While tech is all over the news these days, there’s another corner of the market throwing investors cheap, and surging, dividends. These stocks quietly soared in 2025, but they’re still cheap enough for us to get in on now.

And we have plenty of ways to do so at a bargain.

Chief among them? A growing 7.2% dividend that’s suddenly on sale.

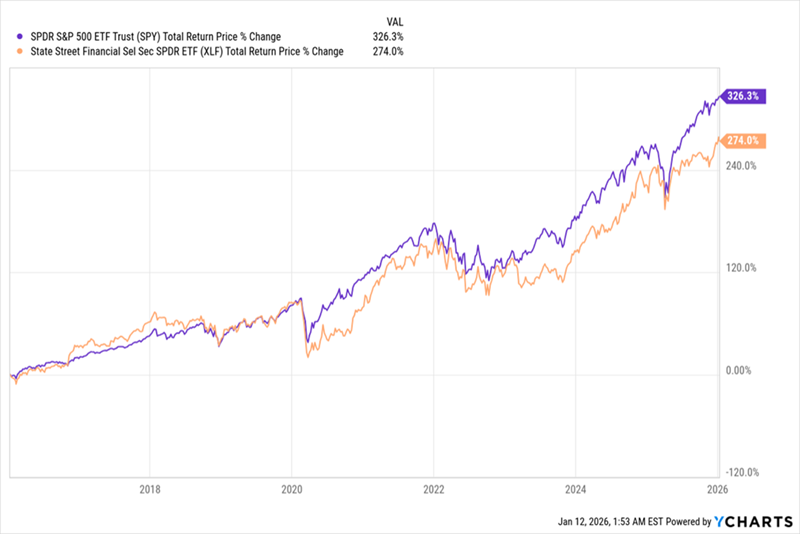

Let’s set the table on that strong fund with the 50,000-foot view: I’m talking about the financial sector, which returned 15% in 2025, going by the performance of the Financial Select Sector SPDR Fund (XLF).

That makes it the fourth-best performer of all sectors, behind tech, industrials and communication-services stocks—the latter of which actually includes tech names like Meta Platforms (META) and Alphabet (GOOGL).

But we don’t hear about financials much because, well, AI has everyone’s attention. The funny thing about that, though, is that banks, insurers and other financial firms are profiting from the AI buildout because they’re playing a key role in financing it.

So we can look at these stocks as a lower-risk “back-door” play on AI’s continued growth.

And despite financials’ strong run, they did not outperform the broader S&P 500, which returned 17.7% last year. That’s another good sign; if they had, it would be a signal that the financial sector is a crowded trade. But it’s not.

So we’re left with a sector that:

- Posted a strong (but not too strong) performance last year, and …

- Did so in the shadow of other, flashier sectors.

And then there’s this:

Financials Lag, Then Start to Close the Gap

After matching the S&P 500 for years, financials failed to recover alongside the market in 2023 and are still lagging. But as you can see at the right side of the chart above, the sector is starting to close the gap.

All of this points to a sector that’s “due,” despite last year’s decent return. In just a moment, we’ll talk about how we can get in at a bargain—a “double discount,” if you will—and grab that growing 7.2% dividend, too.

But enough about the sector’s past performance. What about 2026 (and beyond)?

Lately, industry insiders have been talking about a “supercycle” (as Goldman Sachs calls it) under which banks could invest in excess of $182 billion (to cite research from Barclays’ Jason Goldberg and other analysts) through a mix of “very robust pipelines” (to quote Erika Najarian at UBS).

That’s bank-speak for saying there’s a lot of pent-up capital for banks to invest with and more potential deals for them to profit from, so the recent high watermark of profits we saw from banks is likely to rise even higher in 2026.

Many people would approach a situation like this by parsing individual bank stocks like the Goldman Sachs Group (GS), JPMorgan Chase & Co. (JPM) or Morgan Stanley (MS). Others would look to an index fund like the State Street Financial Select Sector SPDR Fund (XLF) as a way to ride along with the whole sector.

Not us, though.

A Surprisingly Cheap 7.2% Dividend to Play a Looming Banking “Supercycle”

As income investors, we have little interest in XLF’s meager 1.3% dividend, so we’re looking to the John Hancock Financial Opportunities Fund (BTO) instead. This closed-end fund (CEF) focuses on the financial sector and holds a number of regional banks, such as Old National Bancorp (ONB), and investment-bank specialists, like KKR & Co. (KKR). It’s traded on the stock market, like an ETF, and also yields that whopping 7.2%.

There’s more to that dividend story, too.

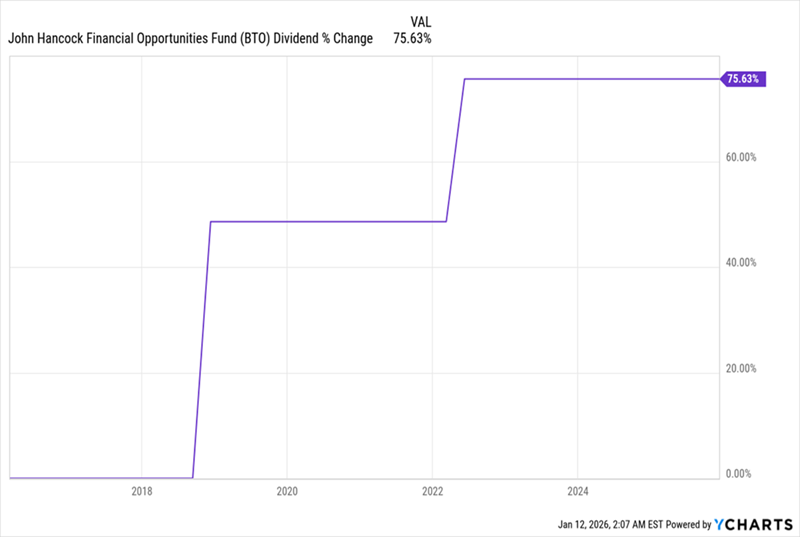

An Accelerating 7.2% Payout

As you can see above, over the last decade, BTO has raised its payout by 75.6%. That’s proof positive that the fund can deliver payout hikes in all market weather. Its long-term total return (including dividends) shows that resilience, too:

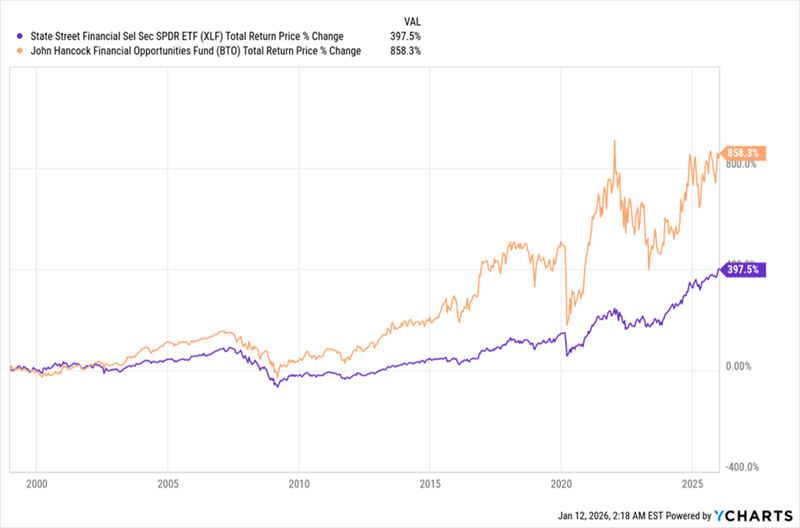

A Long-Term Outperformer

BTO (in orange above) has been around since 1994, so it’s endured the dot-com bubble, the lost decade of the 2000s, the Great Recession and the pandemic. The bottom line is that this fund delivers an income stream we can count on.

And see how much higher that orange line goes past the purple line showing the performance of the index fund in the chart above?

BTO has returned over 800% since the late 1990s, when XLF went through its IPO, while XLF has delivered less than half that. And even though BTO and XLF give you exposure to the same sector and face similar risks, BTO delivers five times the income and has returned more than double the profits.

But there’s yet another reason why we like BTO (to be honest, this is the biggest one):

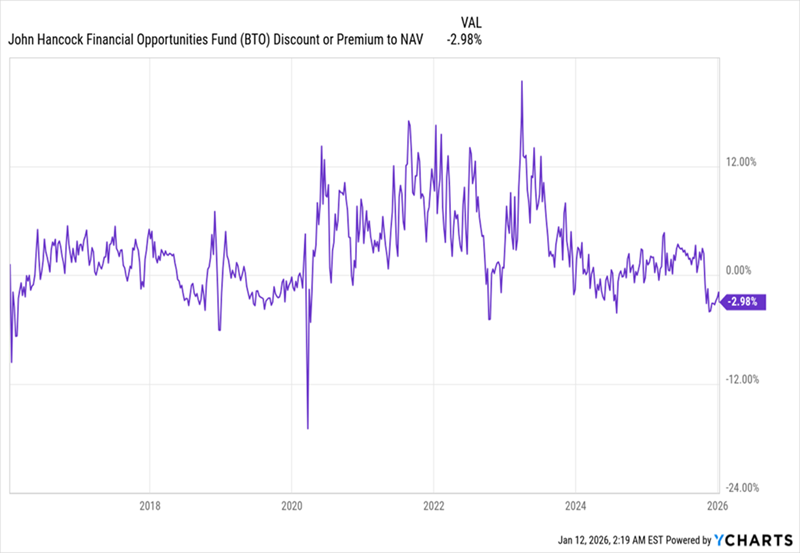

A Sudden Discount Appears

Throughout most of its history, BTO has traded at a premium to net asset value (NAV, or the value of its underlying portfolio), often a big one. That’s unusual for a CEF, but BTO delivers outperformance and a high, growing payout, so a premium does make sense here.

What doesn’t make sense is that this premium has suddenly dropped to a discount. That’s a key signal that a contrarian move into BTO is worth considering now: It gets us in on a low-profile fund (and sector) that looks set to go on a strong run.

And the discount? I don’t expect it to last as investors rotate out of pricier tech stocks and into other areas.

Buy BTO—Then Grab 60 More Dividend “Paychecks” By Doing This

My “60-Paycheck Dividend Plan” builds on BTO’s 7.2% payout by handing you 5 dividend checks a month, on average. That’s a total of 60 dividend payouts in the next year (and every year after that!).

Your average yield? A whopping 9.3%.

Kickstarting this silky-smooth 5-dividend-a-month payout plan couldn’t be simpler. Simply click here and I’ll spell it all out for you in detail. You’ll collect the first of your 60 dividend “paychecks” in just a few weeks!