I know it’s only August, but I’m ready to make my first “dividend prediction” for 2024: utilities—especially growth utilities—will surge.

That means now is the time to dust off our parents’ playbook and grab these rock-steady payers before the mainstream crowd comes around. When they do, it’ll be goodbye NVIDIA (NVDA) and hello Consolidated Edison (ED)—one of the three stocks we’ll discuss below.

The Coming “Rate Rollover” Just Got Moved Up

We’re bullish on utilities now because this economy is bogging out. We got more proof of that last week, with China posting an anemic 0.8% growth rate in Q2.

You and I both know it’s likely worse than that. (Hands up if you’d wager a cent on the accuracy of Xi’s numbers!) And even though China has been a global black sheep for a while, it’s simply too big to ignore.

Truth is, China’s slowdown will weigh down growth across the globe, throwing Jay Powell’s rate hikes in reverse—and likely sooner than most folks expect.

Rate Cuts Will Electrify Utilities

To be sure, a recession isn’t great news. But we contrarians love a pullback because we want dividend deals—and it’ll throw a bevy of them our way!

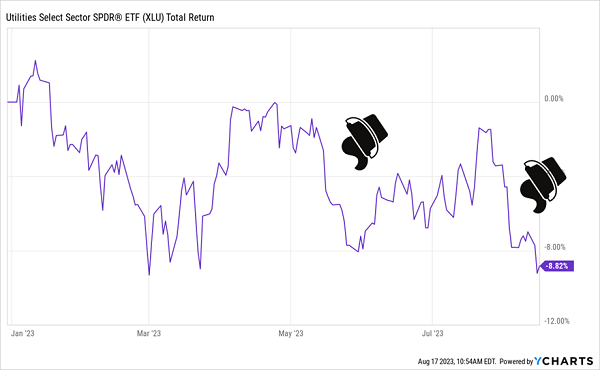

Utilities are our “early bird specials” here because they’ve been completely washed out this year, with the benchmark Utilities Select Sector ETF (XLU) down nearly 9% in a year when the S&P 500 has soared some 16%.

Utilities Lose Their Spark—Giving Us Our “In”

There are a couple of reasons for this. First, utilities carry higher debt than most firms, and rising rates increase their borrowing costs. Second (and more important), as Treasury rates rise, utilities must compete for the conservative income-seekers who are usually the sector’s biggest fans.

But the coming “rate rollover” will flip these headwinds to tailwinds for our favorite “utes.” Never mind that utilities are classic recession plays: their revenues that are all but guaranteed no matter what the economy does. With all this in mind, let’s dive into three names that should be near the top of your list:

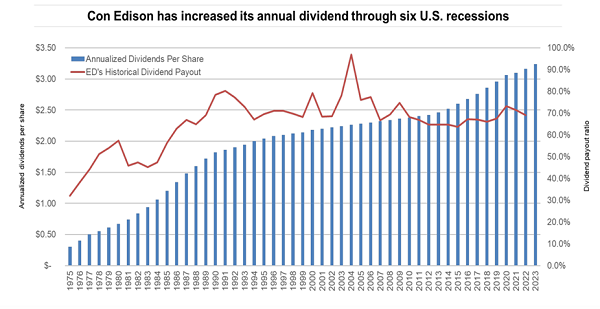

Utility Pick No. 1: Consolidated Edison (ED)

ConEd is putting on a masterclass in dividend growth, raising its payout up for 49 straight years while keeping its payout ratio (or the percentage of adjusted income paid out as dividends) between 60% and 70%. That’s above the 50% I like to see, but it’s A-OK for a utility with steady revenues like ConEd.

Source: Consolidated Edison second quarter investor presentation

The company has 3.6 million electric customers and 1.1 million gas customers in New York and New Jersey and forecasts a 6% yearly increase in its annual base rate through 2025. It’s also benefiting as New York City moves ahead with its commitment to net zero emissions by 2050.

Here’s the real standout about ConEd: after years of issuing shares—a common move for utilities to fund infrastructure expansion and upgrades—the company recently completed a $1-billion share buyback.

We love buybacks, especially when a stock is as cheap as this one, trading at just 12.8-times earnings. Repurchases boost earnings per share and speed up dividend growth because they leave management with fewer shares on which to pay out.

By the way, the stock’s pullback this year—to the tune of about 6.5%—isn’t only giving us a cheap valuation. It’s also letting us lock in a 3.6% yield, as much as ConEd ever pays.

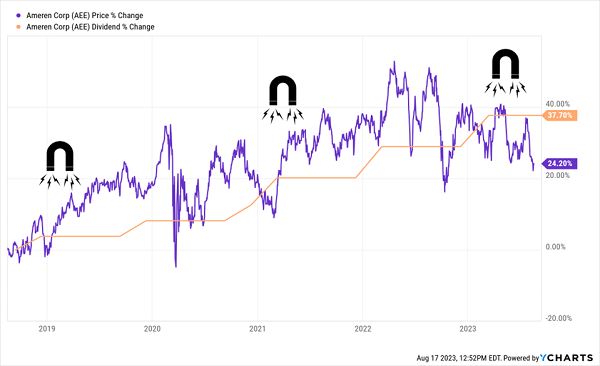

Utility Pick No. 2: Ameren (AEE)

Next time someone tells you utilities are boring, tell them about Ameren, which has 2.4 million electricity clients in Illinois and Missouri. It also has 900,000 gas customers.

This “boring” utility’s dividend isn’t just growing—it’s accelerating and taking its share price along for the ride, a phenomenon I refer to as the “Dividend Magnet”:

A “Dividend Magnet” Power Play

That’s a pretty big “tell” on where the payout—and share price—are headed. First up, we can expect the stock to reel in the dividend and take up the gap you see on the right side of the chart above. As it does, it will likely shrink Ameren’s 3.1% yield back near its 2.5% average over the last five years.

That’s reason No. 1 to give this one a look now.

Reason No. 2 is that the payout is primed to keep marching higher, pulling the share price up with it. Management said as much in its second-quarter earnings presentation, noting that it expects future dividend hikes to match up with its forecast 6% to 8% earnings-growth forecast.

Finally, Ameren is aggressively moving to cut emissions, with a goal of achieving net zero by 2045, while at the same time bringing in another 4,700 megawatts of renewable-power production by 2040. These are smart moves as the cost of renewables falls—they also keep the company on the right side of regulators.

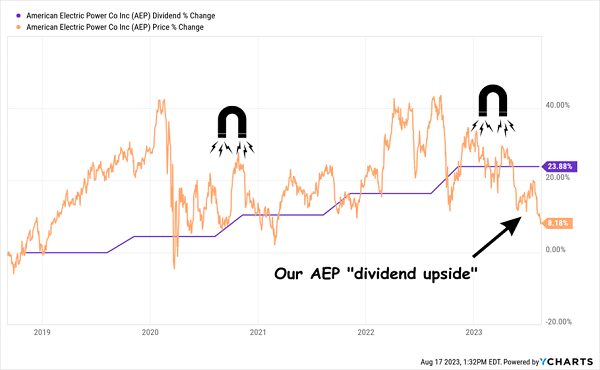

Utility Pick No. 3: American Electric Power (AEP)

AEP matches up with Ameren on a lot of levels: it, too, is calling for steady earnings growth (6% to 7% yearly in AEP’s case) with payout growth to match. And it’s leaning hard into renewables, with a goal of hitting net zero by 2045.

Where it pulls ahead is in scale—AEP boasts some 5.6 million customers across 11 states—and current yield: at 4.2%, it pays you more upfront than our other two utilities do.

And while you do lose out a bit on payout growth here—AEP’s dividend has risen 24% in the last five years, compared to 38% for Ameren—there’s more “snapback” upside with AEP, whose share price has lagged its dividend by much more in this year’s utility washout:

AEP’s Gain Potential in 1 Chart

Finally, AEP’s debt of $44 billion sounds high, but it’s a reasonable 46% of assets. And of course, lower interest rates will reduce its debt burden as these borrowings mature in the coming years. That will likely give the dividend, and the share price, an extra push.

Buy Utilities—and Add This “Perfect” Income Portfolio for Even Higher Payouts

There’s no doubt utilities are among the biggest bargains out there. With their growing “recession-resistant” payouts, they’ll be a magnet for mainstream investors—once the crowd gets past its AI “fever dreams.”

But we shouldn’t stop there. For maximum safety and income, we need to make sure we’re spreading our funds across the economy, which is what my “Perfect Income Portfolio” does. I’ve handpicked this portfolio to deliver income 4X bigger than what regular investors have to scrape by on.

It pays you consistently, reliably and predictably and is packed with overlooked, undervalued investments that are primed for upside as their ridiculous discounts “snap back” to normal.

And thanks to their broad diversification, we get peace of mind as we collect our income, too. Click here and I’ll tell you more about my “Perfect Income Portfolio” and give you access to a free Special Report naming all the stocks and funds inside.