“Hey Brett, what do you think of telecom?”

“Well, let’s take Verizon (VZ). It pays a 5% dividend. It’s growing that dividend by about 2% or so per year. So I’d expect the stock to return 7% or so in the years ahead,” I replied.

“What about profitability metrics like return on invested capital (ROIC)? Or margins? Or…?” my investor friend rebutted.

“If it doesn’t flow through to a higher dividend, then it doesn’t really matter.”

I was “grilled” with many thoughtful dividend-related questions while speaking to subscribers and fellow income hounds at Denver’s AAII (American Association of Individual Investors) chapter last week. One popular question was what I thought of a popular dividend stock – like Verizon, or AT&T (T), or Philip Morris (PM).

I explained that it’s actually pretty easy to project the future returns for any dividend payer.

How to Forecast Returns for Any Dividend Payer

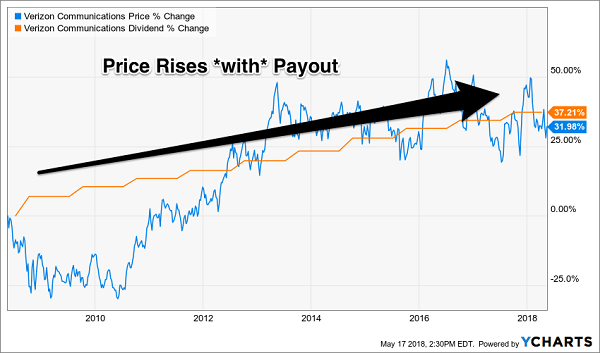

If you told me 10 years ago that Verizon was going to boost its dividend by 37% over the next decade, I’d have told you that the stock’s price would rise by that same amount. I wouldn’t have been far off – it rose 32% (not bad for a decade-long forecast):

Dividend Up 37%, Price Up 32%

(Shortly, we’ll discuss how to predict dividend growth. For now, let’s get back to this example.)

The steady staircase of Verizon’s payout (orange line above) sure makes its price (blue line above) look manic. There were months and even years where the share price shot well above and later plunged below the stocks “dividend curve.”

But over time, the payout acts as a magnet. It simply pulls the stock price back to it. Investors buy Verizon for its dividend – which means that it is likely to underperform when its yield is low (on a relative basis) and outperform when its yield is high.

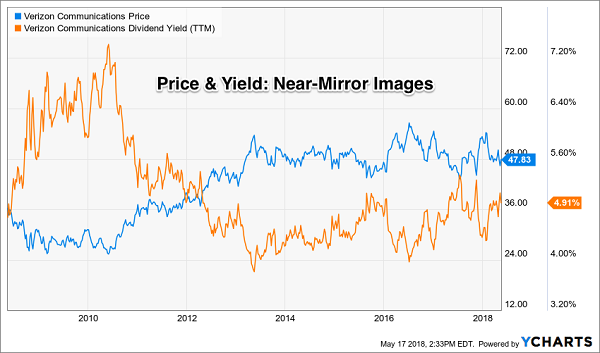

We can see this clearly by looking at Verizon’s yield versus its price history. They are near-mirror images of each other:

When Yield is High, Price is Low

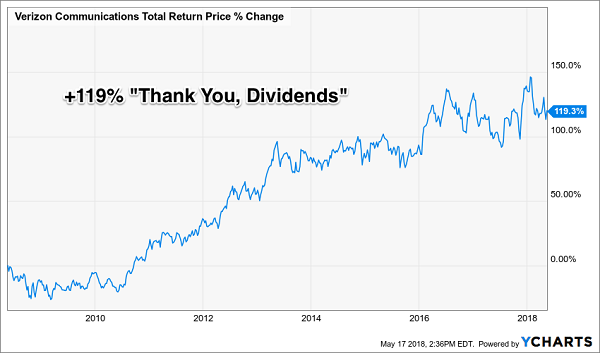

Of course Verizon investors didn’t only receive price gains since 2008. Most of their returns came in the form of cash dividends. The stock actually pays exactly the same today as it did on this date in 2008 (4.9%). But Verizon investors more than doubled their money during that time period, thanks to dividends:

Verizon Doubles, Thanks to Dividends

What will VZ shares return over the next ten years? It’s a pretty simple formula:

5% Current Yield + 2% Dividend Growth = 7% Total Returns Per Year

Can shares beat these projections? They can, but only if the company is able to accelerate its dividend from here.

This is where our “second-level” dividend analysis comes in. We need to look past the obvious metrics such as stated yields and paper profits to identify “inflection points” in payouts. In other words, we need to find the disrespected dividends – and buy them.

Interest rate worries are helpful here. Over the past few years, they’ve sent more solid dividends to the bargain bin that most other headline fears combined. Let’s talk about an obvious win that was available thanks to these concerns.

A Reliable 8%+ Payer Produces Double-Digit Gains Every Year

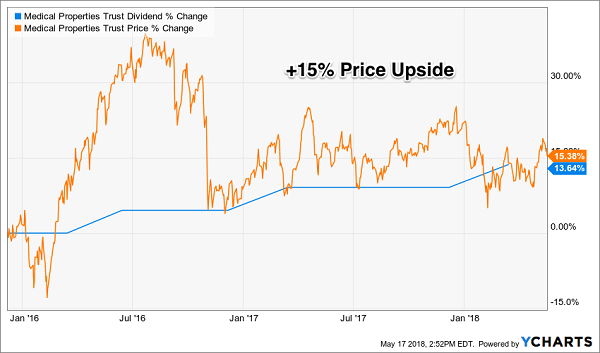

Two-and-a-half years ago my Contrarian Income Report subscribers purchased Medical Properties Trust (MPW), the ultimate “hospital landlord.” It was paying nearly 8% at the time – discarded to the bargain bin because the first-level types fretted that higher rates would harm its ability to collect rent checks from its hospital operators.

Those fears were silly. MPW continued to “play Monopoly” in the hospital space, acquiring more and more valuable assets. Its higher rent income helped it generate higher and higher funds from operations (FFO) – which it then paid to us in the form of three dividend increases:

MPW Rises 15% Thanks to 3 Dividend Increases

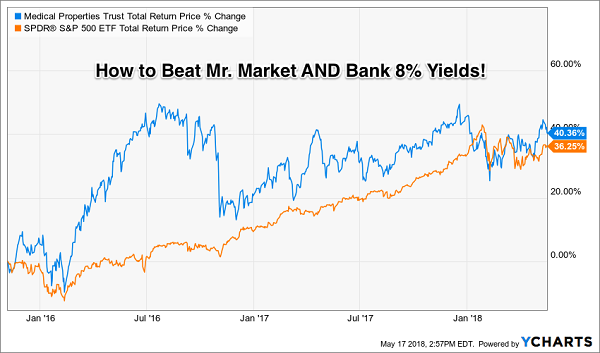

And here’s where it gets better. Not only is MPW growing its dividend faster than Verizon, but it also pays nearly double the popular telecom. Once again it paid to be contrary and buy a perfectly safe, solid stock that the mainstream media simply hadn’t heard of. We banked the capital gains above plus 7% to 8%+ yields along the way, resulting in 40% total returns that beat the broader market to boot:

Have Your Big Yield and Beat the Market!

Who says we can’t have yield and growth? We can easily have both – when we look beyond the brand name dividends and buy the underrated payers.

Like These Plays: The 8 Best 8% Dividends with Big Upside to Buy Today

Most Wall Street spreadsheet jockeys say we investors can’t have both the income and safety of bonds and the upside of stocks. We have to choose, or allocate, or whatever.

They’re wrong. They don’t realize that the nine bond funds in my Contrarian Income Report portfolio have delivered average annualized returns of 23.9% (including dividends)!

My three top picks today are poised to continue the tradition. These funds are a cornerstone of my 8% “no withdrawal” retirement strategy, which lets retirees rely entirely on dividend income and leave their principal 100% intact.

Well that’s not exactly right. Their principal is more than 100% intact thanks to price gains like these! Which means principal is actually 110% intact after year 1, and so on.

To do this, I seek out closed-end funds that:

- Pay 8% or better…

- Have well funded distributions…

- Trade at meaningful discounts to their NAV…

- And know how to make their shareholders money.

And I talk to management, because online research isn’t enough. I also track insider buying to make sure these guys have real skin in the game.

Today I like three “blue chip” closed-end funds as best income buys. And wait ‘til you see their yields! These “slam dunk” income plays pay 8.5%, 8.7% and even 8.9% dividends.

Plus, they trade at 10-15% discounts to their net asset value (NAV) today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat… and we’ll still collect those fat dividends!

If you’re an investor who strives to live off dividends alone, while slowly but safely increasing the value of your nest egg, these are the ideal holdings for you. Click here and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my three favorite closed-end funds for 8.5%, 8.7% and 8.9% yields.