I’ve been covering CEFs for about a decade, and I’ve never seen them get as much attention as they are right now.

And it’s only the beginning.

We talked about the much-brighter spotlight on our favorite income plays in the November issue of my CEF Insider service. Back then, we noted that big institutional investors (including the particularly aggressive folks at Saba Capital Management) were starting to pressure CEFs to change or shut down.

Shuttering a fund may sound dramatic, but the key thing to bear in mind here is that doing so can result in an immediate gain for investors.

Not to get too far into the weeds here, but because CEFs have a fixed number of shares, they sometimes trade higher or lower than the actual net asset value (NAV) of their holdings. When they trade below NAV, they trade at a discount. And if a discounted CEF shuts down, that discount vanishes instantly, delivering an immediate gain to the holder.

But even if that doesn’t happen, CEF discounts are still terrific wealth generators for us. They let us buy stocks like NVIDIA (NVDA) for, say, 13% less than if we’d bought the shares on the open market.

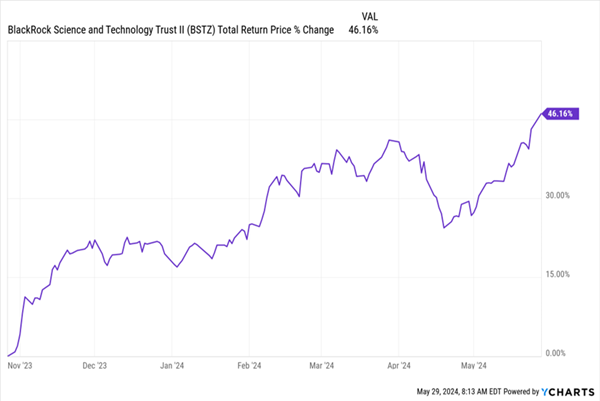

I use that stock and number specifically because that’s what was possible with the BlackRock Science and Technology Term Trust (BSTZ) late last year. The fund, which yields 12.8% currently and trades at a 13% discount, held NVIDIA as its largest position at the end of 2023 (it’s since rotated into other assets). That helped BSTZ get a bump in its performance over the last few months.

Big Tech Holdings Send BSTZ Soaring

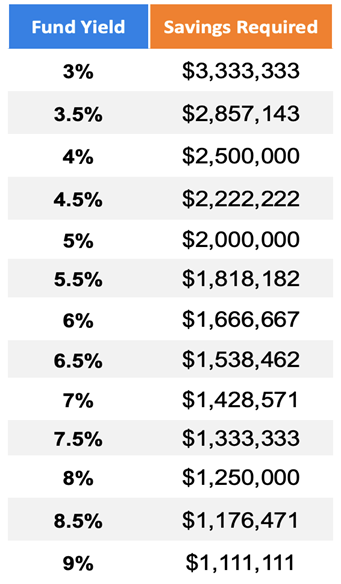

CEFs don’t just invest in stocks and other assets—they exist to translate as much profit as possible into income retirees can use. This is important because the higher your yield, the less you need to retire on. Consider the following chart to see how much money you’d need in a CEF to get $100,000 in annual income.

The higher the yield, the less you need to save, of course, so CEFs’ high income streams are really important to their (and our!) success.

Back to the folks at Saba and the other activist investors going after CEF managers. They’re already billionaires—unlike us, they don’t care about collecting big yields for retirement. So they want CEF firms to let them take over these funds and shut them down so those discounts can disappear, letting our activists book a quick gain.

The Economist, surprisingly, reported on this last month. I say “surprisingly” because CEFs usually aren’t a big enough story to get the attention of the mainstream media. So when they do get on the press’s radar, it’s worth paying attention.

However, the publication’s perspective was, well, kind of weird. For instance, The Economist notes that CEFs are destined to “lose,” as their title proclaims, since CEFs are shrinking. They write: “Critics are also winning the argument about the value offered by such investment vehicles…. Now closed-end funds are outgunned not just by mutual funds but by exchange-traded ones, too. Among the three categories, they hold just 1% of total assets.”

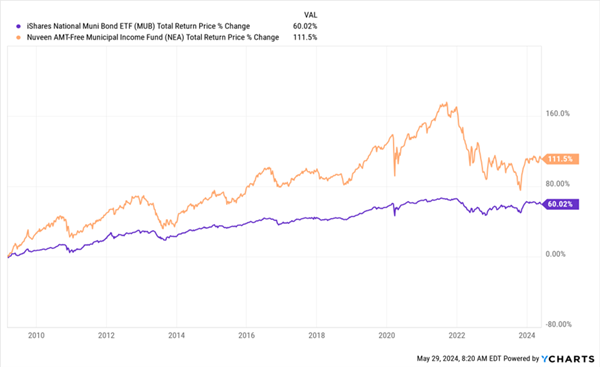

But if we hold a CEF (or any other fund), why should we care about how many other kinds of funds there are? As investors, we care, first and foremost, about making more profits and having more income. For instance, the largest municipal-bond CEF, the Nuveen AMT-Free Quality Municipal Income Fund (NEA), has outperformed the largest municipal-bond ETF, the iShares National Municipal Bond ETF (MUB), both in terms of total profits and income since stocks bottomed in the 2008/2009 financial crisis:

Muni-Bond CEF Outruns Its ETF Rival in Total Returns …

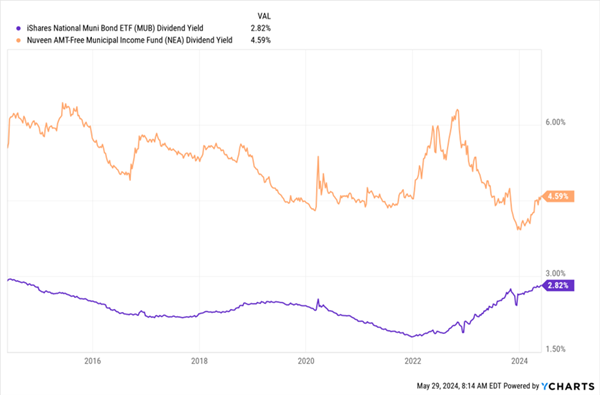

NEA shareholders have had over double the profits they could’ve gotten from the largest muni-bond ETF on the market, but they’ve also gotten higher dividends: NEA yields 4.6% now, versus MUB’s 2.8%. Moreover, NEA has yielded more than MUB throughout its history, and by a lot, too. Here’s a look at just the past 10 years:

… And in Dividend Yield, Too

I don’t want to bore you, but I could repeat this with other asset classes—stocks, corporate bonds, real estate, you name it.

So why does The Economist think CEFs are going to lose? It’s important to remember perspective. The Economist isn’t really talking to CEF investors as much as to CEF managers and the big firms that run these funds. They are correct that CEF managers are losing: They haven’t had this much pressure and attention on them in over a decade, and those are two things CEF managers hate, in my experience.

However, these are also two things that are good for CEF investors because the pressure has already forced companies like BlackRock to start lowering fees on funds, and this is just the beginning. More effort to lower CEFs’ discounts, more incentives to investors, and more profit opportunities in currently underpriced CEFs mean these funds’ yields, which average around 7.8% now, are likely to go up. And profits are set to improve as fees shrink.

Will the total number of CEFs on the market and the amount of money they manage decline? Maybe. But we as investors really don’t care, because the actual profits CEFs have to deliver as CEF managers fight off the activists are very likely to keep rising—and that’s a net benefit to those of us who invest in these high-paying funds.

Yours Now: The 4 Best CEFs to Ride the Growing “Insider Wave”

BSTZ is nicely positioned to gain as more activists target CEFs, but it is heavily weighted to tech, so it’s certainly not for everyone. But that’s okay, because this wave is going to lift CEFs across the board—especially those trading at absurd discounts.

To help you take full advantage, I’ve targeted four of the highest-yielding CEFs out there, with the deepest (and most undeserved) discounts. This quartet yields a rich 10.2% between them, and three of them pay dividends monthly, too.