Three years ago, I wrote to you from the La-Z-Boy in my kids’ room. Which wasn’t unusual. We were all stuck at home staring at whatever immediate family we were sheltered in place with. It was April 3, 2020.

(Ah, 2020. Family walks were the highlight of the day. Our investment strategist—and survivalist father—took no chances when leaving the house. Here’s one from the archives that recently resurfaced on my wife’s phone…)

Six packs in a stroller? The norm. What was unusual was the content of the note I penned to you before the big walk. Favor Stocks Over Bonds was the topic, strange coming from a guy who writes about bonds for a living. But heck, it was pointless to sugarcoat the case:

It’s pointless to put new money into bonds right now.

Was it ever! The 10-year Treasury yielded just 0.62%. Zero-point-six-two!

Plop a million bucks into T-Bills, and we were collecting a mere $6,200 per year. Just over $500 per month. On a million!

Investment grade fixed income paid a bit more. But we smartly avoided those yield traps, too:

Problem is, it’s tough to make a living collecting 1% or 2%. Sure, you could argue that you “win” when yields compress even more, as bond prices rise when yields fall. But c’mon, that game has almost played out.

Why had the game played out? Inflation would soon become an issue:

With Congress and the Federal Reserve each tossing around trillions of dollars at a time, you’d have to offer me an insanely high yield to get me into anything “fixed” for five, ten or (god forbid) thirty years. There’s only so many trillions you can toss around before inflation, eventually, becomes a potential issue.

Stocks would benefit from the money printing. Bonds (via the return of inflation) would not. So, we had an obvious trade to start the decade. Buy stocks, not bonds.

We should have started a hedge fund and called Michael Lewis to document our simple slam dunk trade! Stocks and two flavors of bonds (investment grade and Treasuries) have done exactly as predicted since then:

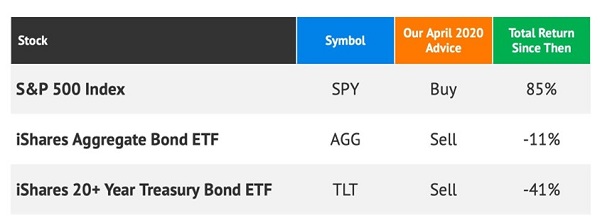

Not bad! Our buy recommendation—stocks, measured by the vanilla S&P 500—returned 85% (including dividends). Our funds to avoid, meanwhile, lost 11% and 41%.

“Safe” bond funds like iShares Aggregate Bond ETF (AGG) and iShares 20+ Year Treasury Bond ETF (TLT) paid their pittance just fine. Their yields even went up in the three subsequent years! However their portfolios were revalued lower and much lower as rates rose.

That’s the problem with fixed income. It’s great when rates are trending down. But a complete disaster when rates rise.

Ironically, income investors tend to fall in love with bonds at exactly the wrong moments. Back in April 2020, Treasuries were safe while stocks were uncertain. The herd clamored for bonds and shunned equities at exactly the wrong moment.

Fast-forward to August 2023, and we have the opposite setup. Investors want nothing to do with bonds. After all, supposedly secure TLT is down 41% in three years!

Meanwhile, stocks are back. The S&P 500 cleared important “support levels” recently. Whatever that means. It’s a hoot when advisors declare stocks “safe again” after a 20% rally. Where were these bullish calls last October?

Up 85% from my pandemic La-Z-Boy missive, I’m closing out that “trade of the decade” for a new one. Stocks are pricey and popular. Bonds are cheap and hated.

Which in Bondland brings an added bonus. Real yields!

From those sad 0.6% levels, 10-year Treasury yields have soared seven-fold to 4.2%. Now we’re talking. We’re at $42,000 on a million-dollar portfolio. More than halfway to our (admittedly lofty) 8% yield goals.

Granted, 8% doesn’t come easily. It requires research and courage to collect 8% and make sure that principal stays intact. We’re not looking for a “TLT since April 2020” type of paper tiger performance.

Speaking of which, TLT is sinking once again towards its fall 2022 lows. We called a bottom here in the pages of Contrarian Outlook, and TLT responded with nifty 9%+ returns in just three weeks. Even Bloomberg hopped on our “bond bounce” bandwagon!

When history rhymes, remember you heard it here first. And heck, if you can’t recall, just jot down our new big picture trade:

Favor bonds—and “bond proxies” over stocks right now.

My favorite bond funds to buy right now check all the boxes that we income investors love:

- They pay their dividends monthly.

- Their yields add up to 8%+ annually.

- And their prices are cheap—which means price upside, too.

I’m out of space to share the fund names, tickers and target prices here—so please click over to my website to access my Monthly Dividend Payer research now.