I love passive investing—but not for the reason you might think.

I love it because, as I’ll demonstrate in a moment, it’s caused plenty of stocks to become mispriced, creating opportunities for active stock pickers who do their homework.

This makes the market more of a meritocracy: the people who work harder, smarter and spend more time and energy on their investments can get a higher return than those who buy index funds like the Vanguard Total Stock Market ETF (VTI) and call it a day.

Why?

Because the more people buy VTI and other index products, the more they drive up the prices of all the stocks in that index. And since these indices aren’t weighted toward any valuation metrics, that means pricier stocks get just as much of a price boost as cheaper ones.

This is madness when it comes to the S&P 500, but it gets even more insane as we drill down into specific sectors, where expertise can yield a superior return. This applies to all industries, no matter how predictable they are.

Take utilities. You might think any utility is like any other, since all of them deliver energy, have a commoditized business model and have no real marketing opportunities. Yet even here, you can buy a select few utilities and get a far superior return.

To prove my point, I’m going to compare the returns of an active utility investor to those of a passive investor.

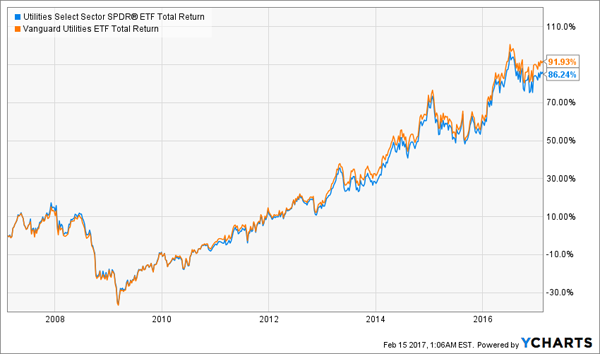

To get exposure to utilities without choosing one company over another, the passive investor would buy either the Utilities Select Sector SPDR ETF (XLU) or the Vanguard Utilities ETF (VPU).

Here’s how both funds performed over the last decade, with dividends included:

Utility ETFs Turn in Gains

Passive investors hate fund fees more than anything else, usually because they misunderstand how these fees work. So passive investors who choose VPU will crow that this fund’s lower fees (0.1% versus 0.14% for XLU) resulted in a superior return. And it’s true—$100,000 in VPU would have earned $5,690 more over the last decade, or about $47 a month.

I say let the passive investors crow about their low fees—they’re missing the bigger picture.

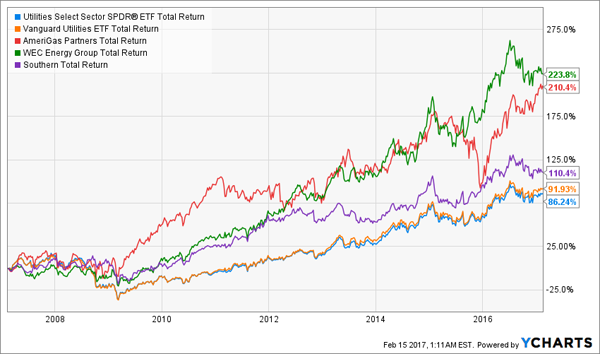

Because with a bit of analysis and research, I would instead choose AmeriGas Partners (APU), WEC Energy Group (WEC) and Southern Company (SO). At Contrarian Outlook, we have recommended these as outstanding utilities plays in the past, although they’re less obvious buys now that the market has figured out what we’ve been saying for a year.

Here’s how they performed over the last decade:

A Little Work Goes a Long Way

With a portfolio of these stocks, we would get utilities exposure and diversification, but our $100,000 initial investment would also have returned more than $159,000 in the last decade, or a profit that’s $61,000 higher than if we had just bought VPU.

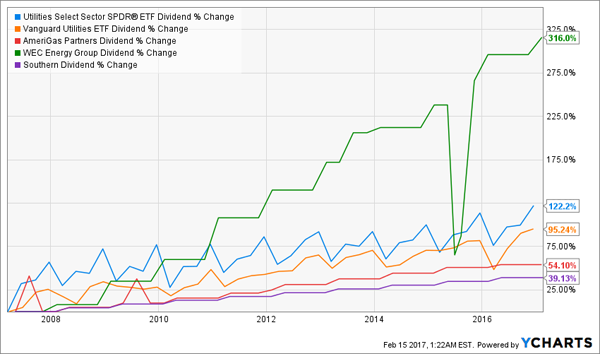

That’s not all. Not only are we getting more profit, but our average dividend growth of 136.4% is also much higher:

Strong Payout Growth

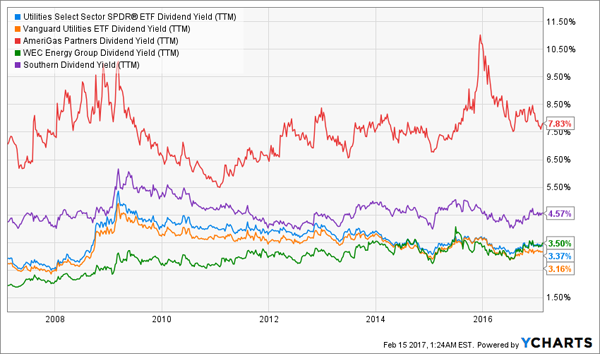

And our average dividend yield is about 60% higher than that of the passive funds:

Juicy Dividends

If selecting outperformers gets you more income, a bigger profit and higher dividend growth, why does anyone choose passive indexing?

To answer that question, we should explore the psychology of the average passive investor.

Passive indexing has surged in popularity since 2008, in part due to headlines about hedge funds underperforming. That makes it seem like active investing doesn’t work anymore (even though this data is cherry-picked and ignores fund titans like Warren Buffett, Jeff Gundlach and Carl Icahn, who still regularly outperform the market).

On top of that, memories of losing a lot of money very quickly in the dark days of 2008/09 are still fresh in many people’s minds, so they see passive indexing as the safer option.

Of course, they’re wrong. Passive investors tend to forget that the S&P 500 used to include Sears Holdings (SHLD), Radio Shack and Lehman Brothers. They also probably don’t know that the turnover rate of companies leaving the S&P 500 is at its highest level in history and is expected to grow. That means more volatility and less reliability in the index.

Then there’s the laziness factor; a lot of people just don’t want to spend time doing the research to choose winning stocks and funds.

Those of us who aren’t lazy owe these people a big debt—they create market inefficiencies (like the one I showed you above) that we can profit from.

A Set-It-and-Forget-It Retirement Portfolio You Can Count On

And yes, there is still a way you can have the best of both worlds: outsized returns without the need to spend hours researching stocks … but it doesn’t involve ETFs.

Instead, you want to focus somewhere else entirely: dividends.

Specifically, you want a portfolio that hands you a safe 8% a year like clockwork. That’s the magic number you need to collect a tidy $40,000 in income on a $500,000 investment—enough for many retirees to pay their bills with dividends alone.

That means you won’t have to worry about what stock prices are doing because you won’t have to sell a single stock to generate cash flow.

This is where our “No-Withdrawal” retirement portfolio comes in. It’s home to 6 potent high yielders investors too often ignore as they rush into overhyped dividend ETFs.

That’s too bad for them, but great for us, because it lets us scoop up these 8%+ payers at a bargain. Click here and I’ll give you the names of all 6 of these off-the-radar income plays and our complete strategy now.