“Adrian, it’s going to Jack. But you have to act like you have the ball.”

My star adjusted his mouthguard and nodded, still breathing heavily.

“Everyone’s gonna follow you.”

I looked around our huddle. Adrian had just motored for a 95-yard touchdown run on our first play from scrimmage—the very first play of our season. Now we were going for the two-point conversion to take the lead.

I knew the defense was dialed in on Adrian. The opposing coach, Jersey Mike, was now ranting and raving like a lunatic. His Eagles had put together a somewhat disjointed but ultimately effective drive in our YMCA contest, eventually scoring a touchdown.

My Bills answered in one play. Which really frustrated the previously ebullient Jersey Mike. (Act like you’ve been there before, JM! Ha!)

Our two-point play relied on Adrian pretending he had the football again while I sent Jack around the other side of the quarterback for an end around. Jack would receive the handoff from our quarterback and run in the opposite direction that Adrian was heading.

Our decoy played it perfectly. Still huffing and puffing from his epic sprint, he ran his distraction assignment to perfection. The entire defense followed him. Jersey Mike even screamed, “Hey! Watch the kid in the blue jersey!”

Meanwhile, Jack trucked around the other end untouched, putting a smile on his face and his parents’ faces. (Would have put a smile on my face too, but unlike my counterpart I stay relatively level-headed for the kids.) The two-point conversion was good. Eight to seven, Bills, en route to a 26-13 opening week victory.

In eight-to-ten-year-old flag football, the key is the play the defense can’t see: The decoy matters as much as the actual ball carrier.

And hey, we contrarian investors live on misdirection, too. When the suits zig, we zag!

Vanilla investors always assume that what just happened is going to happen again. Stocks sold off, so they will keep declining. Or, a hot stock will stay hot. These Jersey Mikes of the investing world think it’s going to Adrian again on the New York Stock Exchange.

The profitable action is what’s about to unfold. The counter move. The invisible company that nobody knows about.

Linde (LIN) is the world’s largest industrial gas company. Everybody knows heating gas, but nobody thinks about industrial gas. Yet, every single AI chip made in America requires Linde’s ultra-high-purity nitrogen to exist. No gas, no chips. No chips, no AI.

Linde builds production plants directly on-site at its biggest customers’ facilities next to chip fabs, oil refineries, and steel mills. Its customers sign 10-to-20-year contracts that include minimum volume commitments. Once that plant is built, it is not going anywhere.

And because industrial gases are heavy and expensive to transport, Linde has geographic moats around each of its production hubs. A competitor can’t just roll into Arizona and undercut Linde’s local pipeline network. Too hard, too costly, and simply too late.

Last month, I recommended LIN to my Hidden Yields subscribers. The stock has already moved 3% higher while the S&P 500 has been gyrating wildly. Nice!

And the best part? Linde is still a great buy at today’s price!

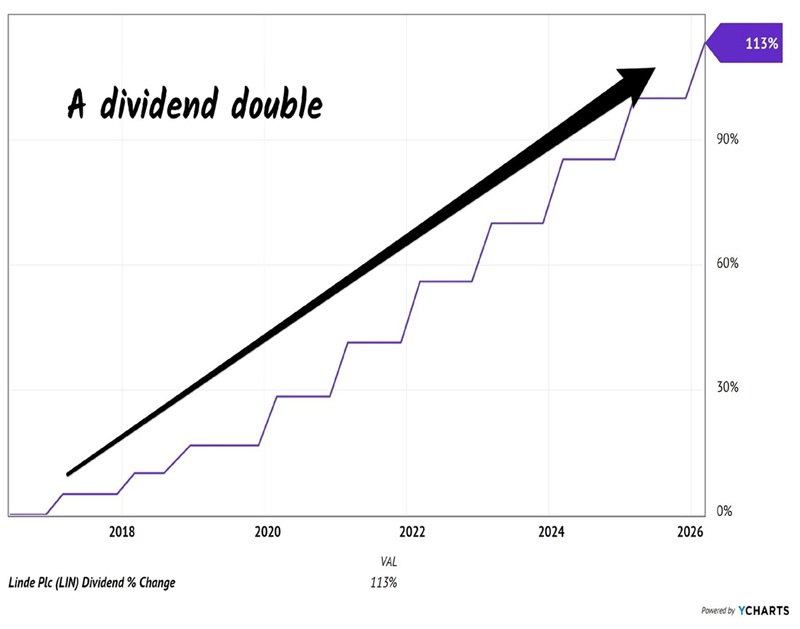

The run is likely to continue. Linde just announced its 33rd consecutive annual dividend increase—a 7% raise year over year. The company has more than doubled its divvie over the past decade. And its payout ratio sits at a historically low 41%, which means the next raise has room to accelerate.

This Doubling Dividend is About to Speed Up

Remember the dividend magnet? When a company like Linde hikes its payout year after year, the stock price follows like a magnet pulling iron filings. Linde’s dividend is marching higher. The stock price will follow. It always does.

Plus, Intel, TSMC, and Samsung are all building new semiconductor fabs in Arizona and Texas today. We’re talking billions of dollars of construction—all requiring Linde’s gases every single day for decades. This is recurring revenue locked in by long-term contracts.

And the big number is the clean energy project backlog: $10 billion. Yes, despite Washington battles, clean projects are still happening and they require Linde’s specialty gases.

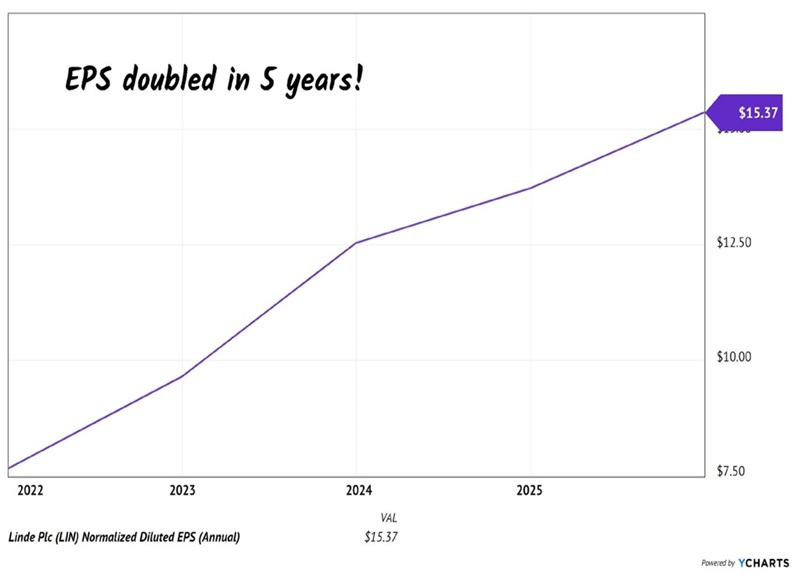

Management expects $2.5 to $3 billion of these projects to start generating revenue in 2026 alone. Linde’s 2026 guidance reflects this, expecting 6% to 9% EPS growth:

Linde’s EPS Growth, Already Strong, About to Hockeystick Higher

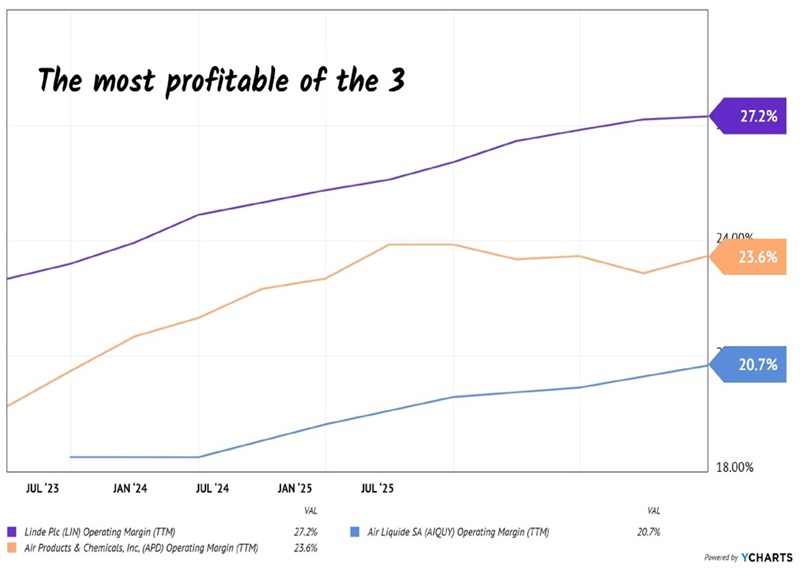

There are only three companies on the planet that can supply industrial gases at this scale, but Linde is the biggest and most profitable:

Linde Leads the Industrial Gas Oligopoly in Profitability

The defense chased Adrian. Jack scored. That’s how we invest—buy what the herd overlooks, collect the dividend, and let the vanilla crowd figure it out later. Linde is our Jack.

Linde is already profitable for us. But you know our contrarian offense—we’re on to the next play!

This month, I’m recommending a new pick in my Hidden Yields service—a Dividend Aristocrat with 31 consecutive years of payout boosts quietly riding one of the biggest commodity comebacks of the entire decade. While the world watches Adrian and then gets distracted by Jack, this is the third play I’ve got in my back pocket. And the defense hasn’t seen it yet.

I’ve built an entire portfolio of these “invisible” dividend growers in Hidden Yields. These are companies with rising payouts, lagging stock prices, and the kind of competitive moats that let you sleep at night.

These dividend magnets are on sale right now. Click here to see my full research, and on Friday you’ll receive this month’s newest pick and my complete Best Buys list.