One year ago, I wrote to you that it was time to buy bonds again. The “index huggers” who only know SPY thought we were nuts for talking fixed income.

The popular narrative at the time (which aged like boxed wine) was that interest rates would rocket to the moon in order to contain inflation. Or help the government fund its ballooning deficit. Or some line of reasoning.

When rates rise, bond prices fall. Hence, the prevailing vanilla sentiment was that bonds were for bums.

We original thinkers disagreed. We reasoned—correctly—that rates fall when recession fears grow. Period. ‘Nuff said.

Our high fixed-income priest from DoubleLine, Jeffrey Gundlach, was equally sanguine in the heat of the moment. The “Bond God” advised investors not to worry about then-rising rates and instead to “Buy a T-Bill and chill.”

The T-Bills worked out fine but our contrarian twist on Gundlach’s formula worked out even better. The 10-year Treasury yield dropped from 5% a year ago to 3.7%. And bond portfolios have boomed.

Our favorite vehicle to ride this move higher? We looked past T-Bills for select closed-end funds (CEFs)—like the one run by Gundlach and his main man Jeffrey Sherman instead!

This “maraschino cherry” fund DoubleLine Yield Opportunities (DLY) (pronounced “dilly” by the Jeffreys at DoubleLine) yielded 9.5% when we discussed it last September. This mega payout was our baseline return—a nice starting point!—and nearly double the chill T-bill yields.

DLY also sold at a 4% discount to its net asset value (NAV). Which meant the Jeffreys’ hand-picked bonds were selling for 96 cents on the dollar. That was quite the deal.

The fund’s top holding features 8.41%-paying bonds from Freddie Mac. Did you get a phone call about this issuance? Me neither. The Jeffreys likely got the first ring and bought everything they wanted.

The yields from Freddie maps to DLY’s current 8.4% yield perfectly. Vanilla investors (and mainstream money managers) realized they were late to our DLY & Co. party. They have since crashed it hard, closing DLY’s discount window.

DLY has delivered 24% total returns—including dividends—since we discussed last September.

But Brett! I can hear you asking. Aren’t we worried about a recession given the gloomy jobs data and hence the creditworthiness of DLY’s portfolio?

First, I’m not worried about Freddie’s paper. As a pseudo-government agency, these 8.4% yields are not only elite but also secure. And generally speaking I trust the Jeffreys to evaluate credit.

Second, I’m not so sure we are staring down a hard landing. For fiscal 2024, the Congressional Budget Office (CBO) projects a $1.9 trillion deficit on $4.9 trillion in tax receipts. And yes, this is the CBO that paints its projections with rose-colored ink.

So, we have nearly $5 trillion in revenues and almost $7 trillion in expenditures. A 40% overshoot.

Where is the money coming from? The US Treasury is (ahem) finessing debt issuance to guide long-term interest rates lower than they otherwise would be. This “Quiet QE” is similar in flavor to the yield-curve control that Japan has implemented for many years.

The result is monetary inflation. And if the economy keeps rolling, which it may very well do thanks to an extra $2 trillion, a soft or even no landing scenario is possible.

Don’t trust me? Then keep it simple and buy US Treasuries. iShares 20+ Year Treasury ETF (TLT) and SPDR Portfolio Long-Term Treasury ETF (SPTL) pay 3.8% and 3.7% respectively. The purest play on a hard landing is plain ol’ US Treasuries with long durations.

Boring? Of course. We love boring when it comes to fixed income. Remember there are only two drivers that determine any bond’s price direction:

- Duration risk: Higher future rates are bearish for bond prices. Lower future rates are bullish.

- Credit risk: What’s the chance that the bond issuer can’t pay us back in the future?

Credit risk is not a concern with Treasuries. If Uncle Sam gets into a bind, he’ll just print more money!

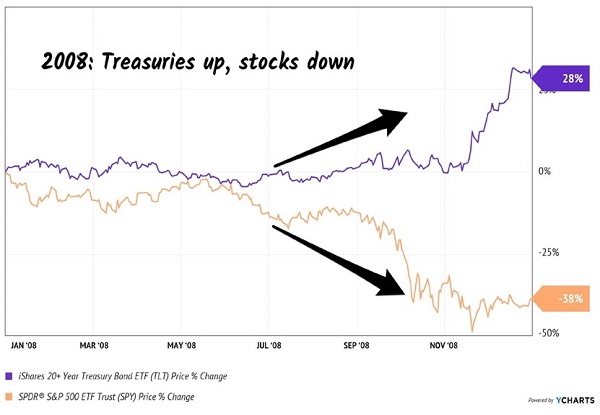

Which leaves duration risk for them, but opportunity for us. It’s why these boring funds have double-digit upside if we see a serious recession. In 2008, TLT returned 28% including dividends while the S&P dropped 38%!

Treasuries are a Hard Landing “Pure Play”

TLT has enjoyed 8.7% returns since we chatted about it last August.

While the economic outlook is uncertain, one sure thing is that bonds are back and they will see heavy trading with short-term swings between fear and greed. This is bullish for “pick-and-shovel” play MarketAxess (MKTX).

MarketAxess makes fixed-income trading tools. Bonds have traditionally changed hands via phone deals. Old school. MarketAxess brought bond trading into the twenty-first century.

Today, the company handles one out of every five bond trades. This is a “big bad” bond business. The company continues to execute, launching a new platform last year called Adaptive Auto-X, which boosted its market share nearly 5% in just a year.

When we last discussed MarketAxess in March, I made the case that the stock had 31% near-term upside. The stock has already enjoyed a 19% pop. More gains are likely as action in the bond market grows.

Did you profit from these bond trades with us? If not, why not? I hate to be blunt, but you are missing out on a historic bond bull market.

A bond bull market is an income investor’s dream. This may be the last one we see for the rest of the decade, to be honest. If you are not making these trades then you are missing the bull.

Stop sitting on your hands and start collecting monthly dividends—plus price gains—with this historic bond bull market today. Please read on and I’ll share my favorite places for fixed-income money right now.