Who doesn’t like a safe, stable utility dividend? In today’s zero-rate, VIX-spiking world, it’s a throwback to simpler times—the “old school” type of dividend we’d like to accumulate sufficiently to retire on!

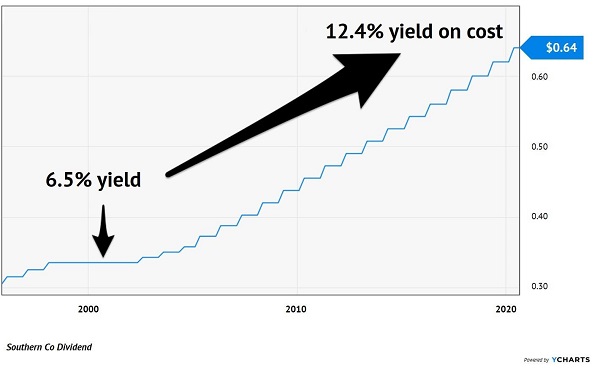

Heck, twenty years ago to this date, we could have bought shares in Southern Company (SO) and enjoyed a 6.5% yield. A $100,000 stake in Southern would have paid $6,500 every year in dividends.

Plus, regular raises were on the way. After a stagnant few years, Southern began hiking its payout every year. That 6.5% yield would eventually grow to a fat 12.4% yield on cost:

Southern’s 20-Year Yield Rise

But wait, there was more. Shares of Southern appreciated along with its dividend. And the Federal Reserve took rates to zero in 2008 (and 2020), so Southern’s yield looked even more appealing with no competition from Treasury bonds. Investors were willing to pay extra for Southern’s bond-like stock, and accept less dividend per dollar than they demanded in 2000.

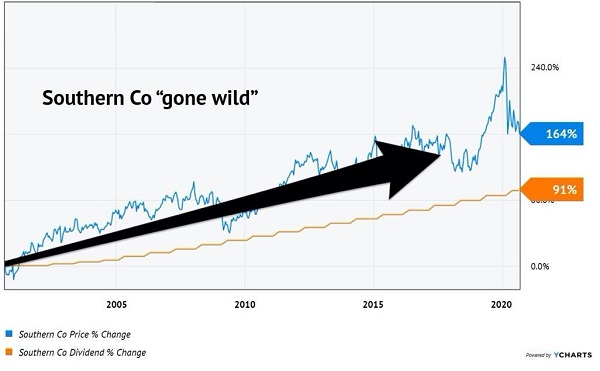

The result benefited Southern shareholders, who enjoyed total returns of 587% over the past two decades (including those sweet dividends). Which is great for them, but does it help us today?

Fast forward to today, and Southern still pays a respectable 4.8%. But a repeat of the 587% total return is unlikely, because Southern’s dividend growth has slowed to 3.2% per year. Which makes our “back of the envelope” total return math look like:

“Price appreciation per year” is essentially driven by “dividend growth” because, over long time periods, stock prices tend to rise (or fall!) along with their payouts. In Southern’s case, its price actually raced ahead of its dividend in the early 2000s and has never looked back:

A Near Dividend Double Drives 164% Growth

But it was buoyed (big time) by falling interest rates. Twenty years ago, the 10-year Treasury paid 5.8%. A yield that hefty today would crush our feeble economy!

The 10-year doesn’t have another 1% to drop, let alone five. So, we’re likely to lose this price catalyst. And while the 8% expected total return I quoted above isn’t bad, there are two ways we contrarians can do better:

- Buy a utility with a higher current yield, or

- Buy one with a dividend that’s growing faster.

Let’s start with the first method. The beauty of contrarian investing is that it is actually easier than running with the herd. Consider first-time investors who are piling into popular tech stocks had better be getting their timing right. When they pay a high multiple of earnings for a stock (or, worse, an infinite amount!), there is little margin for error.

Contrast their buys with a calculated income investors’ purchase of ONEOK (OKE), a high-quality energy “toll bridge” that has been taken down with this year’s energy collapse. The stock pays an incredible 13.6% today, and the advantage of buying a beaten down stock like ONEOK is that it merely has to “muddle through” to make us money.

When we start with a 13.6% yield that is secure, the game is ours to lose. OKE is a well-run energy pipeline firm with assets that have the potential to produce yearly earnings (defined by EBIDTA) of more than $3 billion, no matter the price of gas. Yet the company has a total market cap of just $13 billion. Cheap.

On the other end of the utility spectrum, we have a “high flying” utility such as NextEra Energy (NEE). Twenty years ago, we could have bought NextEra and collected a 3.4% yield. This was just half of what Southern paid, but it was as much as we’d see from NEE ever again.

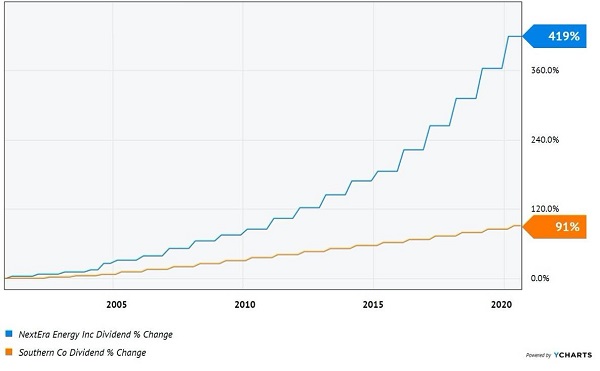

When NextEra’s dividend began to take off, so did its stock price. Its 20-year dividend growth of 419% powered total returns of more than 1,600% (from a utility!).

NextEra’s Payout Went Parabolic

NextEra yields just 2% today, but double-digit dividend growth provides income investors with a path for big returns. The firm is the largest developer of renewable energy in North America.

This is likely to remain a hot market, with much of the West Coast (sadly) ablaze as we speak. Plus, double-digit dividend raises are not an aberration for NextEra, they are the norm for this “growth utility.” Its most recent 12% dividend hike is one you can “pencil in” and add to its current yield for a nice annual total return projection:

Now, I realize you are a “show me the money” type of investor who probably prefers ONEOK’s near-14% dividend now versus NextEra’s promise of 14% returns next year. But what if we can identify dividend growers that are poised for 20% or even 25% total returns per year?

They are out there, and it is even possible to recession-proof these payers. We simply need to:

- Identify dividends that are growing by 15% to 20% or more per year, then

- Kick the business tires to make sure they can “stand up” to the pressures of a recession, and finally

- Buy them at a discount (when their dividend curves are “trailing” their prices).

It’s a tall task, and we won’t find any 20%+ total return “gifts” in the popular stock aisle. To bank recession-proof returns this size, we need to identify what I call Hidden Yields investments. Click here to learn about my top seven growth picks to snag during this current pullback.