Income investors love Dividend Aristocrats. And why not? These are stocks that have delivered dividend raises year after year for many decades.

But we can do even better than the Aristocrats. And get stinkin’ rich in the process by buying these payout raisers before they have clocked 25 years of divvie growth (the qualification to be an Aristocrat).

This is where the real money is made.

The problem with some Aristocrats is that their best days are behind them. When a company reaches a level of dividend maturity, payout ratios can get bloated, and payout increases can become incremental and tied to a company’s modest profit growth. Let’s consider the most recent hikes from this group of Dividend Kings (Aristocrats with 50-plus years of dividend growth.)

Instead, we might do better to target companies a little earlier in their dividend-growth arcs. Take Fastenal (FAST), for instance. Fastenal is one of the newest Aristocrats, joining in 2024 after reaching its 25th year of payout growth earlier this year, just before the S&P 500 Dividend Aristocrats’ annual reconstitution.

Had an investor bought Fastenal a few years before it joined the Aristocrats, they would’ve enjoyed a roughly 81% jump in the dividend over a five-year period—that’s 12%+ annual income growth!

The Dividend Magnet Pulls Fastenal Higher

That’s a lot better for our retirement fortunes than token 1% raises.

Let’s see who’s on deck for Aristocracy to see if they can produce similar price pops now:

Nike (NKE)

Dividend Yield: 1.6%

Consecutive Dividend Increases: 21 years

Nike (NKE) is a global leader in athletic footwear, apparel, accessories and equipment. It operates in 190 countries, selling gear not just through its namesake brand, but also the Jordan and Converse brands.

Most people are aware that Nike is a font of growth, more than doubling its sales in a decade, from about $25 billion in 2013 to a little more than $51 billion last year. Profits have doubled too, from about $2.5 billion to $5.1 billion in that time.

What most people might not realize is that Nike is a longtime dividend payer.

Nike actually began distributing cash as soon as the company went public in 1985. But the company didn’t start its current run of uninterrupted dividend growth until the early aughts.

Its dividend-growth rate has been downright torrid in recent years. The payout has tripled over the past 10 years and improved by 68% (11% annually) since 2019. But while the dividend magnet has largely been working for some time, shares have disconnected over the past couple years.

Why Did Nike Lose Traction?

There’s been no single golden bullet—Nike has been hit on several fronts. Supply-chain issues. Slowing consumer spending. A delayed China recovery. Competitors eating market share in running products. Its split with Kyrie Irving, whose shoes are now being produced by Chinese sportswear brand Anta. All of this has triggered a three-year restructuring and streamlining plan.

As a clothing and gear name, Nike will always be a more cyclical play than a typical Dividend Aristocrat. Its commitment to still-robust dividend hikes shows the company isn’t panicking over its shorter-term issues.

Lockheed Martin (LMT)

Dividend Yield: 2.7%

Consecutive Dividend Increases: 21 years

Lockheed Martin (LMT) is one of the world’s biggest and best-known defense contractors, designing and manufacturing a wide array of products through its Aeronautics, Missiles and Fire Control, Rotary and Mission Systems, and Space segments.

Lockheed is the name behind Black Hawk helicopters, F-16 Fighting Falcon and F-35 Lightning II military jets, and Javelin missiles. But it’s also responsible for technologies such as the Aegis Combat System, firefighting intelligence and the Integrated Crisis Early Warning System (ICEWS) program—a system designed to “monitor, assess, and forecast national, sub-national, and internal crises.”

While defense views might vary from one president to the next, U.S. defense spending is in a decades-long uptrend that has set all-time highs over the past three years. That has not just meant a Street-beating return for shareholders over the past decade or so, but much bigger dividend checks.

Lockheed’s Dividend Magnet Is Humming Along

Over the past five years, LMT’s payout has grown by 43%, or 7.4% annually. That’s not a red-hot clip, but it’s enough to produce a “dividend doubler” every decade. Lockheed still pays out less than half of its profits, too; with continued profit growth, this should be a sustainable rate.

Qualcomm (QCOM)

Dividend Yield: 1.6%

Consecutive Dividend Increases: 21 years

Qualcomm is one of the world’s largest communications chipmakers, providing critical technology for 3G, 4G and 5G smartphones, laptops, vehicles and more. These chips power wireless voice and data communications, networking, computing, multimedia, and position location, among other functions.

While people talk about “the next Tesla” or “the next Amazon,” they never talk about “the next Qualcomm,” but they should—the company has delivered total returns of more than 50,000% (not a typo!) since its 1991 IPO, which is 20 times better than the S&P 500 over that time.

The dividend, which was initiated in 2003, has been prolific in its own right.

More recently, QCOM has upped its dividend by 37% (6.5% annually) since 2019, which is a perfectly fine rate. And given that Qualcomm’s payout ratio is just a bit over 40%, Dividend Aristocracy is well within its means and its sights.

But it’s at least worth noting that Qualcomm has at least one black mark on its record. It actually failed to raise its quarterly payout in 2019 following a brutal fiscal 2018 that saw the company lose nearly $5 billion. However, because Qualcomm raised the payout in the middle of the previous year, 2019’s annual dividend was still higher than 2018. A raise in 2020 helped Qualcomm continue its streak, keeping it technically eligible for eventual membership in the Aristocrats.

Also: QCOM’s Magnet Effect Isn’t as Clean as Other Almost-Crats

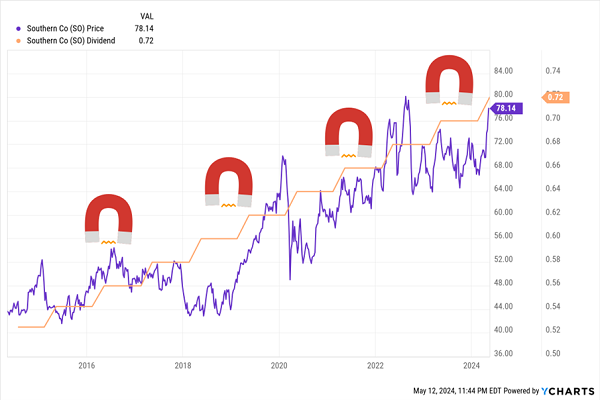

Southern Co. (SO)

Dividend Yield: 3.7%

Consecutive Dividend Increases: 23 years

Southern Co. (SO), which is two years away from qualifying for the Dividend Aristocrats, is one of the largest and most noteworthy utility stocks on the market.

The Atlanta-based utility, through roughly a dozen subsidiaries, provides electric service in three states, gas service in four states, and distributed energy and fiber optic/wireless communications services across the country. All told, the firm boasts roughly 9 million customers.

To its credit, Southern’s dividend magnet is alive and well, but it only has so much to work with.

SO’s Dividend Is Pulling Shares Higher, But at Roughly Half the Pace of the Broader Market

I don’t look at Southern much—the last time was in 2020. And that’s largely because what was true then remains true today. While Southern’s respectable yield is typical for a utility, so too is its leisurely rate of dividend growth.

While the tempo has picked up a hair since then, the dividend’s five-year growth of 20% still comes out to a modest 3.7%. Considering SO’s payout ratio is already above 70%, I don’t expect that pace to quicken.

Eversource Energy (ES)

Dividend Yield: 5.0%

Consecutive Dividend Increases: 24 years

The closest stock to Aristocracy is Eversource Energy (ES), which needs one more year’s worth of growth under its belt to join the Dividend Aristocracy. Eversource provides electric, gas and water to 4.4 million customers in the New England states of Connecticut, Massachusetts and New Hampshire.

Like Southern, Eversource Energy (ES) has a nice yield, but it also has grown the dividend at a much better clip—more than 33% over the past five years, or roughly 6% annually. And yet …

Eversource’s Dividend Magnet Has Powered Down

True, a payout ratio of roughly 80% is signaling the potential for leaner dividend growth going forward, but that’s not why ES shares have fallen off a cliff of late.

While higher interest rates have weighed on the utility sector in general, Eversource shareholders have suffered acutely amid struggles with the company’s wind-energy initiatives, which the company finally decided to exit in 2023. The final project sales were announced in February 2024, but the damage has been done. ES has absorbed nearly $2 billion in impairment charges within the past year.

If there’s any upshot, it’s that Eversource shares’ forward P/E has dipped into the low teens, well below their five-year average and the utility sector median.

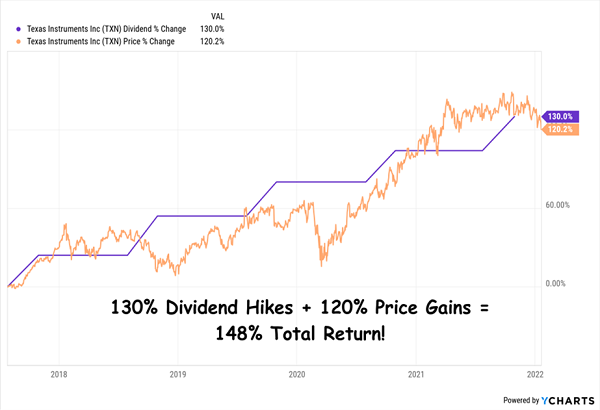

My System Produced Fast 57% and 148% Gains. Here Are Its Next 5 Winners

These future Dividend Aristocrats might be a mixed bag, but I’ve identified five dividend-growth winners that are forecast to deliver 15%+ annual returns going forward.

By tracing the connection between dividend growth and share-price growth, I’ve uncovered gain after gain for my readers.

Including Texas Instruments (TXN), whose dividend marched 130% higher during our holding period, driving a 120% jump in the share price!

We Rode TXN’s Dividend Magnet to a Massive Gain …

Add dividends and those share price gains together and you get a 148% total return!

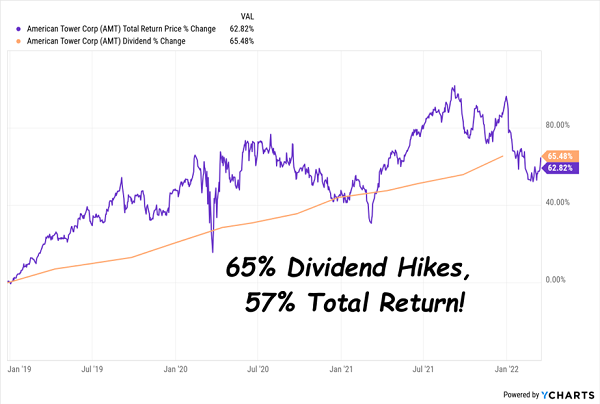

Or American Tower (AMT), whose payout rose every quarter in the little more than three years we owned it, from November 2018 to March 2022, ultimately soaring 65%.

The share price? It soared 54%, resulting in a 57% total return!

… And American Tower’s, Too

Now I’ve zeroed in on my NEXT five Dividend Magnet winners, and I can’t wait to show them to you.