I hate to hear about investors using “rules” like the 60/40 portfolio (where you devote 60% of your holdings to stocks and the rest to bonds) to invest their hard-earned cash.

The problem with “rules” like this one is that they lack the ability to adjust to changing markets, like the mess we’ve been living through this year, which has walloped stocks and bonds in equal measure.

Advisors See the Light on Oversimplified “Rules” Like the 60/40 Portfolio

It seems like advisors and the business media are finally accepting this hard truth. Recently, banks like Goldman Sachs (GS) and JPMorgan Chase & Co. (JPM) have been urging clients to shift away from the 60/40 setup, while publications like Barron’s and Kiplinger are writing articles literally titled “The 60/40 Portfolio is Dead.”

It’s great to see, but if they were really serving their clients (and readers), they’d go further and recommend our go-to income plays, closed-end funds (CEFs).

They’re a much better alternative, for a simple reason: they pay dividends that are high enough for many people to live on without having to sell a single share in retirement. Thanks to the pullback, you can easily find CEFs dishing yields north of 10% these days, while trading at big discounts to net asset value (NAV, or the value of their underlying portfolio holdings).

With your bills paid, you can sit back, collect your dividends and basically tune out the movements of stock prices, Or better still, you can use strategies like dollar-cost averaging to reinvest your payouts and “automatically” take advantage of the bargains this pullback has served up.

CEFs: Purpose-Built to Ride Out Market Storms

To explain how high-yield CEFs help investors during bear markets, let’s take the example of John and Jack.

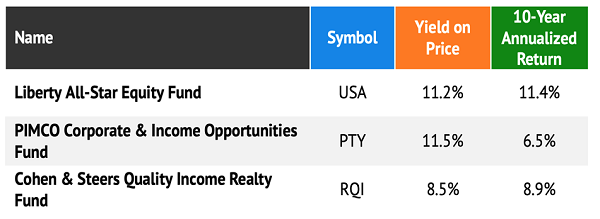

John has a 60/40 portfolio, like his financial advisor has recommended: 60% stocks, 40% Treasuries. Jack, on the other hand, has put his money in CEFs—specifically the Liberty All-Star Equity Fund (USA), PIMCO Corporate & Income Opportunity Fund (PTY) and the Cohen & Steers Quality Income Realty Fund (RQI).

This 10.4%-yielding portfolio has generated a nice 8.9% average annualized return over the last decade (even after the 2022 market decline).

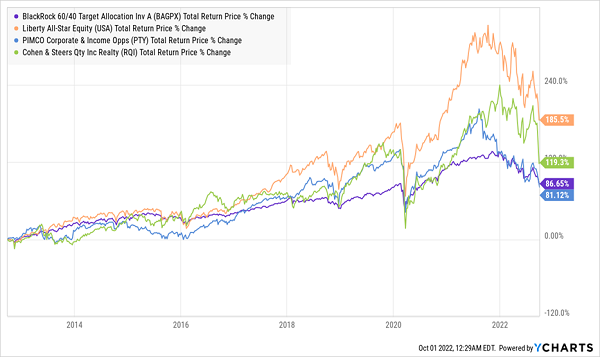

It’s also handily beaten the 60/40 portfolio (in purple below), with a 129% average total return between Jack’s three funds, versus 87% for the BlackRock 60/40 Target Allocation Fund (BAGPX), a good proxy for our 60/40 stock-bond split.

60/40 Portfolio Loses Out to 3 Strong CEFs

But what’s really important is that these funds provide a high income stream: $86.67 per month (or $1,040 annually) on every $10,000 invested, based on their current yields and payouts. Note also that their dividends continued through two of the most difficult bear markets in recent memory: the COVID-19 selloff and the 2022 volatility.

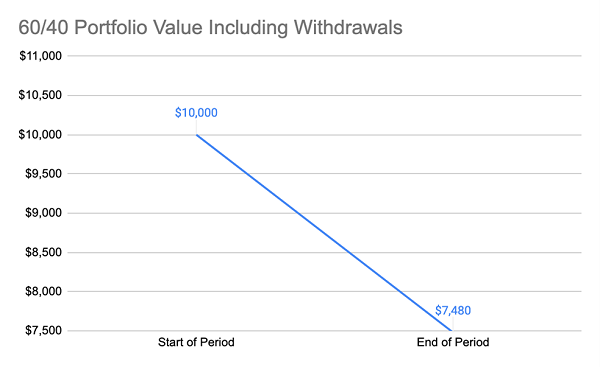

60/40 investors, on the other hand, wouldn’t have this cash cushion.

Source: CEF Insider

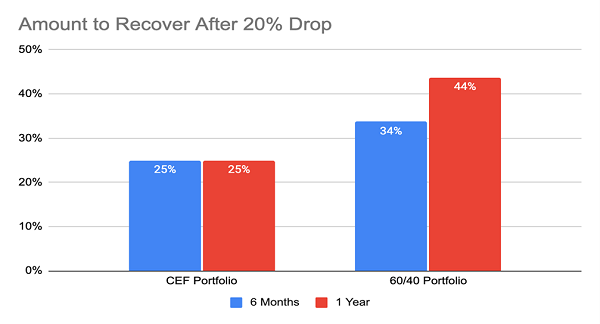

While the CEF investor has the same number of shares (and thus the same amount of potential upside) at the start and end of the period, the 60/40 portfolio has seen a major loss in value due to the 20% decline in its value and the investor’s withdrawal. This means that, while the CEF portfolio needs to gain 25% to get back to where it started before the bear market, the 60/40 portfolio needs to go up 34%.

Source: CEF Insider

The longer a bear market lasts, the worse this effect gets. Because the number of shares stays constant, a 20% drop for a CEF portfolio means a 25% recovery is needed to get back to where it started, whether we’re talking about six months, a year or longer.

But with the 60/40 portfolio, you’re actively withdrawing money from your portfolio during a bear market, so the longer the market stays down, the more you need to gain to make your initial investment whole again. So a required 34% rebound in six months turns into 44% in a year—and it gets worse the longer the decline lasts.

Of course, no one likes seeing unrealized losses in their account. But the good thing about CEFs is that their outsized income streams mean you don’t need to sell shares and make those short-term paper losses real. And you get an opportunity to reinvest your dividends if you so choose, picking up bargain-priced CEF units in the process.

Forget 60/40. Buy These 4 High-Yielding CEFs (Paying 8.5%+) Today

I’ve got 4 CEFs that are the perfect cornerstones for a “post-60/40” portfolio. They yield 8.5% on average today—easily enough to keep most people’s bills paid—and they all pay dividends monthly, too.

Plus all four trade at deep discounts now—so much so that they’re primed for fast 20%+ upside in the next 12 months! And if the markets trade flat, these 4 funds’ big discounts will help them hold their own.

And you’ll still collect their rich 8.5% dividends!

The time to buy these 4 bargain-priced CEFs is now. Click here and I’ll share my entire CEF-investing strategy with you and give you full details on these 8.5%-paying funds, including their names, tickers, current yields and discounts.