This market bounce is giving us a rare window to sell our laggards—and snap up stocks that have been unfairly left behind.

When we dump losers, we want do it into strength. And on the flipside, bounces like this often leave strong bargains in their wake.

Let’s start our “rebound rotation” with two blue-chip laggards lots of people own. Then we’ll pivot to two holdings of my Hidden Yields service that are smart, contrarian places to put cash now.

GIS Is a Prime GLP-1 Target

General Mills (GIS) draws a lot of revenue from snacks people eat routinely (and often without thinking much about it), like Bugles, Dunkaroo cookies and high-sugar cereals like Cocoa Puffs, Cinnamon Toast Crunch and Cookie Crisp.

Unfortunately, those products put the company in the tracks of rising GLP-1 use; these drugs suppress appetites for just these kinds of products. Everyone knows more people are taking these drugs, but when you look more closely, the numbers are stunning.

On April 8, for example, Morgan Stanley Research released a new forecast stating that 55 million Americans will be on GLP-1s by 2035, up from its original forecast of 35 million. This is no fad—it’s a permanent shift in food consumption.

General Mills is pivoting in response, including adding premium snacks (which consumers, including GLP-1 users, will likely keep buying—see my take on Hershey below) and smaller packages aimed at dieters. But it’s far from clear that these moves will be enough.

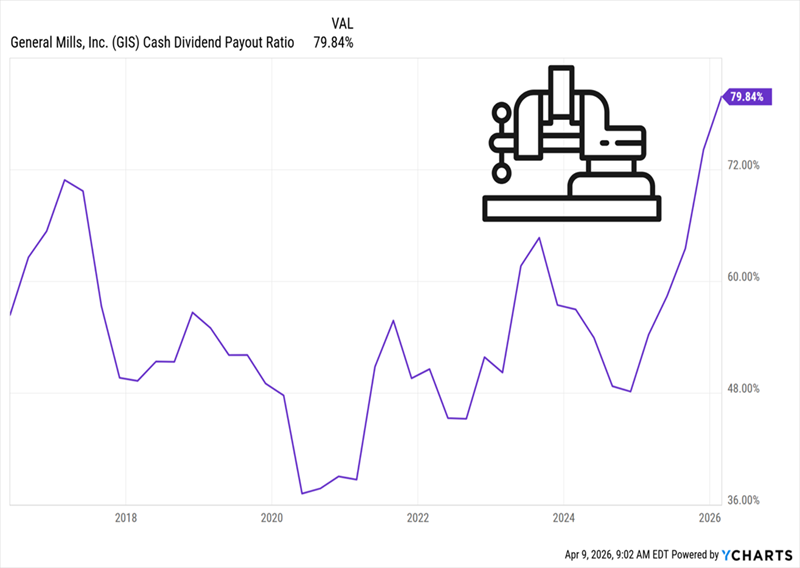

Meantime, GIS is the definition of a yield trap, with a 6.7% dividend. Too bad that payout has consumed a high 80%—and rising—of the company’s free cash flow in the last year.

Rising Payout Squeezes GIS’s Dividend

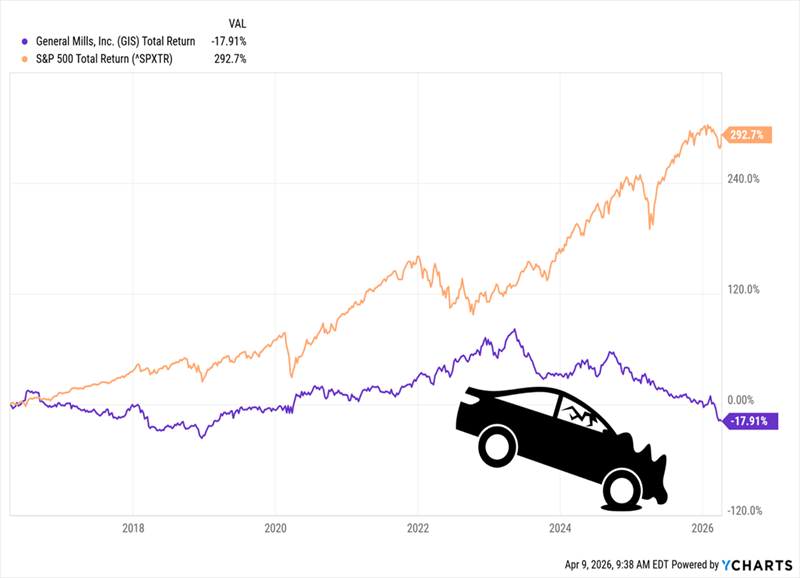

Plenty of investors see GIS as a “safe” stock because its products are considered essential, but that idea just doesn’t hold up: Over the last 10 years, the stock has returned negative 18%, while the S&P 500 has soared nearly 300%:

“Safe” Stock? No Way

Don’t buy the turnaround story here. GIS has a long way to go before it delivers positive returns. And if history is any indication, the stock may never get there—especially with the speed at which the healthier-eating trend is moving.

Coke Looks Like “Dead Money” (at Best) in 2026

Next up, the Coca-Cola Company (KO), which faces similar problems as GIS. To be fair, Coke is in a better spot because it has plenty of low- (or no-) calorie drinks to push, such as Coke Zero, Dasani bottled water and various coffees and teas. But the shift toward healthier eating is still a headwind.

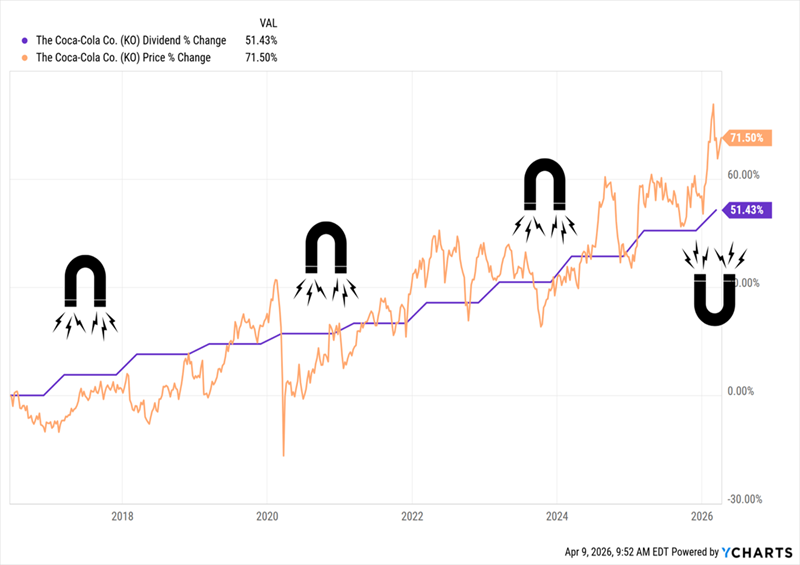

Meantime, Coke’s lame dividend growth—typically just a penny or two a year—isn’t enough to get our hearts racing, especially with the stock yielding just 2.7%. But despite all that, investors still cling to Coke as a “safety” stock. That’s why they’ve bid its shares well above its sluggish payout growth.

KO Gets Out Over Its Skis

If you’ve been reading me for a while, you know I preach the power of buying fast-growing dividends, because they pull the stock up with them—a phenomenon I call the Dividend Magnet. But the magnet can work both ways, pulling down a stock that’s gotten too far ahead. That’s the risk here.

With that said, let’s pivot to two “essentials” stocks I recommend now, starting with another food maker investors regularly (especially these days) get the wrong idea about.

Hershey: A Contrarian Play On Healthier Eating

I’m talking about the Hershey Co. (HSY). I know: You’re wondering how I could recommend a maker of chocolates given what we’ve just discussed. Hear me out.

For one, there’s evidence that GLP-1s are less of a problem for chocolate makers. New research from Lindt & Sprüngli, for example, found that among GLP-1 users, sales of chocolate actually rose nearly 17% in 2025. The findings were based on an internal study of the company’s sales by market-research firm Circana.

Wait, what?

When you think about it, it makes sense, because it suggests these folks are ditching “repetitive” snacks like chips, salted peanuts and the like for small indulgences, like chocolate. This rhymes with why we like Hershey in the first place: People are likely to keep buying small treats, even in a slow (and inflation-weary) economy.

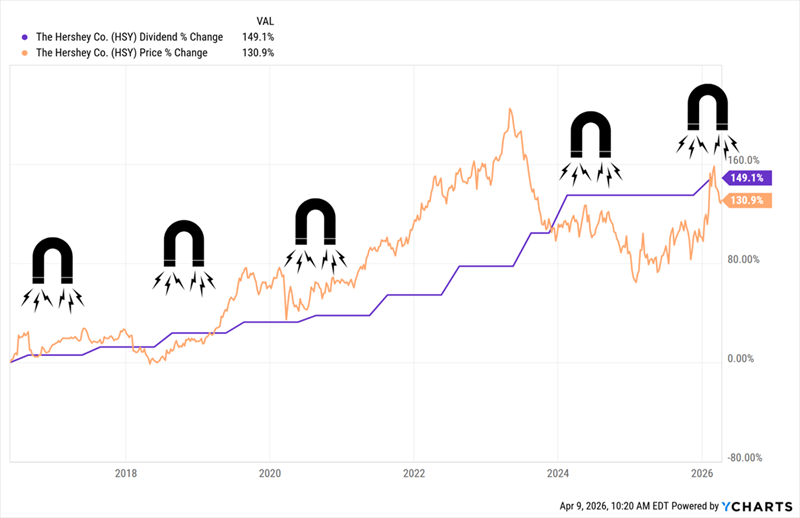

That’s backed up by Hershey’s sales growth, which is ticking right along, rising 4.4% in 2025 and forecast to grow 4% to 5% this year.

Meantime, Hershey expects strong earnings growth as it recovers from a cocoa-price spike in 2024. That’s breathing new life into the dividend, which was hiked 6% last year after holding flat for a short time. That, in turn, adds more “pull” on the stock, which is trailing its payout as we speak:

HSY’s Dividend Magnet Is Tuned

Hidden Yields members who bought HSY on my February 2025 buy call are up 24.7% as I write this. But it’s not too late. Thanks to the above “dividend lag,” more growth is on the table here.

Beyond Food: Visa Is Our Favorite “Tollbooth”

Not many people see Visa (V) as an “essentials” stock, but it is.

Visa controls a large slice of the global payments network, collecting a “toll” on every purchase—from the discretionary to the necessary—that rolls through it.

Management isn’t just sitting back, though: It’s looking ahead, making sure it doesn’t get left behind in digital currency, particularly the rising use of “stablecoins.” These digital “coins” are far from the crypto wild west we’ve heard about these last couple of years; they’re tied one-for-one to the US dollar. Their main use these days is for cross-border transactions, as they can be processed without being converted to local currency. Visa already allows stablecoin settlement on its network.

Meantime, in the here and now, US consumer spending continues to hold up, rising 0.5% in February, ahead of its 0.3% rise in January.

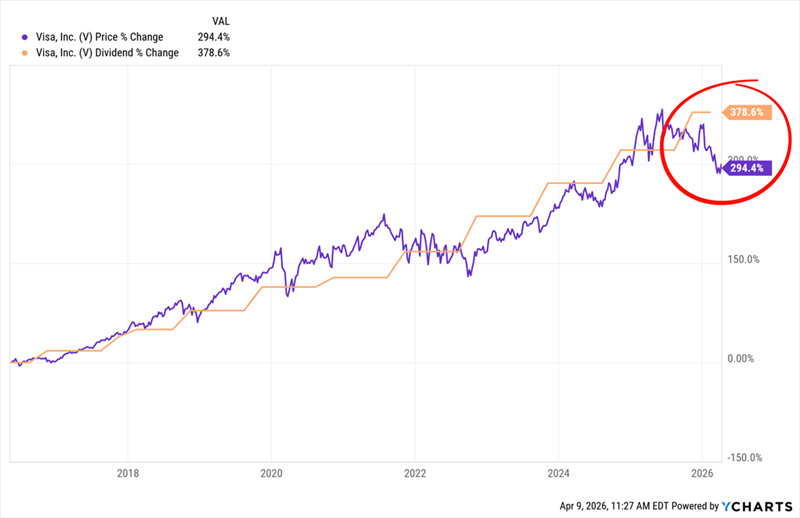

Even so, Visa has pulled back 11.7% this year—a clear mismatch for a company that saw revenue and adjusted EPS each jump 15% in its fiscal 2026 first quarter. That’s opened a wide gap—and another buy window—between Visa’s dividend and its share price:

Visa Is Unloved—in More Ways Than One

Visa yields just 0.7% today, but don’t let that put you off—with the 379% payout growth you see above, it would be paying 3.4% on a buy made 10 years ago. That’s nearly 5X the current yield and is in addition to the 294% price gain.

As you can also see, buyers have profited off every dip in the chart above. There’s no reason for this time to be any different.

That last point, in fact, nicely sums up our strategy: Sell laggards into strength, then buy strong stocks the market has left behind. And that’s exactly what we’re doing with these four tickers.

These 5 “Dividend Magnet” Plays Could Be Our Next 148% Winners

When it comes to the Dividend Magnet, we want to buy at the point where the stock has fallen way behind its dividend growth.

That way, when it snaps back, we get maximum upside. That pattern is obvious in the cases of Hershey and Visa, and these two aren’t the only Dividend Magnet plays I’m watching now.

I’ve assembled 5 other stocks into a single “Dividend Magnet Portfolio.” They’re primed for even bigger “snap-back” upside, and I want to make sure you get a shot at these before they kick off their next rise.

This is exactly the same setup that drove 148% gains in Texas Instruments (TXN) and 82% returns in Progressive (PGR) for Hidden Yields members. And now it’s setting up for us again.