quiet QE” Has Yet to Be Fully Felt in Bonds

Over the last few weeks, we’ve talked a couple times about the Fed’s “Quiet QE.” That’s what we call Jay’s habit of going full Dirty Harry when talking about interest rates and then, behind the scenes, quietly pumping liquidity into the system.

He did it in March 2023, when the banking system was wobbling. The last thing Jay wants is Financial Crisis II, so he put his printing press in silent mode, and it’s been humming along in the Fed’s basement ever since, as you can see in this chart of bank reserves:

Then there’s what you might call “loud” QE, which is taking a haircut, too. At his early May press conference, Jay said he’d cut the amount of Treasuries the Fed lets run off its balance sheet by half, to $25 billion from $60 billion.

In other words, the central bank will buy any Treasuries over the $25-billion cap. We see what you did there, Jay!

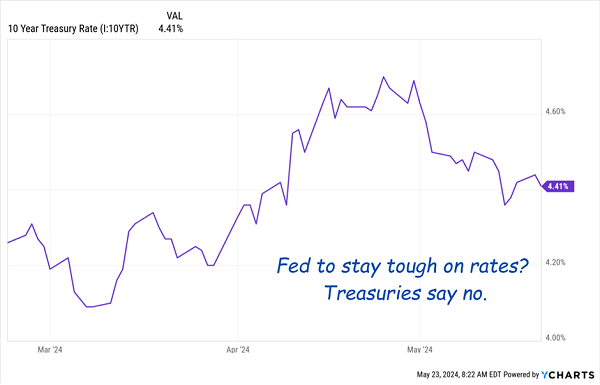

The 10-year Treasury rate, which controls the “long” end of the rate curve (and regularly thumbs its nose at the Fed) has long since figured Jay out. It’s continued to move lower since peaking below the 5% line in April, the last time inflation worries spiked:

10-Year Sees Through Jay, Telegraphs Next Fed Move

It’s likely to keep falling (in the usual two-steps-forward, one-step-back way, of course), as Jay keeps quietly supporting markets for now, then cuts the Fed funds rate as the economy slows.

The upshot? Higher prices for bonds!

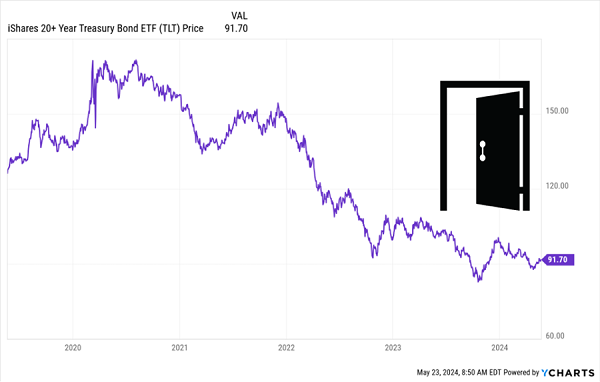

The most direct play here is the iShares 20+ Year Treasury Bond ETF (TLT), the go-to for tracking Treasury prices.

We bought TLT in November 2022, another time investors overestimated inflation’s staying power, in my Contrarian Income Report service. We only held TLT for about seven weeks, from November 4, 2022, to December 21, 2022. But what a seven weeks. TLT rewarded us with fast 10.6% total returns, mostly price gains. These profits annualized to 82%!

Not Bad for a “Boring” Fund!

This time around, TLT is beaten down again, a nice entry point as rates continue to fall and bond prices make their corresponding rise:

Quiet QE, Looming Slowdown Drive Our TLT Opportunity

One side note here: Please note that many websites will say TLT only yields 3.8%. That’s not true. Always use SEC yield when evaluating bond funds.

This is the distribution stat developed by the Securities and Exchange Commission itself to support a truer yield measurement. The trailing 12-month yield—which is lazily quoted—gets “stale” quickly. Things turn on a dime in the bond world!

SEC yield reflects the interest the fund earned, minus expenses, over the past 30 days. It’s the best guide for us today and tomorrow. For bond yields, we want to know where we’ll go, not where we’ve been. In TLT’s case, we’re looking at a richer 4.6%.

To be sure, an economic slump will inevitably arrive. When it does, investors will flock to the safest bonds on the planet. They always do! That makes TLT appealing here. But there’s another ticker that looks even better. Let’s talk about it now.

Municipal-Bond CEFs Top Bond ETFs for Income, Upside

Municipal bonds (used by state and local governments to fund infrastructure projects), which is too bad, because they’re a terrific play as rates decline. And the Nuveen Municipal Credit Income Fund (NZF) tops our list here.

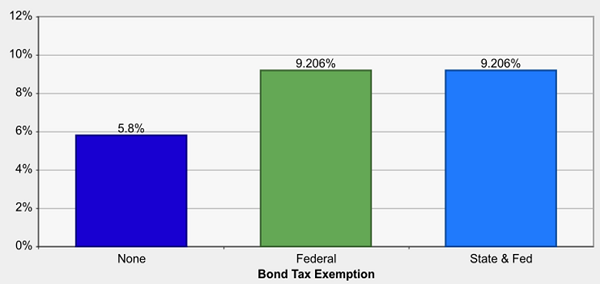

The main reason? Dividends! NZF yields 5.8%, but its payout is federally tax-free for most Americans. That makes a huge difference, especially for those in the highest bracket:

5.8% “Headline” Yield Jumps 58% for Top-Bracket Ballers

Source: Raymond James taxable-equivalent yield calculator

Unlike ETFs, CEFs generally have the same number of shares for their entire lives. That means they can, and regularly do, trade at different levels than their portfolio values, and very often at a discount.

(You don’t get this deal with ETFs, which never trade at a discount.)

Right now, muni CEFs are cheap. NZF sports a 12% discount to net asset value (NAV), meaning we’re getting its muni-bond portfolio for 88 cents on the dollar!

Over the last five years, the fund has sported an average discount of 7.6%. So a return to that level—inevitable in my view—would “bake in” a 5.3% bump in the share price. That’s before we factor in NAV gains, which seem assured as rates move lower and “safe and sound” munis appeal to more conservative folks.

Nuveen is our go-to for munis at Contrarian Income Report because they get the first call when new issues are released and, hence, the best deals.

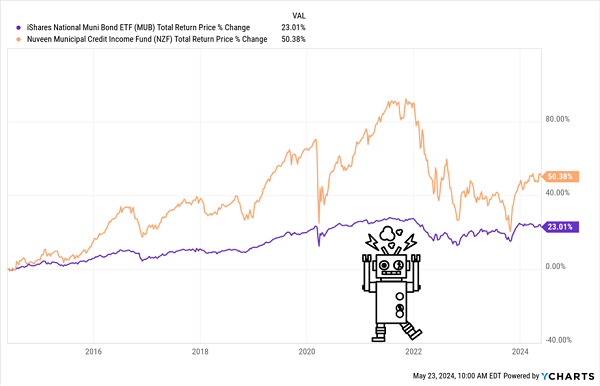

That’s a huge, totally underappreciated edge, and we can see it in action when we stack NZF up against the “algorithm-run” muni-bond benchmark, the iShares National Muncipal Bond ETF (MUB).

Don’t Let the Robots Run Your Muni-Bond Holdings

One more thing: In the event of a crisis, we know the Fed will step into the muni market. Heck, if Powell is running the presses (albeit in the background!) today, we know that if munis even begin to show stress, Jay will be buying alongside us.

So as the financial world enters the “summer doldrums,” munis stand out as a great place to put money to work—and NZF is at the top of our list.

3 More High-Paying (and Cheap!) CEFs to Ride the Coming “Bond Bull”

The bottom line here is that the last few months could set us up for a much longer “bull run” in bonds.

NZF is a smart play at these levels. Now let’s build on it with three other bond CEFs kicking out even bigger dividends—up to 12%—and trading at big discounts, too.

Our play here is simple: Buy … then collect these three funds’ rich payouts while their discounts evaporate—and send their share prices soaring.

One of these funds is run by a guy who’s been making the right calls so often he’s called the “Bond God.” Another is the brainchild of one the top bond managers on the planet and kicks out that 12% payout I mentioned a second ago.

The third is one of the most reliable wealth-generators out there, with a 1,530% return since inception.

Even a slight reduction in rates would put a nice tailwind behind these three funds. The key is to get in now, before that happens.