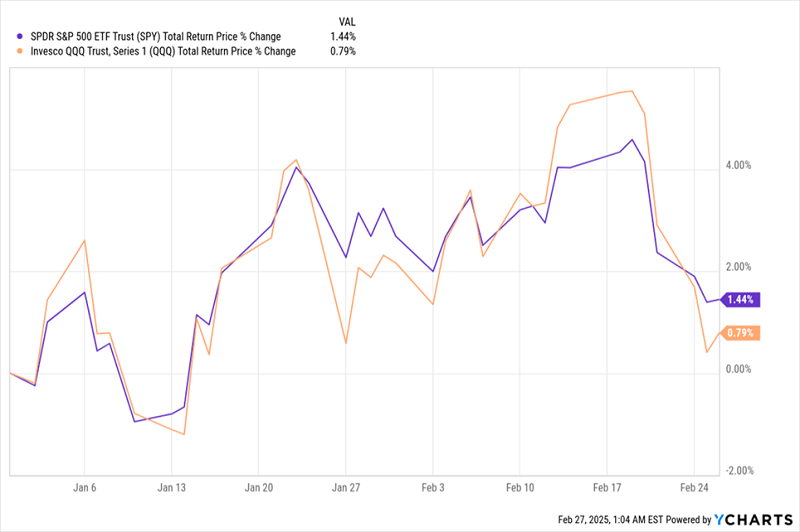

There’s no doubt it’s been a rough couple weeks for stocks: Both the S&P 500 and the tech-focused NASDAQ have wiped out most of this year’s gains, as of this writing.

Stocks Reverse Across the Board

The bigger decline among the NASDAQ, compared to the S&P 500, is notable here because the NASDAQ involves both higher risk and higher reward: With a heavier focus on tech stocks, it’s more volatile than the more diversified S&P 500.

But it also reflects where many of the higher profit margins have been among US firms. Hence, it has outrun the S&P 500 for a long time.

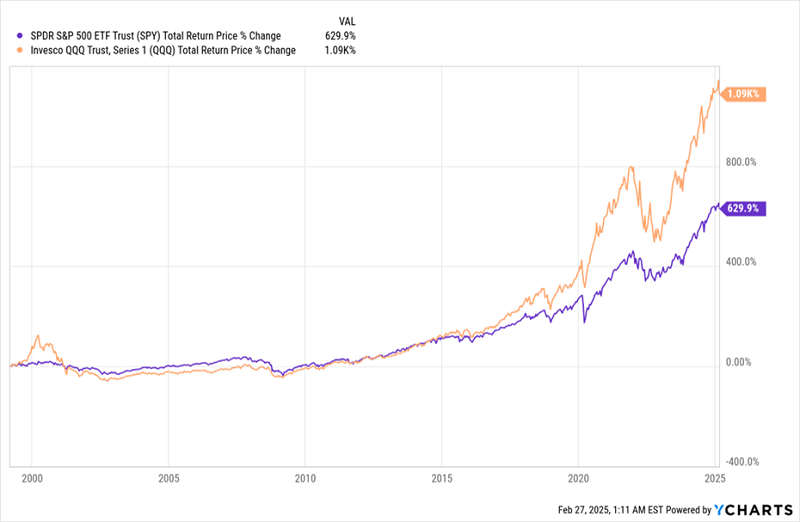

Despite Burst Bubbles, the NASDAQ Wins Long Term

With the big run-up we’ve seen in stocks, high valuations for both indexes and higher volatility, it’s fair to wonder if now is a good time to add to your holdings of stocks, or stock-focused closed-end funds (CEFs).

Diversification is, of course, the key to managing risk. That includes spreading our money across the world, across stocks in different sectors and across asset classes, including bonds, real estate investment trusts (REITs) and preferred shares.

It also includes, crucially, continually adjusting our allocation to stocks, bonds and other assets as our goals, age and risk tolerance change.

That’s in contrast to one so-called “diversification” strategy we want to avoid like the plague, especially in times like these: sticking to the rigid “60/40 portfolio,” a tired “rule of thumb” that, as the name suggests, involves devoting 60% of your portfolio to stocks and 40% to bonds.

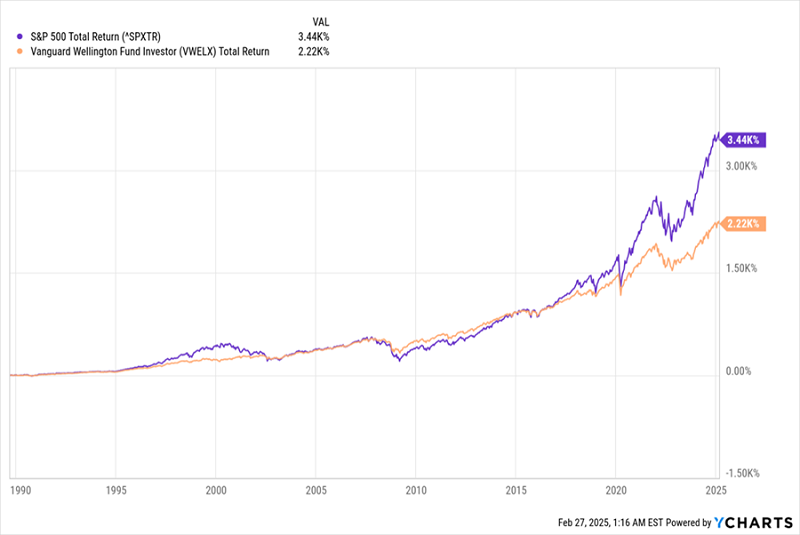

This might sound familiar if you have a financial planner, as many stick to the 60/40 asset split. Even if you don’t, you might have gotten a recommendation to buy a fund like the Vanguard Wellington Fund (VWELX). This fund has been around for nearly a century (its IPO was in 1929), and it has nearly a 60/40 allocation (closer to 67% and 33%, but no matter).

Unfortunately, owning VWELX (in orange below) has resulted in a big lag in performance compared to the S&P 500 over the decades.

60/40-Inspired Fund Falls Behind

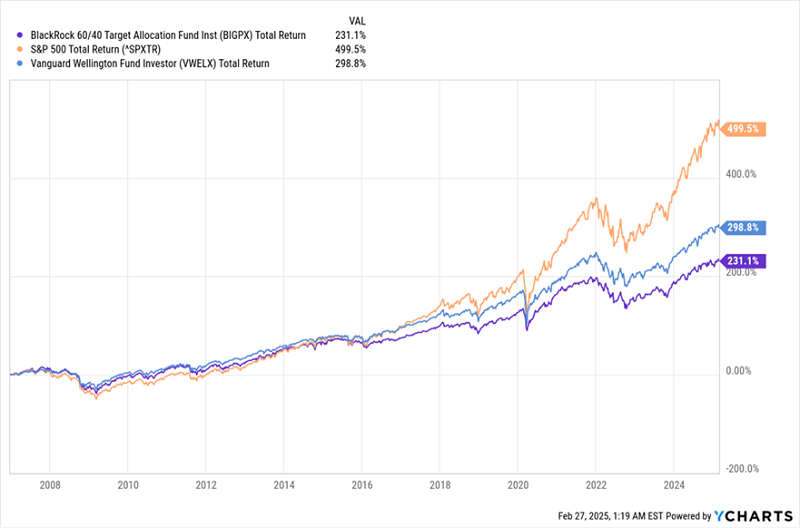

In more recent history, we’ve seen VWELX do poorly compared to the market along with other, newer funds with stricter 60/40 allocations, like the BlackRock 60/40 Target Allocation Fund (BIGPX). Its performance since 2007 (in purple below) has been worse than that of the Wellington fund (in blue).

Strict 60/40 Approach Comes Up Short Again

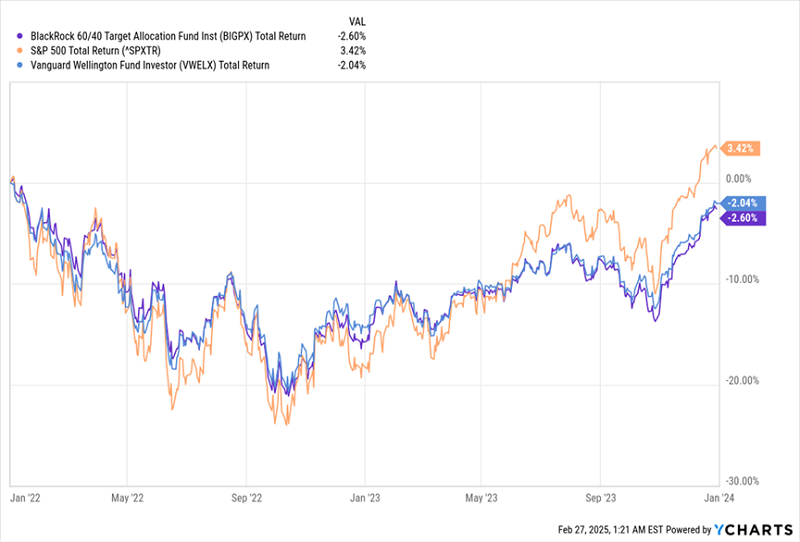

What about times of extreme stress, like the 2022 crash? These periods are, after all, supposed to be what the 60/40 allocation is made for.

Well, it didn’t exactly pan out that way: In this case, the S&P 500 (in orange below) recovered faster than 60/40—measured by BIGPX (in blue) and VWELX (in purple). In other words, this “conservative” rule didn’t protect investors much.

“60/40” Funds Recovered Slowly From the 2022 Mess

Now here’s where the story takes an interesting turn. Because there have been times when the 60/40 portfolio has worked. Take the period following the dot-com bubble, when the Wellington fund (in orange below actually turned a profit while the S&P 500 (in purple) sagged.

60/40 Delivered Strong Gains Over Stocks … 25 Years Ago

But this doesn’t really happen anymore; not only did stocks recover faster than 60/40 in 2022, but following the subprime mortgage crisis, stocks recovered at about the same pace as a 60/40 did. This, again, shows that this “rule” worked in the past but, as of the early to mid-2000s, was no longer a realistic way to lower your risk.

Why did the 60/40 allocation outperform the stock market back then and stop succeeding in the mid-2000s?

One part of the answer comes down to regulation.

In 2000, the SEC cracked down on analysts’ practice of giving sneak previews of research to top clients, which allowed big funds to front-run retail investors. They did this with a law called Regulation Fair Disclosure (Reg FD) in 2000.

Then, a settlement with bankers, analysts and regulators called the Global Research Analyst Settlement of 2003 restricted how well funds could use research to get ahead of other investors. Further tightening of regulations beyond these new rules also ensured that big investors’ advantages were reduced, if not scrapped altogether.

This hurt the 60/40 strategy in one crucial way: It made the stock market more efficient. By ensuring information wasn’t selectively sent to big investors, the stock market instead began to go up more gradually and more directly, based on fundamentals. That, in turn, produced more reliable returns, helping attract more investors throughout the 2000s and 2010s, and lowering demand for bonds in the process.

Again, these rule changes are just part of a bigger story. But they help explain why 60/40 is still a fixture in the financial planning-world, even though it began to lose its punch over 20 years ago.

This Diversified Portfolio CRUSHES 60/40, Yields 8.3%

This is a great spot to bring up my favorite income plays, closed-end funds (CEFs) which yield around 8%, on average, as I write this.

Not only do they kick rich yields our way (often paid monthly), but they go well beyond stocks, so you can set up a personalized portfolio spread across just about every asset class you can think of: stocks, bonds, real estate investment trusts (REITs) and more.

AND you can squeeze a big income stream out of all these investments while doing it.

What’s more, because CEFs trade on the open market, just like stocks, you can easily buy and sell them, rebalancing your portfolio as your needs and risk tolerance change. That’s something a rigid rule like 60/40 just can’t offer.

To get you started, I’ve built you an “instant” 5-CEF portfolio that holds blue chip stocks, preferred stocks, corporate bonds and REITs. One of these 5 even uses a smart option strategy to juice its dividend—and cut its volatility, too.

On average, these 5 CEFs yield a stout 8.3%. And they’re cheap today, which is why I’m forecasting double-digit price upside in the next 12 months.

Click here and I’ll tell you more about high-dividend CEFs and why they’re so far off most people’s radar (for now!). I’ll also give you the opportunity to download a free Special Report naming all 5 of these diversified picks kicking out that rich 8.3% payout.