These unloved stocks yield between 6.9% and 21.4%. These are big dividends, but not the main reason we are discussing this ignored five today.

Each of these names is so unliked by the Wall Street suits that they have serious upside potential.

How could that be?

These shares are heavily sold short.

Short selling is a way to bet against a stock. To do so, one must borrow the shares and sell them today. In hopes of buying back at a lower price tomorrow.

What happens if the stock goes up tomorrow? And rises the next day? And so on?

Eventually, the short seller may “feel the heat” and buy back the shares. Which turns up the temperature on other shorts in the room—who also buy. And send the stock price on an ironic rally higher.

This is popularly called a short squeeze.

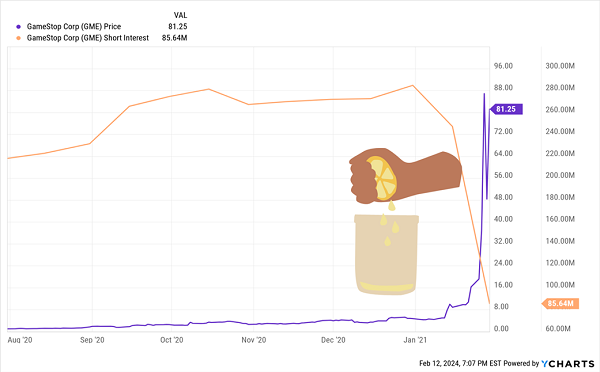

The classic example is the legendary short squeeze back in ’08 that sent shares of Volkswagen AG soaring 82% in a single day. But many newer investors will be more familiar with the wild action around GameStop (GME) and other so-called “meme stocks” a couple years back—their meteoric rises were in part triggered by heavy shorting gone awry.

As GME’s Shorts Were Squeezed Out, Its Shares Were Squeezed Higher

As contrarian investors, we have no interest in joining these herds of short sellers. We want to run the other way and consider buying stocks that are heavily shorted.

Now consideration is only the first step of our careful approach. We next need to identify where the shorts have it wrong. There is plenty of garbage floating in the stock market today. Much of it is shorted for a reason. It’s the flaws in said reasoning that interests us.

So here we go, five heavily shorted dividends ranging from 6.9% to 21.4%. They have our consideration. Next up is our analysis.

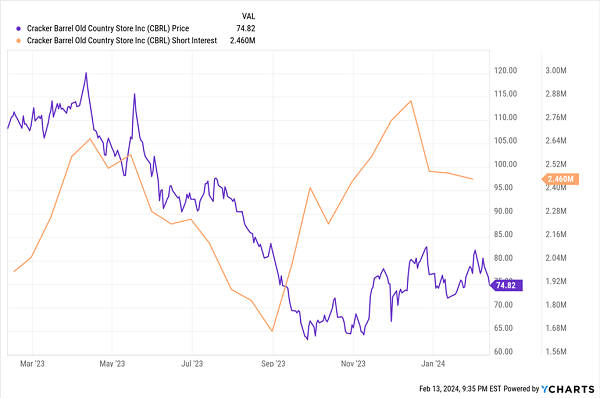

Cracker Barrel Old Country Stores (CBRL)

Dividend Yield: 6.9%

Short Interest (% of Float): 14.4%

Last April, I said investors should sell Cracker Barrel Old Country Stores (CBRL), and here’s hoping you did—CBRL shares have lost a quarter of their value since then. When I took a refreshed look at CBRL in September, I didn’t see any additional reason for optimism; shares are flat since then while the market has climbed by double digits.

Short Interest Is a Different Story

Cracker Barrel’s summer declines helped to work off previously high short interest, but the bears piled in again following a big fourth-quarter earnings whiff on revenues that barely budged. Then in late November, CBRL delivered another miss spurred by a 7.1% drop in traffic.

CBRL’s short camp has eased over the past month or so; the remaining shorts could eventually get squeezed out should several initiatives—including cost cutting and a new rewards program—bear fruit.

More worrisome longer-term is that earnings are failing to cover Cracker Barrel’s nearly 7% dividend; right now, Cracker Barrel is paying out roughly 110% of this year’s estimated profits. To be fair, CBRL has historically maintained an extremely high dividend payout ratio, but that fact won’t exactly give investors the warm fuzzies.

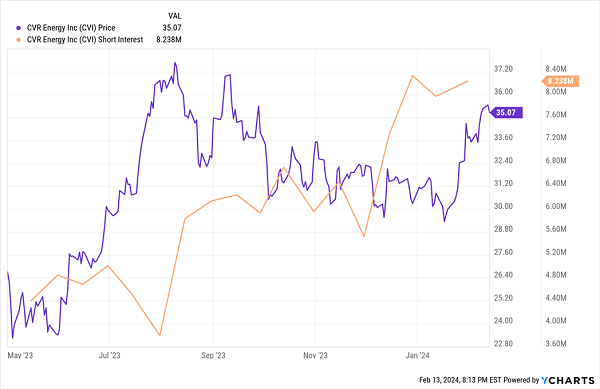

CVR Energy (CVI)

Dividend Yield: 12.8%

Short Interest (% of Float): 28.1%

Texas-based CVR Energy (CVI, 12.8% yield) deals in renewable fuels and petroleum refining, as well as nitrogen fertilizer manufacturing through its interest in CVR Partners LP (UAN).

Unsurprisingly, CVI was among the laundry list of energy firms that cut their payouts during COVID. (Specifically, CVI reduced its dividend by 50%, then suspended it entirely.) It paid a special dividend in 2021, then went to a regular-and-special formula starting in 2022. Currently, its 50-cent quarterly dividend yields 5.7%, and its special dividends over the past 12 months have added another 7.1% to that, to combine for a yield of nearly 13%.

Investors cheered CVR’s summer announcement that it wouldn’t pursue a spinoff of its UAN stake—good news, if nothing else, for the dividend. But the jump in stock price also triggered a big buildup of shorts—a buildup that continued after Carl Icahn (who still owns roughly two-thirds of all CVI stock) sold 4.1 million shares in September.

The Bear Camp Is Growing

This is a shaky situation—one that hinges not just on refined product prices, but also whether Carl Icahn’s selling was a one-off or the start of a trend. The latter could dampen any positive momentum CVI might build.

An important note about short interest: the Financial Industry Regulatory Authority (FINRA) only requires brokers to report short interest positions twice a month. So when you look at short data, you also want to see what the stock has been up to since then. The most recent data is from Jan. 31, 2024, which is a lot of time for a stock to move. CVI is up about 4% since then—not enough to suggest a significant move in the shorts in either direction.

From a longer-term perspective, though, CVI Energy might be good for a decent baseline of yield, but it’s the energy sector—the special dividends will be inconsistent at best, and disappear at worst.

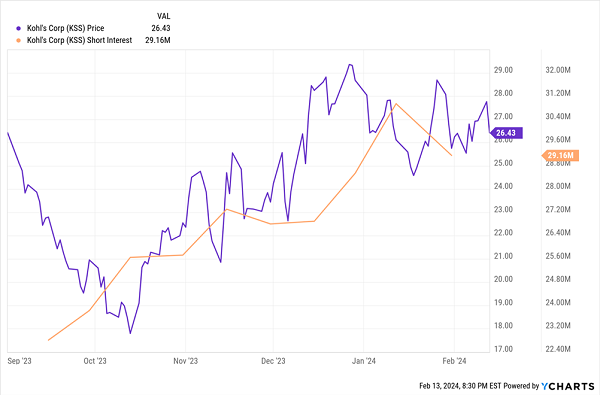

Kohl’s (KSS)

Dividend Yield: 7.6%

Short Interest (% of Float): 29.7%

Kohl’s (KSS) KSS shares are on a nearly 50% run since mid-October, which has spurred quite a buildup in short positions—currently representing almost a third of Kohl’s float.

Wall Street Clearly Doesn’t Trust This Rally

Can you blame the bears? Kohl’s is an e-commerce also-ran, a speck in the rear-view of Amazon.com (AMZN) and Walmart (WMT). At least in a roaring economy, there’ll be scraps for Kohl’s to eat—but any hint of an economic downturn will likely fray KSS shareholders’ nerves.

While 7%-yields are the norm in some sectors, they’re rare in retail for a reason. I view this high yield not as a come-hither signal, but as a warning light. Sales keep falling, as do profits. A payout ratio of 80%-plus is survivable, sure, but it severely limits Kohl’s ability to reinvest in itself.

SL Green Realty (SLG)

Dividend Yield: 6.9%

Short Interest (% of Float): 30.1%

SL Green Realty (SLG) was one of several office real estate investment trusts (REITs) on my list of sells to start 2024. Why? Because it and its brethren had been rallying hard for the better part of a year—SLG more than doubled between its 2023 lows and New Year’s—less because of improving fundamentals, and more because of falling Treasury yields.

In fact, unlike the rest of the stocks on this list, SL Green’s short squeeze might actually be in the rear-view mirror.

SLG’s 2023 Blast-Off Has Been Jettisoning the Shorts

Is there more room to run? Perhaps—short interest remains around 30%. But this is a company that in December reduced its dividend by about 8% alongside the sale of a fee ownership interest in one of its properties. And it’s expected to sell additional property interests in the year ahead. Good news for SL Green’s liquidity and its ability to pay down debt, but worrisome for anyone actually planning to retire on dividends alone.

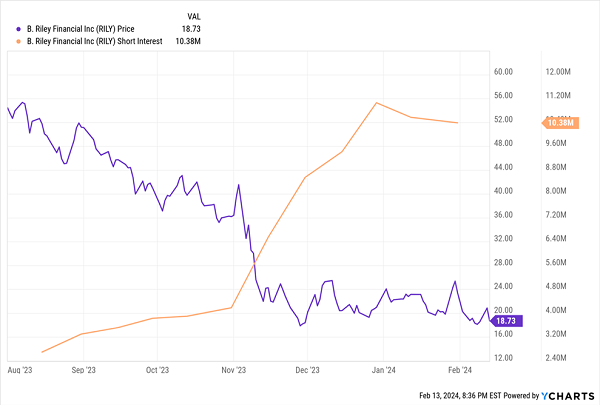

Riley Financial (RILY)

Dividend Yield: 21.4%

Short Interest (% of Float): 56.9%

Riley Financial (RILY) is a financial-services firm in a bunch of businesses, including wealth management, capital markets, consulting, and auction and liquidation. The company tends to grow by acquisition, which leads to choppy revenues and cash flows, though its $1-per-share payout has held up over the past couple years.

And it is acquisitions that have the bears knocking down RILY’s door.

Bloomberg, citing people familiar with the matter, have reported that U.S. authorities are investigating the firm’s deals with Brian Kahn, the former CEO of Vitamin Shoppe parent Franchise Group who stepped down in January amid growing coverage of his links to a failed hedge fund. As Bloomberg reported, Kahn was “an unidentified co-conspirator in a U.S. Department of Justice criminal case prompted by the 2020 demise of the Prophecy Asset Management hedge fund.”

Riley issued a statement saying it has not received anything from the SEC about the matter. Still, questions about Kahn’s relationship with B. Riley, which helped arrange a deal to buy out Franchise Group last year, paired with writedowns at the firm has sent shares plummeting by 70%.

And the Bears Are Hungry for More

While a short squeeze is always in play when more than half a company’s float is sold short, this could take a while to resolve—and even the reported investigation is in dispute. Even if you decided to wait it out, yes, B. Riley has a monstrous dividend—but its free cash is well less than what’s needed to finance it, raising questions about that dividend’s sustainability.

Give Me 4 Minutes, I’ll 5X Your Retirement Income

Riley is the perfect example of what some investors will pounce on in the name of high yield.

I don’t blame them! Soaring inflation has sent projected retirement costs to the moon, and investors are starting to get wise.

They know they’ll need fatter yields and bigger returns to keep their plans on track.

But you don’t have to sacrifice quality just to get a few more percent each year.

In fact, that’s the worst thing you can do.

Me? I suggest you get greedy.

If we want a cozy, comfortable retirement without bleeding your nest egg dry, we need to have it all. Big yields. Growth potential. A bargain price. And the ability to take macroeconomic headwinds head-on!

It sounds like a lot, but these are reasonable, realistic asks. And those are exactly the kind of traits you can find in the investments I hold in my “Perfect Income” portfolio.

My “Perfect Income” portfolio attacks retirement investing from a different angle. Rather than trying to time the market and chase trends, we target high-yield holdings (roughly 5x the S&P!) that walk their own path, no matter what the Fed, Congress or the rest of the world throws their way.

So, what makes these dividends “perfect”? Well, they have to have a few things in common:

- They DO pay consistently, predictably and reliably.

- They DO survive—and even thrive—in market crashes.

- They DO deliver double-digit returns, with safe, secure investments.

- They DO require minimal management time—just a few minutes every month!

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!