Railroad stocks are set to roll and we’re going to climb aboard with two stocks—including one that’s hiked payouts by 50% in five years—we’ll delve into in a sec.

What’s driving this opportunity? Our usual contrarian mix of overlooked growth and stocks that have been tossed overboard, of course!

Since the days of the Wild West, railroads have been the backbone of the US economy, so when economic growth gets out of sync with railroad stocks’ prices—as is happening right now—we need to take notice.

As I write this, the US economy is still in growth mode and shoppers are still spending. First-quarter GDP gained 1.4% and consumer spending rose 1.5%. Those are “goldilocks” numbers: not too hot, not too cold.

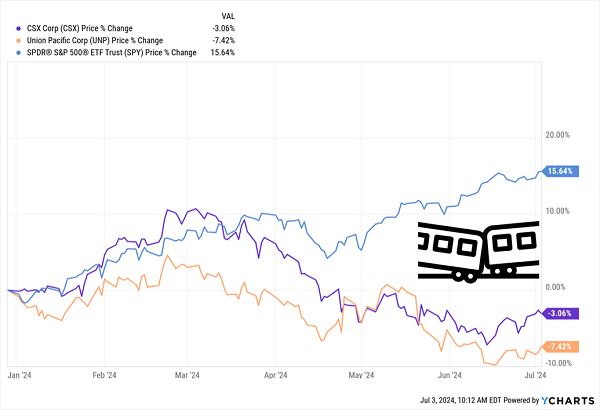

In a setup like that, you’d expect railways to at least pace the market, right? Wrong! Look at the share prices of the two railways we’ll delve into today—Union Pacific (UNP) and CSX Corp. (CSX).

Both have been derailed (sorry, I couldn’t resist) this year as the S&P 500 grabbed a full head of steam:

CSX, UNP Run Behind Schedule

If you needed any proof that this market has largely been powered by NVIDIA (NVDA), Microsoft (MSFT) and the other AI darlings, well, this is it.

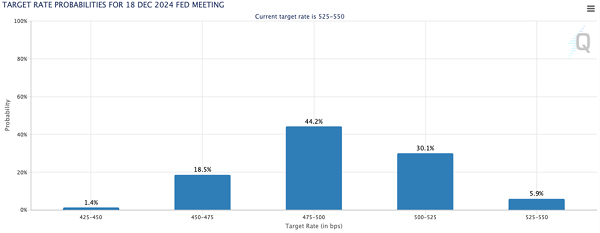

Here’s the other thing about railway stocks: The Fed has our back on these economic bellwethers. If those “goldilocks” economic numbers we just talked about start to fade, Powell & Co. will cut rates, reinflating consumer spending—and by extension giving an assist to the railways that ship the goods buyers are after.

Futures traders have already baked this in, calling for two rate cuts by year-end, with nearly 20% of them forecasting three.

Source: CME Group

“Tariff Wars” Are an Underappreciated Boon for Railways

So far, then, we’ve got three factors underpinning railroad stocks now:

- “Goldilocks” economic numbers

- Lagging railroad stocks, and …

- Coming rate cuts.

Let’s add one more: The ongoing tariff wars, which are likely to roll on no matter who wins the White House. That will continue to send manufacturers back to American shores, prolonging a shift that’s been playing out for years now.

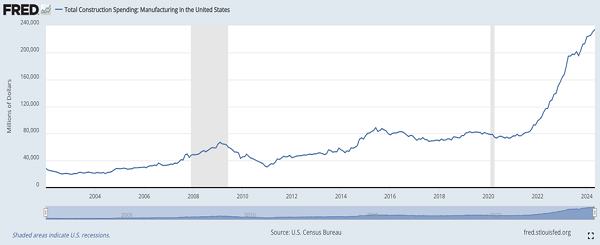

I know, I know. Plenty of people have paid lip service to this trend. But the numbers behind it are nothing short of astonishing:

The US Factory Boom in 1 Chart

The total spent on new plants in the US hit a record annual rate of $234 billion in the 12 months ended in March, and that number continues to soar.

And the railroads—classic “pick-and-shovel” plays on this “onshoring” trend—are set to benefit. (“Pick-and-shovel” refers to the California Gold Rush, in which the businesses that sold miners picks, shovels and other supplies made the real money, not the gold-panners themselves.)

Now let’s delve into CSX and UNP, which, between them, span the country, with CSX’s network covering the East and UNP dominating the West.

CSX: A Pick-and-Shovel Play on, Well, Pretty Much Everything

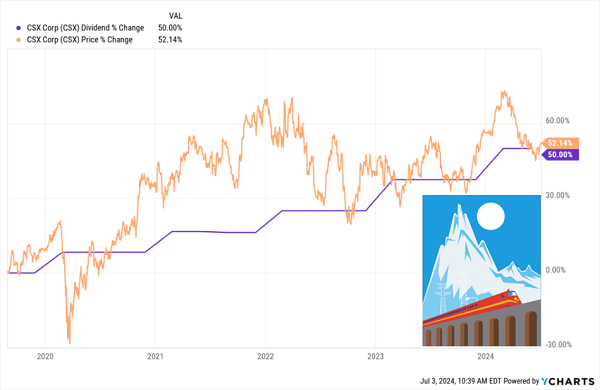

Let’s start in the East, where CSX yields just 1.4%, right around the S&P 500 average. But the stock is far from average on the dividend-growth front, with a payout that’s popped 50% in just the last five years.

That’s driven up the share price in lockstep—yet another case of our “Dividend Magnet” in action:

CSX’s Dividend “Engine” Keeps a Steady Speed

I see that pattern continuing as rising domestic demand (through our three-way combo of economic growth, rate cuts and the factory boom) boosts CSX’s volumes, which rose 3% in Q1.

More dividend fuel? CSX paid just 29.5% of free cash flow (FCF) as dividends in the latest 12 months. In other words, it could drop a substantial payout hike tomorrow and still be below 50%. So we’ve got some baked-in payout (and by extension share-price) growth here, even if business goes through a soft patch.

Management emphasized the factory boom in its first-quarter earnings report, and it’s easy to see why: According to CSX, its customers brought 100 new projects online in the 12 months ending in March, and they have 500 more in the pipeline.

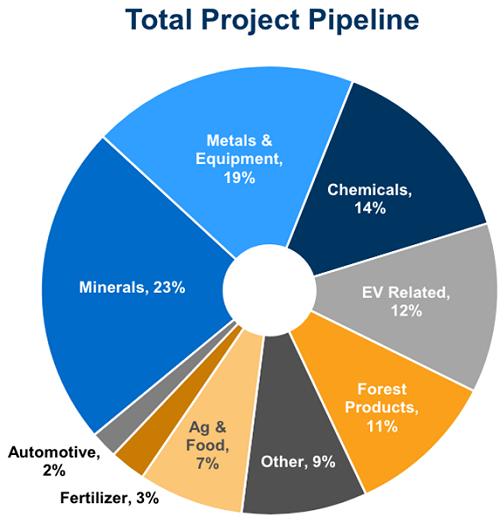

As you can see below, metals, minerals and chemicals account for a big slice of those future projects, but the EV portion is growing, making CSX a “pick-and-shovel” play on the energy transition, too:

Source: CSX Q1 investor presentation

When analyzing railways, it’s always worth looking at the operating ratio—a key metric for the sector (operating costs as a percentage of revenue, the lower the better). But we need to look at it the right way.

For example, many folks would look at CSX’s 63.2 and pass it by in favor of UNP, which is more efficient at 60.7. But that gap actually leaves CSX management more room (not to mention motivation!) to boost efficiency, and with it profits and dividends. Possible moves could include cutting costs and leveraging new tech, like AI, which could, for example, bring about better timing of railway signals.

UNP: An Overdue Dividend Magnet

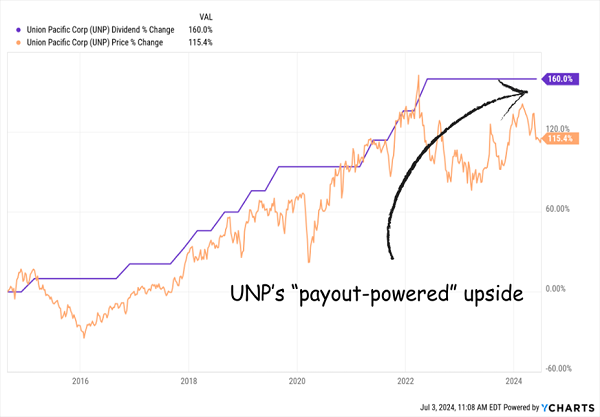

UNP, like CSX, stands to gain from lower rates, and it does start us off with a higher 2.3% yield. But our dividend picture is a little different here.

As you can see below, UNP’s dividend growth has been stuck on the platform for a couple years. But the stock is still well behind the payout’s rise, and as you can see in the chart below, it always closes the gap. So we’ve already got strong upside baked in:

UNP’s Dividend and Share Price Come Unhooked

What does the future hold for the payout? UNP paid 63% of its last 12 months of FCF as dividends, which sounds high, but as with the operating ratio, we need to look a bit deeper.

For one, that figure is trending the right way, after peaking around 66% in the third quarter of 2023. As demand (and shipping volumes) build, I see it moving back to its five-year average of 52%. That would tee up more hikes, giving the stock an extra push.

Meantime, we’ll happily collect our dividends (and price gains) while we wait for the payout to get back on schedule.

5 More Urgent Dividend Buys (With Mighty Dividend Magnets)

At times like this, when stocks seem pricey, my Dividend Magnet strategy is a proven way to zero in on the gems regular investors leave behind—like CSX and UNP.

The key is to find stocks whose dividends are lagging behind their payout growth. Then we buy, collect our payouts and ride along as that “dividend gap” slams shut.

It’s a proven strategy we’ve used again and again in my Hidden Yields service.

Like when we bagged a 148% total return from Texas Instruments (TXN) in 5 years … a 57% return in American Tower (AMT) in a little under 3.5 years … or a 92% total return in insurer Assurant (AIZ) in a little over four years.

I know these aren’t the eye-popping 1,000%+ returns you regularly read about on the Internet. But most of those (if they’re real at all) involve heart-stopping risk. We’ll leave that to the gamblers—and instead focus on building lasting wealth using proven indicators like the Dividend Magnet.

I want to share the full strategy with you now, including the best way to put it to work yourself. I’ll also show you 5 stocks with fast-growing payouts I see as our next big winners. Click here to learn more and download a free Special Report naming these 5 top Dividend Magnet plays.